A Texas leadership team usually reaches the same point before searching for a professional employer organization in Texas. Payroll is getting messy. Benefits costs are hard to predict. HR keeps absorbing compliance work that nobody planned for. Then proposals start coming in, and instead of clarity, the team gets five versions of the same promise with different fee structures, different service language, and very different contract risk.

That's where most buying processes go sideways. The problem usually isn't whether a PEO can help. The problem is whether the buyer can tell the difference between a strong-fit provider and an expensive mismatch before signing a co-employment agreement.

Table of Contents

- Why Choosing a PEO in Texas Is More Complicated Than You Think

- Navigating Texas PEO Compliance and Licensing

- Comparing PEO Service Models and Benefits Packages

- How to Benchmark and Analyze PEO Costs in Texas

- Identifying Critical Risk Flags in Your PEO Contract

- Key Levers for Negotiating a Better Texas PEO Deal

Why Choosing a PEO in Texas Is More Complicated Than You Think

The hardest part of buying a professional employer organization in Texas usually isn't finding one. It's narrowing the field without getting trapped by polished sales process, vague pricing, or generic bundles.

One Texas directory says 121 different PEOs operate in Texas in its Texas PEO provider listing. That changes the buying problem completely. This is not a thin market where employers take whoever is available. It's a crowded market with national firms, regional firms, niche providers, industry specialists, broker-led options, and firms that look similar until contract review starts.

Many articles still spend most of their time defining co-employment. That's useful for a first pass, but it doesn't solve the actual decision. A buyer comparing multiple proposals needs to know who handles payroll exceptions, who owns the benefits strategy, who escalates claim issues, how renewal pricing works, and what happens if the relationship fails.

Practical rule: In Texas, buyer confusion usually comes from too many plausible options, not too few.

A common failure pattern looks like this:

- The shortlist is too broad: HR gathers proposals from several recognizable names, but the list mixes full-service PEOs, lighter-touch models, and firms built for very different employer profiles.

- The comparison stays too shallow: Finance compares the admin fee but doesn't normalize setup charges, software fees, reporting costs, or termination language.

- The implementation story wins: A provider with the best sales engineer and cleanest demo gets the nod, even though service delivery after go-live may look very different.

- The contract gets reviewed last: Legal receives the agreement after the business has already committed emotionally to the vendor.

That's why the first task isn't “learn what a PEO is.” It's “build a filtration process that strips away noise.” Teams that need a baseline definition can review what a professional employer organization is quickly, then move to the harder work of comparing service model, pricing architecture, compliance posture, and exit risk.

Operationally, proposal review also creates a document problem. Census files, benefit summaries, implementation scopes, and contract exhibits often arrive in inconsistent formats, especially PDFs. When a finance or HR team needs to standardize those inputs fast, tools that eliminate manual PDF data entry can reduce comparison errors and speed up side-by-side analysis.

The takeaway is simple. In Texas, the market is large enough that almost any company can find a PEO. The primary value comes from ruling out the wrong ones faster.

