A lot of companies reach the PEO vs ASO decision at the same moment. Headcount is climbing, payroll is getting messy across states, benefits renewals are painful, and the HR team is either one person deep or split between finance and operations. The immediate question sounds simple: which model costs less?

That's usually the wrong starting point.

For a CFO or owner, PEO vs ASO is a structural decision about employer liability, cash flow predictability, benefits strategy, and operating control. A 75-person company can feel large enough to outgrow ad hoc HR, while still being too small to negotiate from strength on benefits, compliance support, or workers' compensation administration. That's where the model choice starts affecting real business outcomes, not just administrative convenience.

Many leadership teams also underestimate how much this choice changes the back office. Tax filings, benefits sponsorship, who carries the insurance framework, and who sits in the line of fire when an employment issue surfaces all shift depending on the model. Companies exploring broader human resources outsourcing options usually find that the legal structure matters more than the feature list.

Table of Contents

- When to Choose Between a PEO and an ASO

- The Core Difference Co-Employment Explained

- PEO vs ASO A Side-by-Side Comparison

- Modeling the True Cost PEO and ASO Scenarios

- The Decision Framework When to Choose Each Model

- Negotiation and Contract Risks to Avoid

- PEO vs ASO Frequently Asked Questions

When to Choose Between a PEO and an ASO

A common trigger point is a company with about 75 employees, operations in several states, and a finance leader who's tired of discovering HR risk after the fact. Payroll runs, but every exception takes too long. Benefits are up for renewal. Managers want faster hiring. Nobody is fully confident about leave rules, handbook language, or onboarding consistency.

At that point, a PEO and an ASO can both look attractive on paper. Both can support payroll, benefits administration, HR technology, and compliance-related work. The difference is that they solve different problems.

A PEO usually fits when leadership wants a broader operating partner and is willing to accept a co-employment structure in exchange for a more integrated setup. An ASO usually fits when the company wants administrative help but intends to keep legal employer status, maintain more direct control, and manage more responsibility internally.

The best choice often comes down to one question: does the company need help doing HR administration, or does it need a new operating structure for employment itself?

That distinction matters most when a business is growing faster than its internal systems. A founder-led company with a lean HR function may need relief now. A larger business with a stable HR team may need support without changing the legal framework underneath its workforce.

