A finance lead signs a PEO agreement believing the hard part is over. Payroll will run, benefits will improve, HR admin will shrink, and employment risk will move to the PEO. That story holds up right until the first claim arrives.

Then essential questions begin. Who is insured. Which policy responds first. Whether the PEO’s coverage is shared across hundreds of clients. Whether the agreement makes the client reimburse the PEO for defense costs. Whether coverage disappears the day the relationship ends.

That’s why PEO liability insurance deserves the same scrutiny as pricing, benefit rates, and service guarantees. The insurance section and indemnity language often decide who writes the check when a manager terminates the wrong employee, a payroll file exposes workforce data, or a workers’ compensation claim crosses state lines. A surprising amount of risk is buried in routine contract language, which is why buyers should review the PEO contract loopholes to watch before signing or renewing.

Table of Contents

- Why Your PEO Contract Is a Liability Landmine

- Deconstructing PEO Insurance Coverage

- Unmasking the Named Insured in Your Policy

- Finding the Risk in Your PEO Service Agreement

- PEO Liability Scenarios What Could Go Wrong

- Your PEO Insurance and Contract Review Checklist

- Negotiating Better PEO Liability Terms

Why Your PEO Contract Is a Liability Landmine

One of the most expensive assumptions in the PEO market is that co-employment means outsourced liability. It doesn’t. It means shared responsibility, and shared responsibility only works when the contract clearly says who carries which risk.

A common pattern looks like this. A company with a lean HR team signs with a national PEO because the sales process highlights compliance support, EPLI access, workers’ compensation administration, and a stronger benefits platform. Months later, a manager terminates an employee after a poorly documented performance issue. The former employee names both the employer and the PEO in the claim. At that point, the client learns the PEO’s insurance isn’t a blanket shield. It’s one layer in a stack that includes the client’s own policies, the service agreement, and the exact endorsement language attached to those policies.

That’s where routine legal wording becomes a budget issue. “Indemnify,” “hold harmless,” and “duty to defend” sound like standard boilerplate until outside counsel starts billing and the carrier asks for policy language.

Practical rule: If liability language feels too technical for an HR or finance review, that’s usually where the biggest uninsured exposure sits.

The market backdrop makes that review more urgent. The global professional liability insurance market was valued at $72.4 billion in 2025 and is projected to reach $138.6 billion by 2034 at a 7.5% CAGR, with Errors and Omissions insurance holding 38.2% of the market in 2025, or about $27.7 billion according to Dataintelo’s professional liability insurance market analysis. That growth is tied to litigation pressure, regulatory demands, and larger liability awards. Those same pressures show up in PEO contracts.

The false comfort of bundled protection

The problem isn’t that PEOs are by their nature risky. Many reduce operational mistakes and improve process discipline. The problem is that buyers often focus on service delivery and skip over how losses are allocated when something goes wrong.

For a CFO, this is a capital preservation issue. For an HR director, it’s an employment governance issue. For an owner, it’s the difference between a manageable claim and a six-figure surprise that was sitting in the agreement all along.

Deconstructing PEO Insurance Coverage

A PEO can show you four insurance boxes checked and still leave a client exposed to the loss that matters most. The critical review starts after the coverage list. The question is how each policy responds, who is insured under it, and whether the limit is available when a claim hits.

A broader primer on what PEO insurance covers helps frame the categories. Contract review has to go further. Buyers need to test whether the policy structure matches the liability the PEO agreement pushes back onto the client.

Workers’ compensation and general liability

Workers’ compensation handles employee injury claims, but the exposure in a PEO arrangement usually sits in the details. Confirm which entity is listed on the policy, which states are covered, how leased employees are classified, and whether the policy follows your workforce as operations change. A coverage dispute after an injury usually starts with paperwork, not medicine.

This also affects cost. If payroll is misallocated by class code or state, the correction shows up later in premium audits, collateral demands, or disputed claims handling.

General liability responds to third-party bodily injury, property damage, and related claims. It is not the policy that fixes most employment disputes, and that gap causes confusion. I often see buyers assume the PEO package covers any lawsuit tied to an employee. General liability does not do that. It protects against a narrower set of operational events involving customers, vendors, visitors, or premises exposure.

