A company lets go of a manager after months of performance issues. The file includes coaching notes, a final warning, and a termination memo signed by HR. Leadership thinks the process was clean.

Then the demand letter arrives.

The former employee alleges retaliation, discrimination, and damage to reputation. The first surprise is operational. HR pulls records, managers get interviewed, and the finance team starts asking where defense costs will hit the budget. The second surprise is insurance. General Liability usually isn't built for employment disputes, so the company learns too late that one of the most expensive risks on the balance sheet sat outside the policy they assumed would respond.

That gap is why the question isn't just what does EPLI insurance cover. The better question is whether the policy covers the way the company hires, disciplines, promotes, and exits people in real life. For employers in a PEO, that question gets more complicated because the coverage may sit inside a master policy with terms the client never negotiated directly.

Table of Contents

- The Lawsuit You Did Not See Coming

- What EPLI Actually Covers Day to Day

- Real Claim Scenarios and Their Financial Impact

- Deconstructing Your Policy Limits Exclusions and Endorsements

- How EPLI Costs Are Calculated and What You Control

- Evaluating EPLI Inside a PEO Agreement

- Your Action Plan for EPLI Evaluation

The Lawsuit You Did Not See Coming

A wrongful termination claim rarely starts as a major event inside the business. It starts as an ordinary management decision. A supervisor documents missed targets. HR confirms policy steps. Leadership approves the exit. Then a lawyer reframes the same facts as discrimination, retaliation, or harassment tied to the termination.

That shift matters because a business isn't just defending a personnel file. It's defending every email, every manager comment, every exception to policy, and every inconsistency between what happened and what the handbook says should happen. Even when the employer believes it acted properly, the cost of proving that can be painful.

Good documentation helps. It doesn't eliminate the need to defend the company.

Many owners and finance leaders misread the risk. They think broad business insurance will absorb it. Employment claims sit in a separate lane. EPLI exists because decisions involving hiring, promotion, discipline, and termination create a distinct liability exposure that standard liability policies typically don't pick up.

Preventive process still matters. Practical legal checklists like Miles Hansford business law guidance are useful because they focus on the habits that reduce dispute frequency in the first place, including clear agreements, consistent procedures, and early review of legal risk.

For a CFO, the key point is simple. An employment claim isn't just a legal problem. It's a budget shock, a management distraction, and often a reputational issue at the same time. EPLI should be evaluated as protection for management decisions, not as an optional add-on that sits somewhere in the insurance schedule.

What EPLI Actually Covers Day to Day

Employment Practices Liability Insurance is designed to cover lawsuits tied to employment decisions and workplace conduct, including wrongful termination, discrimination such as age, race, gender, or disability, harassment, retaliation, and failure to hire or promote. It also typically pays defense costs such as lawyers, settlements, and judgments up to the policy limit, as explained in this overview of EPLI coverage.

That sounds broad, but the practical reading is better than the textbook reading. EPLI covers the risk created by the employer's people decisions. If a company recruits, interviews, promotes, disciplines, evaluates, or terminates employees, it has exposure in this category.

The claims that usually trigger EPLI

Some claims are obvious. Others show up after an otherwise routine decision.

- Wrongful termination: A former employee says the firing violated law or policy, or that the stated reason was pretext.

- Discrimination: The allegation may target the hiring process, promotion decisions, compensation treatment, restructuring choices, or accommodation issues.

- Harassment: The claim can arise from supervisor conduct, coworker conduct, or a failure to respond after a complaint.

- Retaliation: This often becomes the centerpiece after an employee reports misconduct, requests accommodation, or raises a compliance concern.

- Failure to hire or promote: Applicants and internal candidates can allege unfair treatment tied to protected characteristics.

For teams reviewing options, Find employment practice protection is a useful outside reference because it frames EPLI the way buyers shop for it, by looking at covered events, defense obligations, and policy structure rather than abstract definitions.

A practical benchmark for buyers comparing policy structures inside and outside a PEO sits on PEO Metrics' EPLI coverage page, which outlines the questions that usually expose gaps.