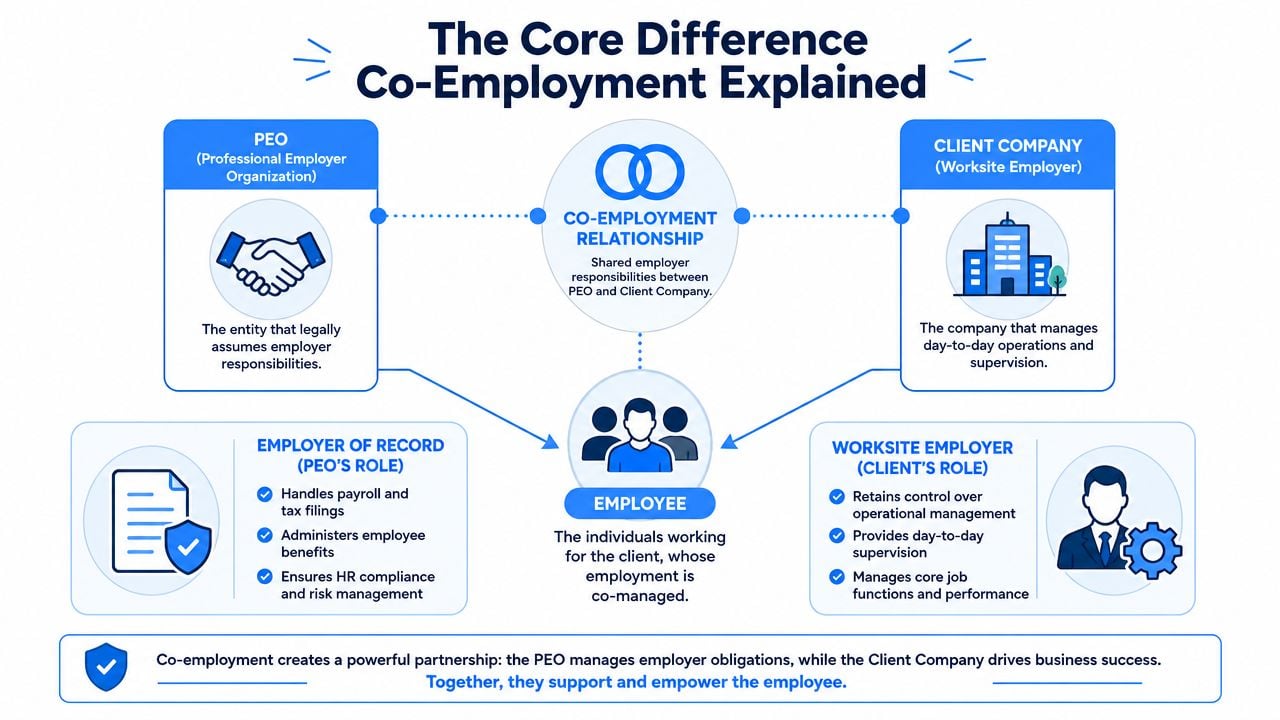

The Core Difference Co-Employment Explained

The center of the PEO vs ASO decision is co-employment.

According to the U.S. Chamber's explanation of PEO vs ASO, the defining difference is that in a PEO arrangement, the provider becomes a co-employer and may act as the employer of record for tax and insurance purposes, while in an ASO arrangement, the client remains the sole employer of record and keeps its own FEIN for filings. That's the single fact that drives most downstream differences.

Why co-employment changes the entire analysis

Under a PEO model, employer obligations are shared in a formal relationship that can include payroll, benefits administration, workers' compensation support, and compliance services. Under an ASO model, the provider is closer to a service vendor. The client still holds the employment relationship and the related liability.

That means the legal position is different before anyone even talks about pricing.

A PEO can file under its own tax framework for covered employees and may bundle insurance and compliance administration into the same relationship. An ASO typically processes and supports, but the client company still sits in the primary legal seat. For finance and HR leaders, that changes how risk should be modeled, how contracts should be read, and how an exit should be planned.

A practical way to think about the split

An ASO is like hiring a property manager for a building the company still fully owns. The manager handles administrative work, but ownership, core responsibility, and major exposure stay with the company.

A PEO is more like bringing in a formal operating partner for the employment infrastructure. The client still runs the business day to day, supervises employees, sets compensation, and directs work. But some employer responsibilities are shared through the co-employment structure. A more detailed walkthrough of that legal setup appears in this guide to PEO co-employment explained.

Practical rule: If leadership wants support without shifting the employer framework, an ASO is usually the cleaner fit. If leadership wants a more integrated compliance and insurance structure, a PEO usually deserves a harder look.

PEO vs ASO A Side-by-Side Comparison

A CFO choosing between a PEO and an ASO is usually deciding three things at once. Who carries which employment risks. How much operational control the company keeps. What the back office will cost after fees, insurance, internal labor, and claim exposure are added up.

The comparison below is useful, but the key decision sits in the second and third order effects. A lower visible admin fee can still produce a higher total employer cost if the company keeps more compliance work, broker coordination, and claims exposure in-house.

PEO vs. ASO Key Differentiators

| Criteria | PEO (Professional Employer Organization) | ASO (Administrative Services Organization) |

|---|---|---|

| Employment structure | Co-employment relationship | Vendor relationship |

| Employer of record status | PEO may act as employer of record for tax and insurance purposes | Client remains sole employer of record |

| Tax filing framework | Often tied to the PEO structure | Client keeps its own FEIN |

| Liability position | Shared employer obligations within the formal relationship | Client retains the employment relationship and associated liability |

| Benefits approach | More integrated and often bundled with administration | Usually client-sponsored and handled separately |

| Workers' compensation support | Often part of the integrated relationship | Usually remains in-house with the client |

| Service scope | Broader HR outsourcing structure | Narrower administrative arrangement |

| Buyer profile | Often appealing for smaller employers without deep HR infrastructure | Often appealing for employers that want modular control |

A more detailed legal breakdown appears in this PEO legal structure vs ASO comparison.

What changes in practice

On paper, both models can cover payroll, benefits administration, reporting, and HR support. In practice, the difference shows up when something goes wrong.