EPLI and professional liability

Employment Practices Liability Insurance, or EPLI, is usually the policy clients care about most after a dispute begins. It can respond to wrongful termination, discrimination, harassment, retaliation, and similar claims. In a PEO deal, policy existence is only the starting point. The harder questions are whether defense costs erode limits, whether the retention applies to each claim, and whether the client is drawing from a shared aggregate with every other company in the PEO’s book.

That shared-limit issue is where many deals go sideways. A large master policy can look strong on paper and still deliver weak protection in practice if multiple client claims hit the same aggregate.

Professional liability, often called Errors and Omissions insurance, covers mistakes in the PEO’s professional services, such as payroll administration, benefits enrollment, tax filing support, or HR guidance that causes financial loss. That policy matters because many of the most expensive disputes are not bodily injury claims. They are administrative errors, missed filings, and bad advice with a long cleanup tail. For a plain-language outside reference, PIA Southern Alliance offers a useful overview on understanding E&O coverage.

The right question is not whether the PEO carries insurance. The right question is which policy responds to your loss, whether your company has direct rights under it, and how much limit remains after other client claims.

Cyber liability in the co-employment model

Cyber liability deserves separate review because the PEO often holds payroll data, Social Security numbers, bank information, benefits records, and tax data for multiple employers in one system. That concentration creates two problems. A single incident can affect many client companies at once, and the client may discover too late that the PEO’s cyber policy was built to protect the PEO first.

Review the trigger for coverage, the definition of insured, any sublimits for funds transfer fraud or social engineering, and what happens to protection when the client leaves the PEO. If the coverage terminates with the relationship, replacement insurance needs to be in force before the separation date. Otherwise a routine offboarding decision can create an immediate gap.

Unmasking the Named Insured in Your Policy

Most buyers hear “master policy” and assume scale works in their favor. Sometimes it does. Sometimes it means the opposite.

The first question in any PEO liability insurance review is simple. Is the client a named insured, an additional insured, or just a party with indirect access to the PEO’s coverage. Those are not interchangeable.

Master policy does not mean dedicated protection

A master policy can create the illusion of depth. The declarations page may show large limits, polished carrier names, and broad categories of protection. But if the aggregate is shared across the PEO’s client base, the actual protection available to any one employer may be much thinner than it appears.

A concrete example makes the point. For PEOs like LBMCP, the EPLI policy includes a $6,000,000 aggregate limit covering all client companies and a $2,000,000 per-claim limit, which means one lawsuit could use up to one-third of the total pool before other clients’ claims are paid, as described by LBMCP’s EPLI coverage summary.

That’s the hidden issue behind shared aggregate limits erosion. The client isn’t only underwriting its own employment practices risk. It is also exposed to claims made by companies it doesn’t know, in industries it didn’t choose, managed by supervisors it has never trained.

A useful lens on this appears in the discussion of PEO master policy liability transfer. The value of the policy depends on whether the coverage is dedicated, partitioned, or fully pooled.

What to verify before a claim exists

A buyer should ask for more than a certificate with broad labels. The review should confirm:

| Item | Why it matters |

|---|---|

| Insured status | Named insured status generally gives stronger rights than being listed only as an additional insured or certificate holder. |

| Aggregate structure | Shared aggregates can be depleted by unrelated client claims. |

| Per-claim limit | A high aggregate with a narrow per-claim cap may still disappoint in a serious employment dispute. |

| Defense allocation | Some policies defend both the PEO and the client. Others create friction over whose conduct triggered the claim. |

A shared master policy is not automatically bad. It is bad when the buyer mistakes pooled protection for dedicated protection.

The strongest buyers don’t stop at “Are we covered?” They ask, “Covered how, by whom, and with what priority if several claims hit at once?”