EPLI coverage at a glance

| Typically Covered Claims | Common Exclusions |

|---|---|

| Wrongful termination | Bodily injury |

| Discrimination | Property damage |

| Harassment | Intentional or dishonest acts |

| Retaliation | Claims outside policy terms or endorsements |

| Failure to hire or promote | Matters that may require separate coverage treatment |

The table is where buyers should slow down. “Covered” doesn't mean unlimited, automatic, or broad in every version of the policy. “Excluded” doesn't just mean denied. It often means the company discovers too late that a claim landed in a carve-out, sublimit, or endorsement issue that wasn't discussed during purchase.

Practical rule: If the policy language doesn't clearly track the company's real HR processes, the coverage may look stronger on paper than it performs in a claim.

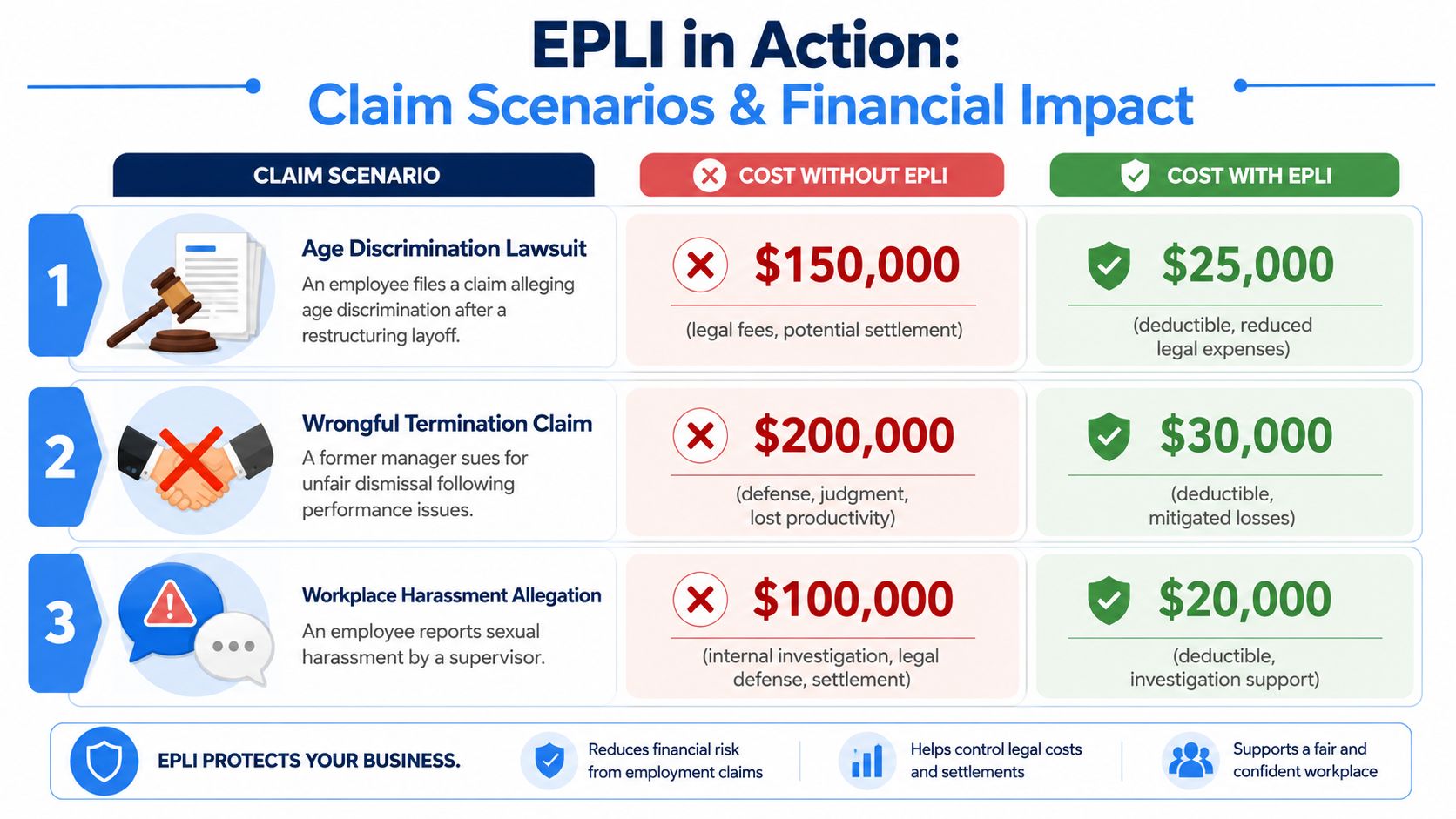

Real Claim Scenarios and Their Financial Impact

The fastest way to understand what does EPLI insurance cover is to stop thinking in policy categories and look at how claims unfold inside a business. Most of the damage starts before anyone knows whether the case has merit. HR collects records. Managers are pulled into interviews. Counsel gets involved. Normal work slows down.