With a PEO, the provider is part of a formal employer structure. That usually means tighter process requirements around onboarding, payroll coding, employee classification, workers' compensation handling, and policy administration. It can reduce execution gaps, but it also requires the client to operate inside the provider's rules and systems.

With an ASO, the company keeps more freedom. It can preserve its current broker, benefits design, HRIS, and internal approval flow. That flexibility has a cost. The company usually keeps more responsibility for policy consistency, manager training, state notices, leave administration decisions, and defense of employment practices.

That trade-off matters more than the feature list.

Benefits, workers' compensation, and vendor sprawl

Smaller employers often choose a PEO because it simplifies a messy operating setup. Payroll, benefits administration, compliance support, and workers' compensation management are often handled in one service model. For a company with 20 or 40 employees and no senior HR leader, that can remove a real amount of coordination work from finance and operations.

An ASO fits better when the company has already built a decent employment infrastructure. If leadership likes its current carriers, has a broker that knows the industry, and wants to keep plan design control, an ASO often creates less disruption. That is common in firms that already have HR staff, established workflows, and benefit programs they do not want to replace.

I usually advise clients to look at this through a finance lens. Bundling is not automatically cheaper. It is often easier to administer. Those are different outcomes.

Cost signals that matter

Pricing should be read as a structure question, not just a fee question.

PEO pricing is often tied to payroll or charged as a flat per-employee fee. ASO pricing is often charged as an administrative fee layered onto the employer's existing insurance, broker, payroll, and compliance stack. That means a side-by-side quote can mislead buyers if one proposal includes workers' compensation administration, benefits platform access, payroll tax administration, and HR support while the other leaves those items outside the base fee.

The better comparison asks four questions:

- What services are included in the stated fee?

- What expenses stay outside the contract?

- What internal headcount or manager time is still required?

- Where does claim, audit, or compliance exposure remain?

A company may prefer the ASO model because the invoice is lower and the control is higher. That can be the right call. It is also common for that same company to underestimate the value of internal time spent managing vendors, handling escalations, reviewing filings, and cleaning up preventable errors.

Which side usually wins

A PEO usually wins when the business wants tighter infrastructure, fewer moving parts, and more administrative relief, even if that means giving up some vendor choice and process flexibility.

An ASO usually wins when the business has the staff and discipline to manage its own employment framework and wants support services without changing that structure.

For CFOs, the deciding factor is rarely preference alone. It is the full cost of control versus the full cost of outsourcing.