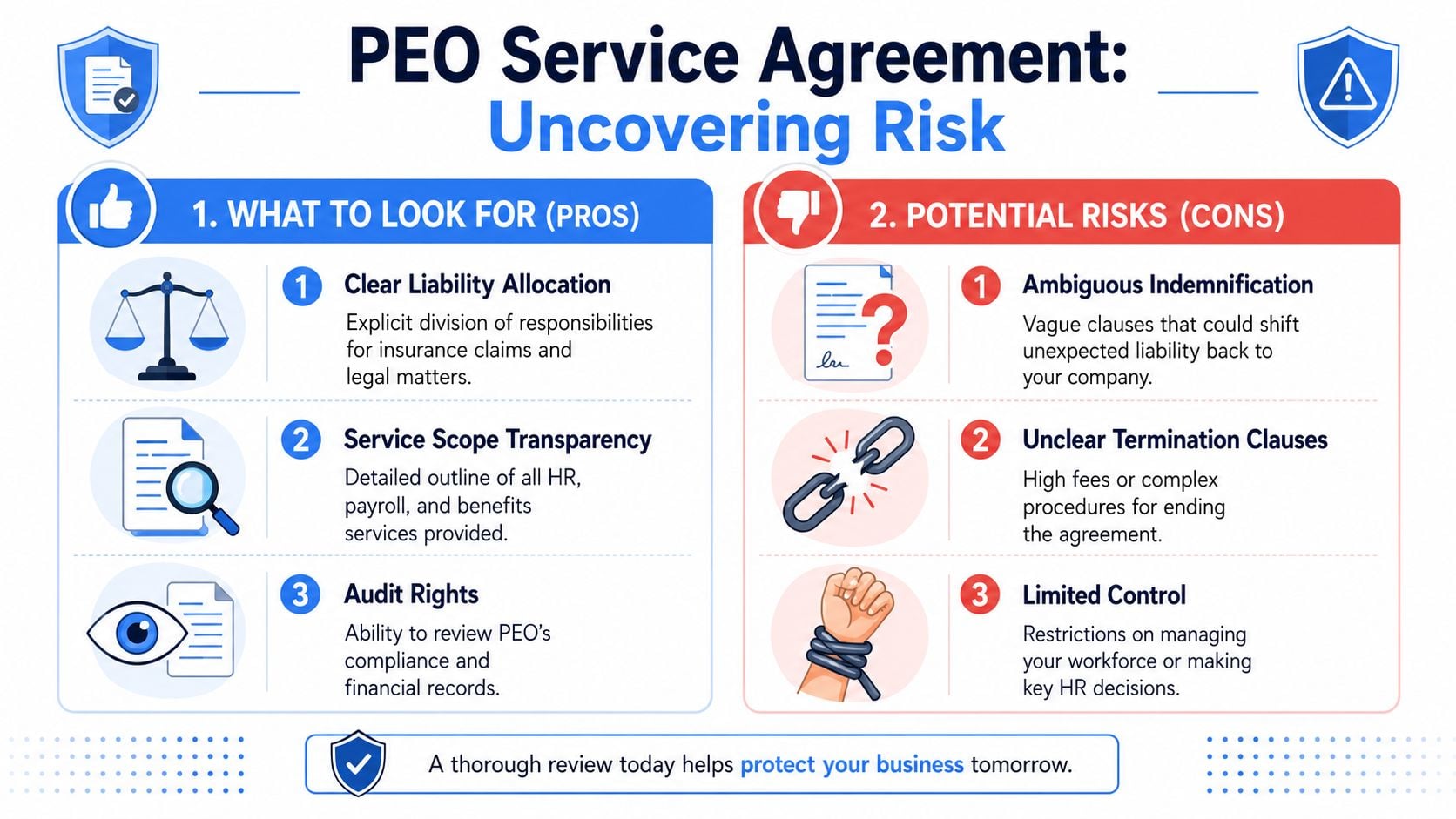

Finding the Risk in Your PEO Service Agreement

Insurance responds to loss. The service agreement decides whose loss it is.

A careful contract review usually turns up risk in a handful of recurring clauses. That’s where finance and HR leaders should slow down and read line by line. The most useful companion resource is a focused look at PEO limitation of liability clause review, because limitation language often works together with insurance and indemnity provisions.

Clauses that shift money, not just responsibility

Three clauses matter most.

Indemnification decides who reimburses whom after a claim.

Hold harmless language can expand that obligation.

Duty to defend determines who pays for lawyers at the beginning of the dispute, not just after liability is sorted out.