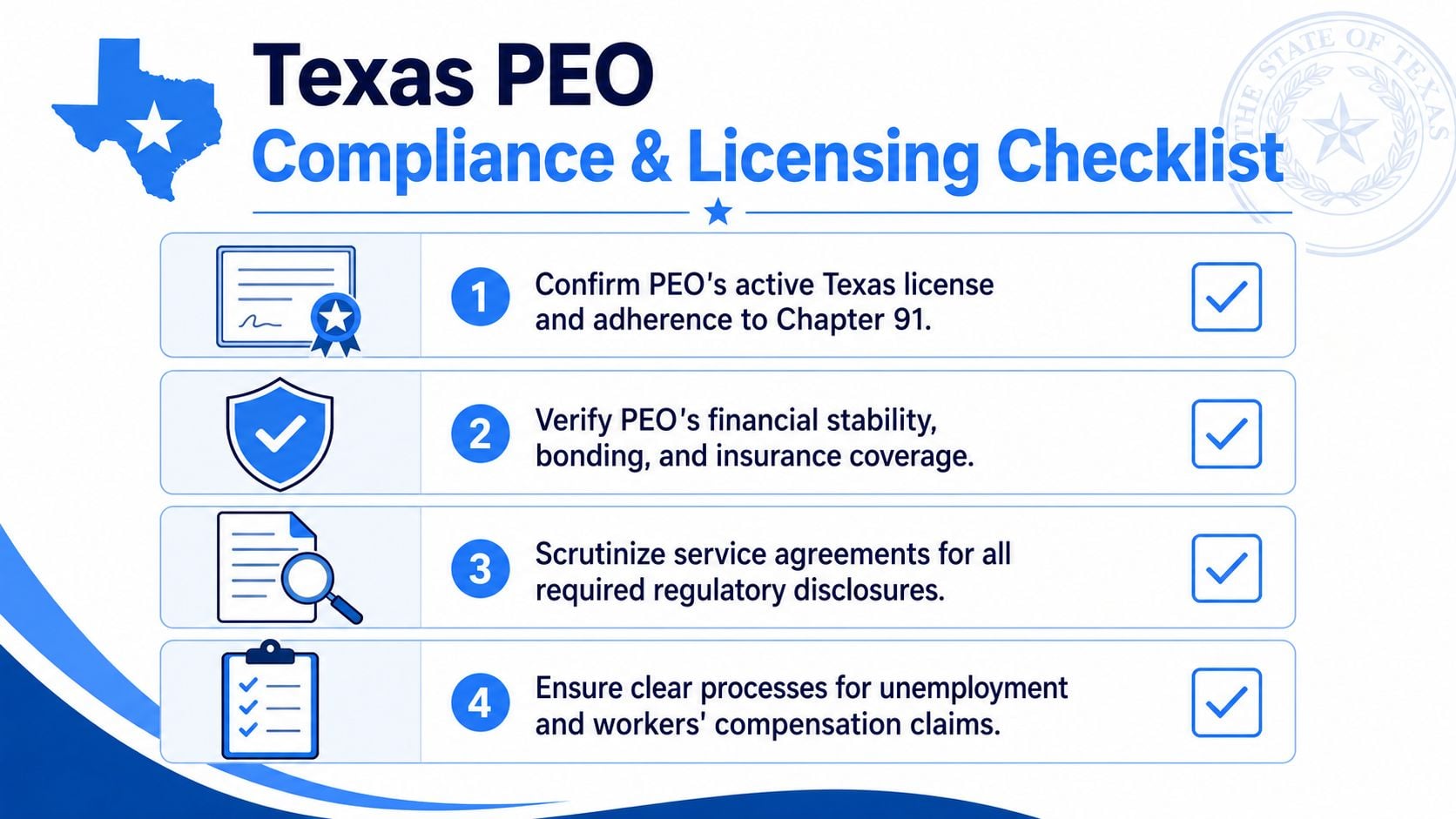

Navigating Texas PEO Compliance and Licensing

A CFO gets a proposal that looks competitive, the implementation team sounds polished, and benefits pricing is in range. Then legal checks the contracting entity and finds a mismatch between the brand in the sales deck and the entity expected to employ the worksite staff in Texas. That is not a paperwork detail. It is an early warning that diligence is starting too late.

Start with license verification

In Texas, licensing is the first screen. PEOs are regulated under Chapter 91 of the Texas Labor Code, and the Texas Department of Licensing and Regulation requires licensure for this category. TDLR also notes that "staff leasing company" is the older term replaced by PEO, sets minimum positive working capital thresholds based on assigned employee count, and publishes the related fee schedule for initial and renewal filings in its Texas Department of Licensing and Regulation PEO FAQ.

That does not tell a buyer which provider will execute well. It does tell you whether the provider has cleared a basic regulatory and financial threshold in Texas.

Use a tighter diligence sequence than most sales processes encourage:

- Confirm the exact licensed entity name. Do not accept only the parent brand or trade name from the proposal.

- Match that entity to the contract. If a different affiliate will sign, get a written explanation of the legal structure and operating roles.

- Ask who holds the employer-facing obligations in practice. Payroll tax filings, unemployment claims, workers' compensation administration, and employee notices should not sit in a gray area.

- Request proof of current standing before redlines begin. It is easier to disqualify a provider early than renegotiate after internal stakeholders are committed.

This step matters more in Texas because the market is crowded. Buyers often compare three providers that all sound credible, but one may have a cleaner entity structure, a clearer compliance process, and fewer handoffs between affiliates. Those differences rarely show up in the demo.

What Texas compliance review should actually test

The useful question is not merely, "Are you licensed?" The useful question is, "How does your licensed structure affect my risk if something goes wrong?"

Ask for direct answers on these points:

- Unemployment claims administration: Who receives notices, who drafts responses, and what response-time obligations stay with the client

- Workers' compensation handling: Which party reports the injury, manages carrier communication, and owns return-to-work coordination

- Payroll tax operations: Which filings the PEO submits under its structure, which approvals the client must still make, and how correction errors are escalated

- Employee onboarding disclosures: What Texas-specific notices are issued, by whom, and how acknowledgment records are stored

- Audit and document access: Whether the client can get reporting quickly if a state agency, auditor, lender, or buyer asks questions

A licensed provider can still be operationally messy. I have seen buyers assume the compliance model was strong because the provider cleared the state requirement, then discover after go-live that claims management was fragmented across service teams and outside partners. The license reduced one category of risk. It did not remove execution risk.