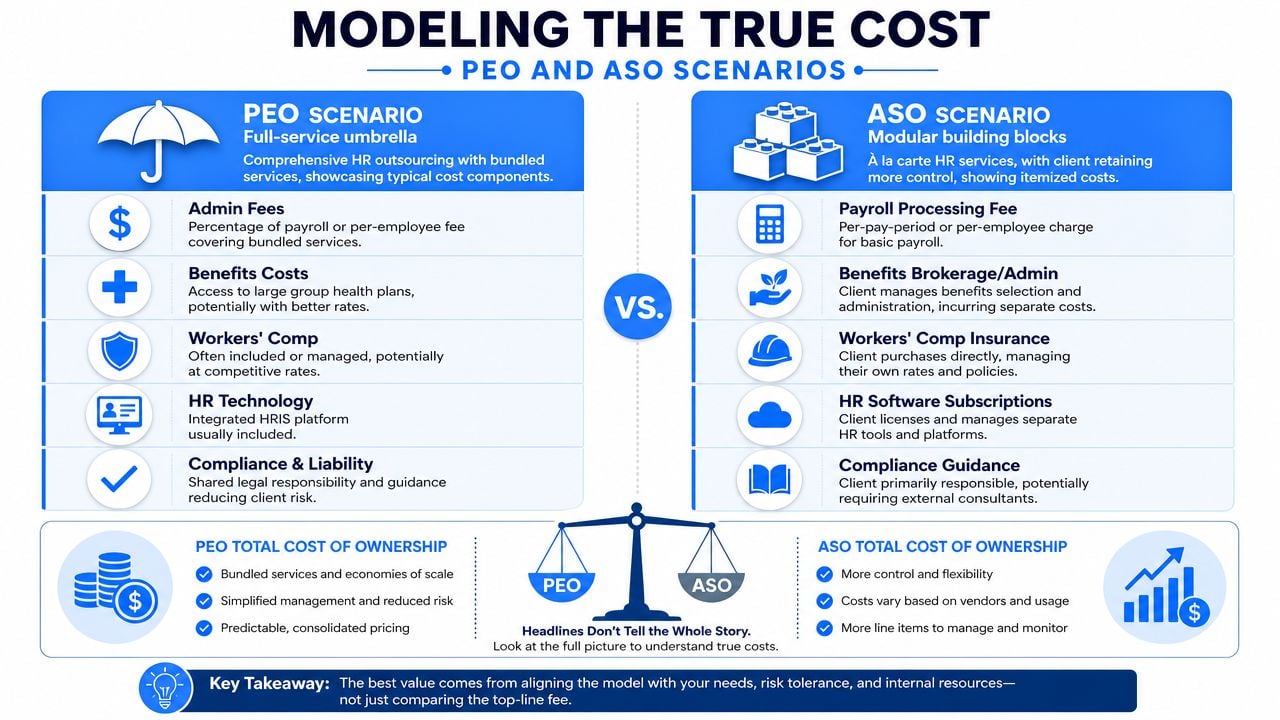

Modeling the True Cost PEO and ASO Scenarios

A CFO reviewing PEO and ASO proposals usually sees one immediate problem. The invoice is visible, but the true cost drivers are scattered across benefits, payroll administration, compliance work, manager time, and retained legal exposure.

One proposal may look higher because more cost is bundled into the fee. Another may look leaner because key obligations stay with the employer. Paradigm International's PEO vs ASO guide is a useful companion read if you want a second operator-focused view of that distinction.

Scenario one 25 employees and no HR bench

A 25-person software company is hiring fast. There is no HR director. Payroll sits with finance, onboarding sits with operations, and employee relations issues land on whoever is available that week.

In that setup, an ASO can appear cheaper because the admin fee is lower. The problem is that the employer still has to assemble and manage the rest of the stack. That usually includes broker coordination, policy administration, payroll oversight, employee issue triage, and follow-up on compliance tasks that do not disappear just because an outside partner is involved.

The hidden cost shows up in labor and error rates. If a controller spends several hours each pay period fixing deductions, answering notices, or chasing enrollment issues, that time belongs in the model. If managers handle terminations or leave questions without clear process support, the legal risk belongs in the model too.

I usually tell clients to price this scenario in four buckets: vendor fees, internal labor, benefit cost differentials, and retained risk. Once you do that, the cheaper line item often stops looking cheaper. A finance team that wants a cleaner side-by-side comparison can build one with this PEO financial modeling template for total cost analysis.

Scenario two 500 employees and an established HR team

Now change the fact pattern. The company has 500 employees, an HR leader, in-house payroll capability, established carriers, and enough process discipline to manage issues before they turn into claims.

In that case, the economics often shift. The company may already have the staff to run open enrollment, coordinate leave administration, handle handbook updates, and manage state registrations without buying an integrated co-employment structure. An ASO can preserve existing vendor relationships and avoid the switching cost that comes with moving benefits, payroll workflows, and employee support into a new model.

The trade-off is straightforward. A larger employer can spread administrative work across existing team members, so bundled convenience has less financial value. A PEO may still make sense if the company has heavy multi-state complexity, poor internal controls, or a weak benefits position. But if the infrastructure is already in place, paying for a broader bundle can raise total cost without reducing enough risk to justify the difference.

The practical takeaway is simple. The lower-cost option depends on what the company would otherwise need to hire, fix, insure, or supervise on its own.