That’s why legal guidance on negotiating contract indemnification is useful during a PEO review. The wording can look balanced while still shifting most financial burden back to the client.

There’s also a technical workers’ compensation point many buyers miss. In co-employment arrangements, PEOs are typically named as additional insureds under both Part One Workers’ Compensation and Part Two Employers’ Liability of the client’s policy, which helps share liability for leased employees. If that language is absent, the client may face sole liability, based on the New York PEO endorsement language published by NYCIRBEndorsement-May%201,%202020.docx).

Weak language versus strong language

Below is the practical difference between a clause that protects the relationship and one that loads risk onto the client.

| Clause style | What it usually means in practice |

|---|---|

| Weak client-side clause | The client indemnifies the PEO for claims “arising out of employment decisions,” even when the PEO advised on or processed the action. |

| Stronger shared-risk clause | Each party indemnifies the other for claims caused by its own negligence, misconduct, or contractual breach. |

| Weak defense clause | The client must defend immediately, before fault is determined. |

| Stronger defense clause | Defense obligation follows a clear trigger tied to actual responsibility, with cooperation requirements on both sides. |

Review every sentence that includes “sole discretion,” “arising out of,” or “related to.” Those phrases often widen the client’s obligation far beyond what the sales discussion implied.

The best contract language doesn’t eliminate disputes. It keeps them from turning into avoidable uninsured ones.

PEO Liability Scenarios What Could Go Wrong

A claim rarely arrives labeled with the coverage dispute that follows. It shows up as a demand letter, a regulator inquiry, a forensic invoice, or a workers’ compensation file. Then the contract starts deciding who pays first.

A termination claim hits both parties

A client terminates a supervisor after a series of attendance problems. The file is incomplete. There are gaps in the write-ups, one manager used inconsistent language, and the employee had recently asked for an accommodation. The complaint that follows alleges discrimination, retaliation, and wrongful termination.

Both the client and the PEO get named. That is common when the PEO helped with handbook language, leave administration, payroll coding, or termination processing.

The first problem is not the merits of the claim. It is the fight over whose policy responds and whose retention applies. I see buyers assume the PEO’s EPLI will step in because the PEO touched the process. The service agreement often says the client kept control over the employment decision, which gives the PEO room to deny responsibility or tender the claim back.

The second problem is limit erosion. If the PEO’s EPLI sits inside a shared aggregate across many clients, your claim is competing with losses you cannot see. A CFO may believe the company bought a clean layer of protection, only to learn the available limit was already reduced by unrelated claims from other worksite employers.

Ask two direct questions before renewal. Is the client covered under the PEO’s EPLI for this type of allegation, and is that limit dedicated or shared? If the answer to either question is unclear, the exposure is still sitting on the client’s balance sheet.

The PEO system suffers a breach

A payroll administrator at the PEO clicks on a convincing phishing email. Attackers get into a file repository holding W-2 data, direct deposit details, addresses, and benefits enrollment records for several clients. Your employees start calling your HR team, not the PEO’s broker.

Weak contract drafting quickly becomes expensive. The PEO may carry cyber insurance, but the client’s rights under that policy are often narrow, temporary, or tied to specific enrollment terms. Coverage can also end with the PEO relationship, which creates a serious tail-risk problem during a provider transition. If a breach is discovered after the move, each side may argue the other should report it.

The financial exposure goes beyond notice letters. There may be forensic costs, counsel, call center support, credit monitoring, regulatory response, wage disruption, and fraud losses tied to payroll or funds transfer. If the PEO’s cyber limit is shared across its client base, one large event can consume a meaningful part of the aggregate before your company even submits its own expenses.

If the PEO holds the data, the client still owns the employee relationship and the reputational damage.

The fix is not just “confirm cyber coverage exists.” Require written confirmation of who is insured, what event triggers client access to coverage, whether the limit is shared, how prior acts and post-termination reporting work, and who controls breach counsel and vendor selection.

An injury claim exposes an allocation gap

A warehouse employee gets hurt at a client site shortly after the company expands into a new state. Operations assumed the PEO had already folded that location into the workers’ compensation setup. The endorsement package says otherwise.