Multi-state employers need one more layer of review. A provider may be orderly in Texas and inconsistent elsewhere, especially if acquisitions created a patchwork operating model. That is where a closer review of PEO state law compliance exposure across jurisdictions helps separate a Texas fit from a broader platform fit.

The practical takeaway is simple. In Texas, compliance review should eliminate weak candidates and expose entity-structure problems early. It should also help the buyer avoid overpaying for a provider that is merely available, but not built to support the way the company operates.

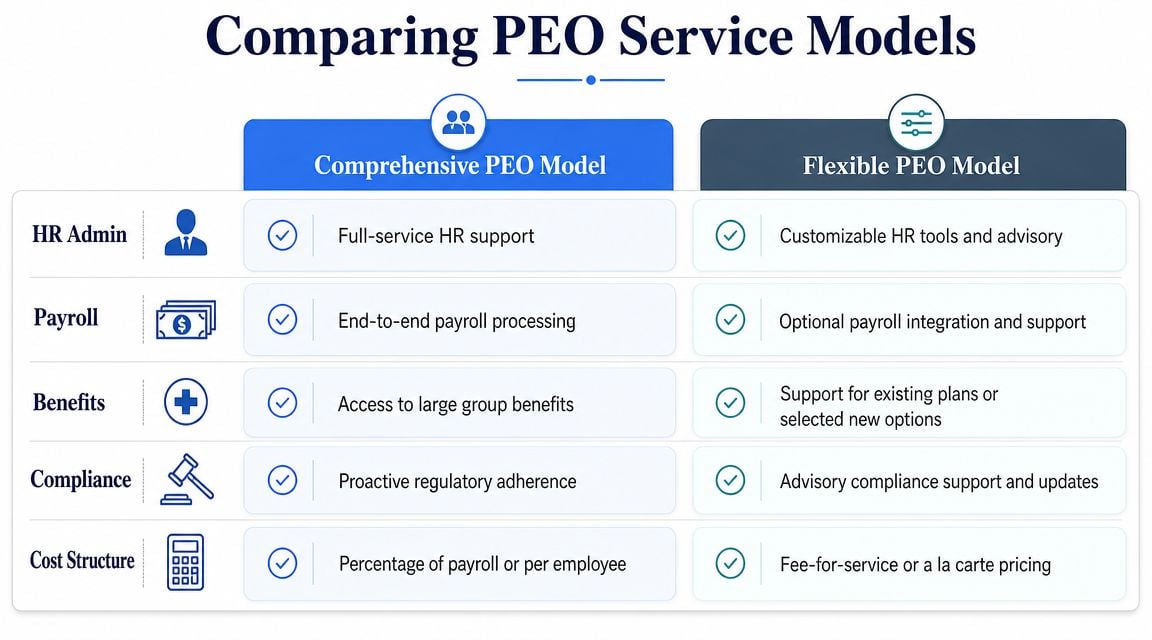

Comparing PEO Service Models and Benefits Packages

Once the licensing screen is cleared, the next issue is operating model. Two PEOs can offer payroll, benefits, HR support, and compliance administration on paper while delivering a very different day-to-day experience after implementation.

The service model matters more than the demo

A professional employer organization in Texas often falls somewhere between a high-touch relationship model and a service-center model. Neither is automatically better. The right fit depends on who inside the client company uses the service.

An HR director with strong internal process may do well with a structured support model, clear ticketing, and specialized teams for payroll, benefits, and compliance. A founder-led business with a lean back office often needs a more direct relationship with named contacts who know the company's history and can solve issues without repeated handoffs.

The trade-offs usually look like this:

| Service question | Dedicated relationship model | Shared service or call-center model |

|---|---|---|

| Day-to-day support | More continuity with the same contacts | More standardized routing |

| Escalation path | Often clearer and faster for recurring issues | Can require multiple handoffs |

| Best fit | Lean internal HR, fast growth, hands-on leadership | More mature HR operations, repeatable workflows |

| Risk | Relationship quality depends heavily on assigned team strength | Speed may vary by queue and case type |

That table won't appear in most sales decks, but it usually determines whether the partnership feels smooth or frustrating six months later.