Employers that want to understand how that liability can be allocated in a co-employment setting should also review PEO liability in wrongful termination claims, especially before assuming the PEO absorbs the risk.

Scenario one when a routine employment decision turns adversarial

A company restructures a department and selects one long-tenured employee for layoff. Leadership believes the decision was role-based. The employee alleges age discrimination and points to comments about “new energy” and “modern leadership.”

The direct legal costs are only part of the problem. The business has to produce records showing why this person, and not someone else, was selected. If the file is uneven or the criteria shifted during the process, defense gets harder quickly.

What works:

- Consistent selection criteria: The same business rationale applied across the group.

- Clean documentation: Notes, evaluations, and restructuring records that line up.

- Early carrier notice: The insurer can engage counsel before the file gets worse.

What doesn't:

- Loose manager language: Offhand comments often become exhibits.

- Backfilled reasons: A rewritten narrative after the claim arrives damages credibility.

Scenario two when conduct by one manager creates enterprise risk

A supervisor makes repeated inappropriate jokes. Employees complain informally, but no one escalates the issue through the formal channel until a resignation triggers legal counsel.

This type of claim often exposes governance failure more than isolated misconduct. Plaintiffs' counsel will test whether the company trained managers, documented complaints, and responded consistently. If HR knew and delayed action, the employer's defense posture weakens.

A harassment claim often becomes a process claim. The question isn't only what the manager did. It's what the company did after learning about it.

Scenario three when a weak process becomes the real problem

An employee reports concern about pay treatment or manager conduct, then gets terminated soon after for “fit” issues. Even if leadership had genuine performance concerns, the timing creates a retaliation narrative.

Finance leaders should focus on operational drag. The company may spend months dealing with hold notices, interviews, legal review, and leadership time. In a smaller organization, the same executive team that approved the termination may become the witness pool.

A policy can fund defense and covered loss. It can't repair a weak internal process after the fact. That is why EPLI should be purchased alongside disciplined HR procedures, not instead of them.

Deconstructing Your Policy Limits Exclusions and Endorsements

EPLI's value sits in the terms buyers skip. A policy schedule may look adequate until a claim tests timing, limit structure, or a missing endorsement.

According to IRMl's EPLI definition and policy overview, EPLI is typically written on a claims-made basis and is designed to cover wrongful acts arising from the employment process, including wrongful termination, discrimination, sexual harassment, retaliation, failure to promote, defamation, invasion of privacy, and negligent evaluation. These policies commonly include defense costs, settlements, and judgments up to the policy limit, and often extend insured status to directors, officers, management personnel, and employees.

Claims-made changes the timing risk

Claims-made means timing matters twice. The act has to fit within the policy's terms, and the claim usually has to be made and reported in the right window. That becomes a serious issue when a company changes carriers, exits a PEO, or discovers a complaint after renewal.

CFOs should ask four direct questions:

- What triggers coverage: Is the policy clearly claims-made, and what reporting obligations apply?

- Who is insured: Are executives, managers, and employees all included?

- How do defense costs erode limits: Some buyers focus on the headline limit and miss the fact that defense can eat into it.

- What happens on exit: If the company leaves the PEO or changes insurers, is there any continuity protection?

For side-by-side evaluation, this comparison of PEO master policies and standalone policies helps frame the structural differences that matter before a claim is filed.

The endorsement that many public-facing employers miss

Some EPLI policies can be extended to cover third-party harassment or discrimination claims from customers, vendors, or contractors, not just employees. This extension is critical for service, retail, and healthcare businesses but is often an optional endorsement, not standard coverage, as described in AmTrust's discussion of EPLI and third-party coverage.

That distinction matters more than many buyers realize. A medical practice, hospitality group, staffing company, or field service business may have more meaningful interaction with non-employees than with internal staff on any given day. If a customer alleges harassment by an employee, the company may assume EPLI responds. Sometimes it won't unless the endorsement was added.