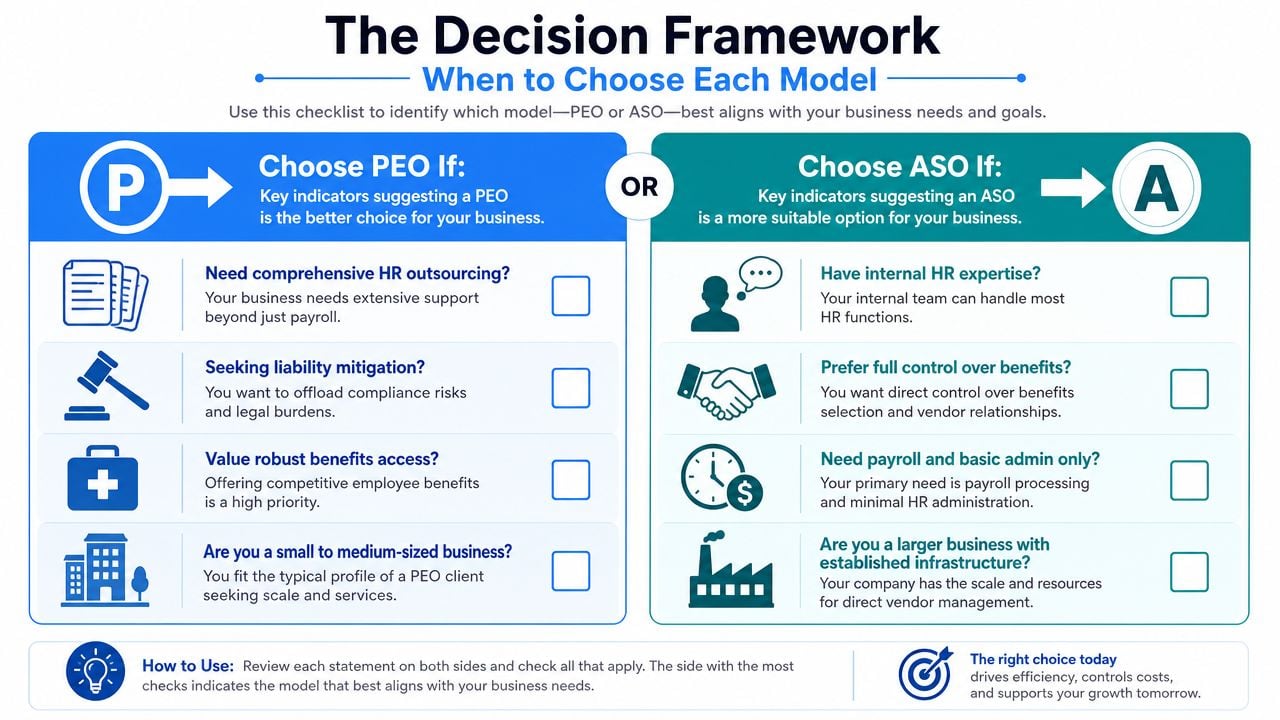

The Decision Framework When to Choose Each Model

A CFO usually reaches this decision after a trigger event. Hiring expands into new states. Benefits renewals jump. Payroll errors start pulling finance into employee issues. The question is not which model has more features. The question is which model lowers total cost and risk for the next 12 to 36 months.

The cleanest way to decide is to test four variables at the same time: internal HR capacity, compliance exposure, benefits strategy, and tolerance for retaining employer-side responsibility. A PEO usually wins when the business needs operating support and risk containment more than customization. An ASO usually wins when the business already has a capable team and wants to keep control over vendors, plans, and processes.

Choose a PEO when these conditions are true

A PEO fits best when leadership is trying to solve several problems with one operating model.

- Internal HR coverage is thin. Payroll, onboarding, benefits questions, leave tracking, and policy updates are landing on a controller, office manager, or founder instead of a dedicated HR team.

- Compliance mistakes would be expensive. The company is hiring across multiple states, cleaning up classification issues, or dealing with inconsistent documentation and employment practices.

- Benefits are hurting recruiting or retention. Leadership needs a stronger package and wants administration, employee support, and compliance help bundled together.

- Finance wants fewer people-related surprises. The company is willing to pay more for a model that can reduce administrative strain, close process gaps, and create clearer accountability.

In practice, this often describes a smaller or fast-growing employer that cannot justify building a full internal HR infrastructure yet. The premium can be rational if it replaces at least one hire, improves benefits competitiveness, and lowers the chance of costly errors.

Choose an ASO when these conditions are true

An ASO is usually the better financial choice when the company already has the basics under control and wants targeted support instead of co-employment.

- An HR leader or experienced people team is already in place. The business can handle employee relations, handbook updates, leave coordination, and vendor oversight internally.

- The company wants to keep direct employer control. Plan sponsorship, policies, carrier relationships, and employment administration are strategic decisions leadership does not want to hand off.

- Current vendors are working. There is no strong reason to replace carriers, brokers, payroll workflows, or reporting structures just to gain more bundled service.

- The business is comfortable retaining more responsibility. Management understands that lower fees often mean more work and more legal exposure remain in-house.