Now there are three active disputes at once. Was the worker properly scheduled in that state? Which entity had the duty to report payroll and class codes correctly? Who handles the claim if the service agreement assigns responsibilities differently from the policy structure?

These files get expensive even before liability is resolved. Defense costs start. The injured worker needs benefits decisions. The state agency may ask questions about registration, coverage placement, and reporting. If the policy structure and the contract do not match, the client can end up funding a claim it thought had been transferred.

This is the pattern across PEO disputes. The insurance issue is rarely just “is there a policy.” The key question is whether the contract gives your company reliable access to that policy, to an intact limit, and to a defense obligation that does not disappear the moment fault is contested.

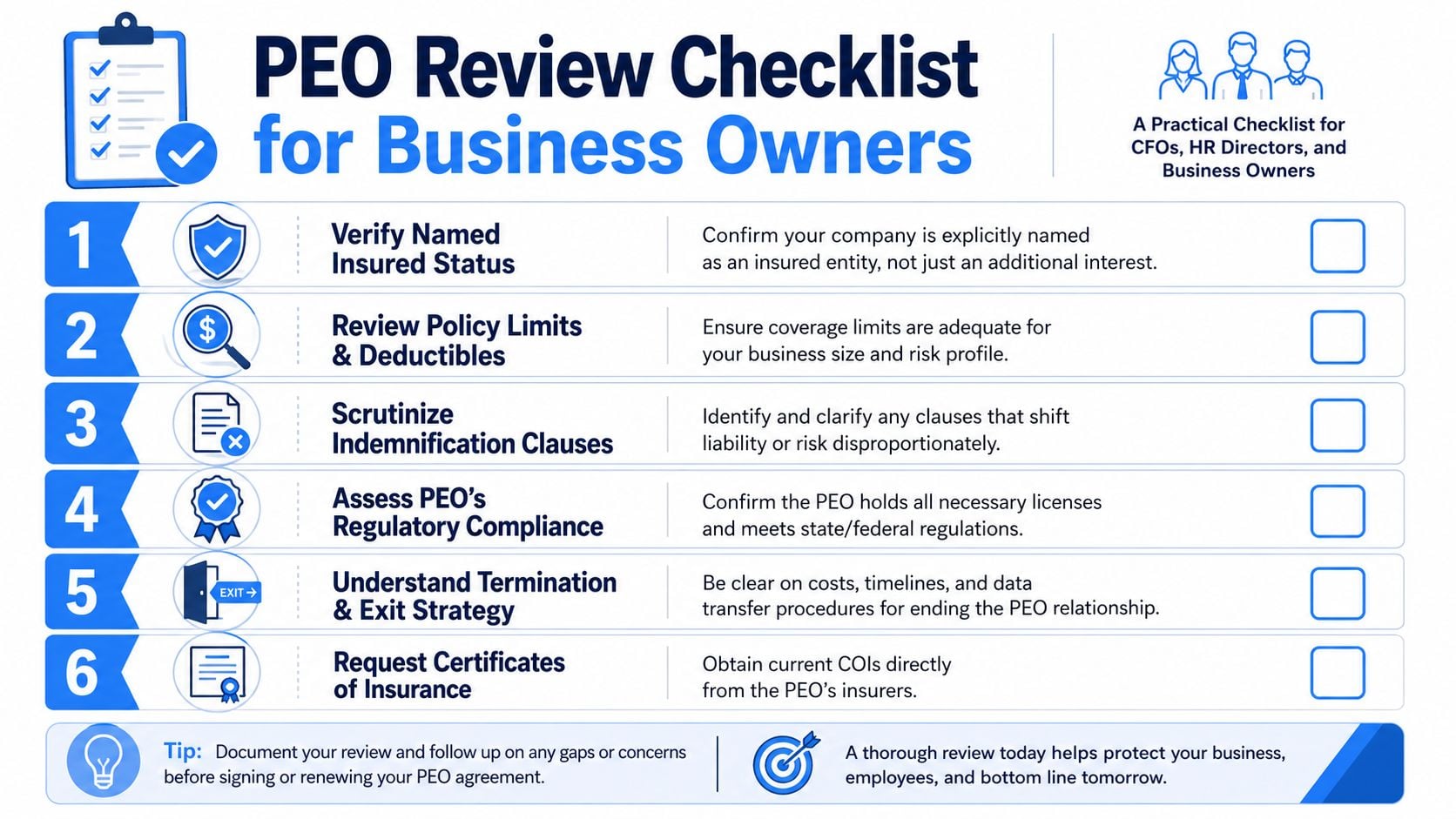

Your PEO Insurance and Contract Review Checklist

A good review process should produce documents, not reassurance. If the PEO can’t produce clear evidence, the buyer shouldn’t assume the coverage works the way the proposal says it works.

Documents to request

Use this list during diligence, renewal, or before a provider switch.

- Current certificates of insurance. Request current COIs directly and make sure the named entities, policy types, and effective dates align with the actual service agreement.

- Relevant endorsements. Don’t rely on summary schedules alone. Endorsements often answer key insured-status and termination questions.

- Service agreement exhibits. Liability allocation is sometimes pushed into exhibits, addenda, or state-specific attachments.

- Claim reporting instructions. A delayed notice problem can complicate coverage even when the underlying claim would otherwise qualify.

Questions to ask before renewal or transition

The strongest checklist is question-driven.

- Are we a named insured anywhere that matters most? If not, what rights do we have under the policy.

- Is the aggregate shared with other clients? If yes, how is erosion tracked and disclosed.

- What happens to EPLI when the PEO relationship ends? This one matters more than most buyers realize.

- What happens to cyber coverage at exit? If the PEO relationship ends, does data-related protection continue for prior incidents.

- Which claims are clearly our responsibility under the contract, and which are the PEO’s? Ask for the answer tied to contract sections, not sales language.

One fact should drive the exit review. Cancellation of the PEO relationship automatically triggers cancellation of the EPLI policy, creating a serious coverage cliff. A company switching providers needs tail coverage or an extended reporting period for claims filed after the exit date tied to prior incidents, as explained in Cooley’s discussion of using a Professional Employer Organization.