If the buyer can't name who will own payroll exceptions, benefits escalation, and HR issue triage after implementation, the service model is still too vague.

Benefits strength is real, but fit still matters

Benefits are one of the main reasons employers consider a PEO, and Texas is a major market. NAPEO reports that 13% of all PEO clients are located in Texas, making it one of the top three states by client concentration. The same industry data says more than 200,000 businesses nationwide use PEO services and the broader U.S. PEO industry supports about 4 million worksite employees, as summarized in this NAPEO market overview.

That concentration matters because it tends to attract strong provider competition and gives many Texas employers access to broader plan options than they could easily assemble alone. But benefits access alone shouldn't close the deal.

A disciplined buyer asks narrower questions:

- Carrier choice: Is the company buying into a fixed master plan menu, or does the provider offer meaningful plan design options?

- Contribution flexibility: Can the employer shape contribution strategy by class, location, or workforce needs within the provider's structure?

- Enrollment support: Who handles employee questions during open enrollment and new hire onboarding?

- Broker coordination: If the company has an existing advisor relationship, can it still be used productively?

For deeper context on how carriers, pooled buying power, and plan structure affect negotiating advantage, this overview of PEO benefits negotiation leverage is worth reviewing.

A good benefits package that comes with the wrong service model often disappoints quickly. The strongest PEO fit combines usable benefits with support delivery that matches how the client runs HR.

How to Benchmark and Analyze PEO Costs in Texas

Most buyers start with the headline fee. That's understandable, but it's where comparison errors begin. A PEO quote only becomes meaningful after the team rebuilds it into a total-cost view.

The pricing model can distort the real cost

Independent Texas buying guidance notes that PEOs commonly charge either a flat per-employee-per-month fee or a percentage of gross payroll, and that the percentage model can become materially more expensive for highly compensated teams while the flat model is usually more predictable. The same guidance warns buyers to watch for hidden add-ons such as setup costs, renewal increases, reporting or software charges, and cancellation penalties in this Texas PEO pricing guide.

That distinction matters a lot for companies with uneven compensation. A business with a large number of executives, technical specialists, commissioned sales staff, or bonus-heavy employees may see the percentage model rise because payroll rises. The underlying HR workload may not have changed much, but the fee does.

A company with a more stable hourly or mid-salary workforce may find percentage pricing less volatile, but it still needs to test year-two and year-three cost assumptions.

A simple comparison table changes the conversation

The fastest way to expose pricing differences is to force every quote into one worksheet. Even when provider assumptions differ, a common format makes outliers obvious.

| Metric | PEO A (3.5% of Payroll) | PEO B ($120 PEPM) |

|---|---|---|

| Pricing basis | Percentage of gross payroll | Flat per employee per month |

| Sensitivity to raises and bonuses | High | Lower |

| Predictability for budgeting | Lower | Higher |

| Best fit | Lower-paid or stable payroll mix | Higher-paid or mixed compensation teams |

| Risk area to test | Payroll growth increases fee | Add-on charges and service exclusions |

The exact numbers in live quotes will vary, but the comparison logic doesn't. If compensation rises, the percentage model rises with it. If headcount rises, the PEPM model rises more transparently. Finance teams need both views in the same file.

Benchmark test: If the provider won't help normalize the quote into a clean apples-to-apples model, the buyer should assume the structure benefits the seller.

What belongs in the cost worksheet

A proper worksheet should separate the visible price from the true cost of operation. At minimum, it should include:

- Admin fee structure: Record whether pricing is percentage-based or PEPM, and note what compensation elements affect the billed amount.

- Implementation charges: Ask whether setup, onboarding, data migration, or first payroll conversion fees are billed separately.

- Technology line items: Some providers bundle reporting and software. Others charge separately for modules, exports, or enhanced access.

- Renewal provisions: The worksheet should capture whether annual increases are capped, discretionary, or tied to specific conditions.

- Off-cycle and exception activity: Manual checks, corrections, special payrolls, and custom reports can add recurring friction if priced separately.

- Exit cost exposure: Include termination fees, notice-period obligations, and any charges tied to transition support.

One more discipline helps. Build the worksheet around the company's real census, not a simplified sales sample. Segment employees by compensation pattern, state footprint, and benefits eligibility. Otherwise, the quote may look cheaper only because the assumptions are cleaner than reality.

Teams that need a deeper framework can review how much a PEO costs to structure a more complete benchmarking model.

The buyer's job isn't to find the lowest visible fee. It's to identify the provider with the best net value after pricing mechanics, add-ons, and contract behavior are all translated into one financial view.