This is often the right fit for larger employers, but size alone should not drive the decision. I have seen a 75-person company use an ASO well because it had a strong HR director and disciplined processes. I have also seen a 300-person company choose a PEO because multi-state growth and weak controls were creating too much risk.

A simple test helps. If the business would need to hire HR staff, replace benefit support, or tighten compliance processes in the next year, a PEO may be the cheaper decision after those costs are added back in. If those capabilities already exist and perform well, an ASO often preserves flexibility and lowers total spend.

Negotiation and Contract Risks to Avoid

A weak contract can erase the savings that made the model look attractive in the first place. I have seen companies choose the lower quoted fee, then spend the next year arguing over off-cycle payroll charges, carrier handoffs, and who owns the employee data at exit.

What to lock down before signing

The pricing discussion should start with invoice logic, not just the headline rate. A PEO may quote a percentage of payroll or a per-employee fee. An ASO often looks cleaner on paper, but the lower admin fee can hide separate charges for implementation, benefits administration, reporting, or year-end work. For a CFO, that is the difference between a cost you can forecast and one that drifts every quarter.

Get the contract specific on four points:

- Service scope. List who handles payroll processing, tax filings, benefits administration, leave tracking, compliance support, reporting, and employee issue escalation.

- Fee treatment. Spell out charges for setup, off-cycle payrolls, special reports, open enrollment support, year-end processing, broker coordination, and carrier work.

- Termination terms. Define notice periods, transition help, final invoice timing, and exactly how employee and payroll data will be returned.

- Renewal controls. Require a review window before renewal and written limits on how fees can change.

A practical checklist helps during legal review. These PEO contract negotiation red flags cover the clauses that tend to create cost overruns and messy exits.

Where buyers get surprised

The hidden risk in a PEO contract is often exit cost. The hidden risk in an ASO contract is often scope gap.

With a PEO, buyers should test what happens if the relationship ends in the middle of a plan year, after an acquisition, or during rapid hiring in a new state. Ask who handles payroll conversion, benefits transitions, tax account changes, and employee communications. If those duties are vague, the company may end up paying internal staff, outside counsel, and a new vendor to rebuild the infrastructure on a tight deadline.

With an ASO, the pressure point is different. The contract may promise support, but support can mean advice only, not execution. That distinction matters when a wage claim, leave dispute, or multistate registration issue lands on the internal team. If your HR lead still has to coordinate vendors, interpret policy, and manage the deadlines, the lower fee may not be the lower total cost.

Small omissions create expensive problems. Data access, response times, indemnity wording, and implementation responsibility matter more than polished sales presentations.

The safest approach is to negotiate the contract as if the relationship will be tested in year one. That means pricing changes, a disputed service issue, and a possible exit all need to work on paper before you sign.

PEO vs ASO Frequently Asked Questions

Is an ASO just a more expensive payroll provider

No. A payroll provider typically focuses on payroll processing and related filings. An ASO usually sits one layer above that and can support benefits administration, reporting, HR processes, and compliance-related administration while the client remains the employer of record.

The confusion happens because some ASO arrangements are narrow and some are broader. Buyers should ask what work the provider will perform versus what it will only advise on.

What happens when a company outgrows a PEO

The company usually doesn't “cancel and move on” overnight. It has to reset pieces of the employment infrastructure. Payroll, benefits administration, tax filing workflows, data migration, and vendor ownership all need a transition plan.

That's why mature buyers model the exit before they sign. A company that expects major growth, M&A activity, or a future shift toward a custom HR stack should treat exit complexity as part of the original buying decision.

Can a company use a PEO for some employees and an ASO for others

Sometimes, yes, but only if the workforce structure is designed carefully. Different legal entities, employee classes, or operating divisions can create room for mixed models. The complexity is real, though. Payroll, benefits eligibility, management practices, and compliance oversight can become harder, not easier.

For companies comparing those structures, independent evaluation tools can help separate service scope, pricing, benefits design, and contract terms. PEO Metrics is one example of a comparison-focused advisory service that helps employers assess providers and negotiation points without relying only on vendor sales materials.

If a leadership team is actively weighing PEO vs ASO, PEO Metrics can help compare provider structures, pricing models, benefits trade-offs, and contract terms so the decision is based on total cost and risk, not just a sales demo.