Checklist mindset: The right answer isn’t “don’t worry, we handle that.” The right answer is “here’s the endorsement, here’s the clause, and here’s what survives termination.”

Negotiating Better PEO Liability Terms

Most PEO buyers negotiate admin fees and implementation credits. Fewer negotiate the terms that decide who pays when a claim lands. That’s a mistake.

The strongest advantage is clarity. A buyer doesn’t need to accuse the PEO of bad faith. It needs to insist that the written terms match the risk both parties say they’re sharing. That’s especially important because 40% of SMBs switching PEOs face unexpected liability exposure in the first 6 months due to unclear termination clauses and coverage gaps related to shared policies, according to NAIFA’s discussion of PEO shopping questions.

A useful preparation step is reviewing PEO indemnification negotiation tips before renewal or provider selection. The negotiation usually improves once the buyer asks narrower, harder-to-deflect questions.

Negotiation points worth pushing

- Dedicated or ring-fenced EPLI capacity. Ask whether the PEO can offer protection that isn’t fully exposed to unrelated client claims.

- Mutual indemnification. If each party controls part of the employment process, each party should stand behind its own conduct.

- Clear defense obligations. Require contract language that says who defends first and under what trigger.

- Exit protection. Require written terms for tail coverage, extended reporting, and post-termination data handling.

- Policy transparency. Ask for the actual structure, not just a marketing summary of “included coverage.”

Language that moves the conversation

Direct phrasing works better than broad objections:

- Please revise the indemnity so each party is responsible for claims caused by its own acts, omissions, negligence, or contractual breach.

- Please confirm whether our EPLI protection sits inside a shared aggregate and whether a dedicated option is available.

- Please add language confirming what coverage survives termination and what tail or extended reporting options apply.

PEO liability insurance shouldn’t be treated as a side note in the agreement. It’s one of the core products the buyer is purchasing, whether it’s priced separately or embedded in the bundle.

PEO buyers that want help pressure-testing insurance terms, comparing contract language across providers, and negotiating cleaner liability protections can work with PEO Metrics to evaluate options side by side and spot the risks that sales decks usually leave out.