Identifying Critical Risk Flags in Your PEO Contract

A weak contract can undo a good proposal. That's why the service agreement deserves more scrutiny than the pitch deck, the benefit summary, and the implementation slide combined.

Termination language can erase any savings

The first clause many buyers underestimate is termination. A low admin fee loses its appeal fast if the agreement locks the client into a long notice period, automatic renewal, or financial penalties tied to early exit.

The practical question isn't just “Can the company terminate?” It's “Under what conditions, with how much notice, and with what financial consequence?” A provider that's easy to enter but expensive to leave is in a stronger position than the buyer may realize.

Watch for these patterns:

- Automatic renewal language: If the contract renews unless notice is given in a narrow window, the buyer can lose bargaining power before renewal talks even start.

- Broad early termination fees: Some agreements convert expected future revenue into a charge that survives even when service quality drops.

- Vague transition support: If the contract doesn't define offboarding responsibilities, data transfer can become slow and painful right when the company needs speed.

- One-sided breach standards: The provider may retain broad rights to suspend service for payment issues while the client has limited remedies for underperformance.

“The cheapest PEO contract on signature day can become the most expensive one to unwind.”

A legal team that wants a fast reference point on baseline employment document structure may find TheLawGPT's employment contracts useful as a general drafting resource, but a PEO agreement still requires specialized review because co-employment language changes the risk profile.

Liability wording deserves line-by-line review

Liability provisions are where buyers often assume more protection than the contract provides. Marketing language may emphasize compliance support, but the agreement may allocate many practical responsibilities back to the client through approvals, representations, and indemnity clauses.

That doesn't mean the provider is acting improperly. It means the buyer needs precision.

A focused review should test:

- Who is responsible for data accuracy: If the client supplies incorrect wage, classification, or employee-status data, how much liability shifts back?

- What happens after a recommendation is ignored: Does the PEO document its advice and then disclaim downstream exposure if the employer chooses differently?

- How broad are indemnification duties: Is the client indemnifying the provider for routine operational issues or only for clearly client-caused events?

- What remedies exist for service failures: If taxes are mishandled, payroll is processed incorrectly, or required notices are missed, what contractual remedy is available?

For a sharper checklist of problem clauses, PEO contract negotiation red flags offers a useful lens.

Contracts don't need to be hostile to be risky. They only need to be imprecise in the wrong places.

Key Levers for Negotiating a Better Texas PEO Deal

Most PEO agreements have more flexibility than buyers assume. The advantage usually comes from being specific, prepared, and willing to negotiate items beyond the headline admin fee.

Ask for concessions that change total value

A better Texas PEO deal often comes from a handful of terms that materially affect cost control and operational flexibility.

- Scope alignment: Strip out services the company won't use. A mature HR team may not need the same advisory depth as a founder-led business. Paying for bundled support that sits idle is common and avoidable.

- Rate protection: Ask for a multi-year rate lock or a clear cap on annual increases. If the provider won't hold pricing, ask what conditions trigger changes and force those conditions into writing.

- Implementation relief: Setup fees, conversion charges, and first-year onboarding costs are often negotiable, especially when the client presents a clean census and organized transition plan.

- Fee transparency: Require a full list of recurring and non-recurring charges in the order form or main agreement, not buried in an exhibit or implementation appendix.

- Benefits flexibility: If benefits are a major reason for switching, ask whether there are multiple carrier or plan design paths instead of accepting the first packaged menu.

Tie service promises to accountability

Service promises matter less if they aren't measurable. Negotiation should push beyond “white glove support” and into operating commitments.

A buyer can ask for:

| Negotiation lever | What to ask for | Why it matters |

|---|---|---|

| Support ownership | Named points of contact or defined support structure | Reduces confusion after go-live |

| SLA language | Response and escalation expectations in writing | Creates accountability |

| Renewal mechanics | Clear notice periods and pricing review windows | Preserves leverage before auto-renewal |

| Exit support | Defined offboarding assistance and data transfer obligations | Makes switching feasible if needed |

The strongest negotiating posture comes from presenting the provider with a disciplined issue list instead of broad dissatisfaction. “Please remove setup fees, cap annual increases, confirm transition support, and define escalation contacts” gets further than “Can you sharpen the pencil?”

One more point matters in Texas. Because the market is large and fragmented, buyers usually have more alternatives than the sales process suggests. That only helps if the team uses competitive pressure carefully and asks each provider to respond to the same commercial and legal points.

For teams preparing for a renewal or final-round negotiation, PEO Metrics helps employers compare providers, benchmark costs, and pressure-test contract terms so they can secure a stronger PEO agreement with fewer surprises.