The cleanest negotiation point in EPLI is often not the premium. It's whether the policy quietly omits a claim category the business is exposed to every day.

A serious review should also test exclusions for intentional misconduct, claim reporting, and any endorsement wording that narrows non-employee claims. If the business is public-facing, third-party coverage shouldn't be treated as optional until someone proves the exposure is immaterial.

How EPLI Costs Are Calculated and What You Control

EPLI pricing starts with workforce exposure, not just revenue. The underwriter looks at how many employees the company has, what industry it operates in, where those employees work, how claims have been handled in the past, and how disciplined the HR infrastructure appears.

A practical pricing marker exists for smaller employers. MSA Insurance's EPLI overview notes that premiums can start at about $500 per year for a business with up to five employees for $1 million in coverage, while a small business under 100 employees may expect around $5,000 annually. That same source also notes that pricing scales with employee count, industry, and claims history, against a backdrop of more than 65,000 discrimination charges resolved by the EEOC in 2022.

What drives premium

The variables that usually move cost most are straightforward:

- Employee count: More employees usually means more hiring, more terminations, and more management interactions.

- Industry profile: Public-facing and labor-intensive environments often present different claim patterns than office-based operations.

- Claims history: Prior disputes signal underwriting risk.

- Policy structure: Limits, retention, endorsements, and carrier appetite all change price.

Companies estimating spend should compare that external market context with EPLI insurance cost analysis when reviewing PEO-bundled terms against standalone alternatives.

What an employer can influence before renewal

The best way to lower risk isn't clever negotiation language. It's cleaner operating discipline.

- Manager training: Supervisors need plain rules on interviewing, documentation, accommodations, complaints, and terminations.

- Handbook quality: Policies should match actual practice. A polished handbook that no one follows creates its own evidentiary problem.

- Documentation standards: Hiring decisions, promotion choices, performance warnings, and exits should be recorded consistently.

- Escalation paths: Employees need a clear complaint route outside the direct manager.

A broker or underwriter can't fix weak HR hygiene. They can only price it. Employers with tighter processes generally put themselves in a better position to negotiate terms and defend claims.

Evaluating EPLI Inside a PEO Agreement

Bundled EPLI inside a PEO can be efficient. It can also create blind spots if the client treats it like a black box.

The attraction is obvious. A PEO may place coverage through its master insurance structure, fold parts of the cost into the service package, and align claims handling with the HR and compliance support it already provides. For some employers, especially those without internal risk management depth, that structure can be simpler than building a standalone tower of advisors, brokers, and carriers.

Why bundled coverage can work

There are legitimate advantages:

- Administrative simplicity: The employer gets one operating relationship instead of coordinating multiple vendors.

- Integrated support: HR guidance, handbook review, and claims reporting may sit closer together.

- Potential advantage in placement: A larger master structure can create access to terms an individual smaller employer may not secure on its own.

That said, simpler doesn't always mean better protected.

Where the hidden trade-offs sit

The main questions aren't marketing questions. They're contract questions.

- Is the limit dedicated or shared: If the aggregate is shared across many clients, one large claim elsewhere can affect perceived security.

- Who controls claims: The client should know who selects counsel, who decides settlement strategy, and how much visibility the employer gets.

- Is third-party coverage included: Public-facing employers shouldn't assume it is.

- What happens at termination: When the PEO relationship ends, continuity of coverage needs direct attention.

- Who is formally named: The insured structure should be reviewed carefully.

A detailed framework for these issues appears in this explanation of PEO employment practices liability structure. That kind of review is especially useful when a PEO says EPLI is “included” but doesn't immediately provide specimen wording, endorsement schedules, reporting instructions, or details on shared limits.

If a PEO can't explain the carrier, the limit structure, the retention, and the claim workflow in plain language, the buyer doesn't yet know what it bought.

One practical option during evaluation is to use an independent comparison process such as PEO Metrics, which reviews PEO pricing, benefits, contract terms, and liability language so employers can see where bundled EPLI offers an advantage and where it creates risk.

Your Action Plan for EPLI Evaluation

A useful EPLI review ends with decisions, not definitions.

For HR directors, the first move is an internal audit of the moments most likely to create a claim. Review hiring practices, promotion criteria, complaint intake, investigation procedures, and termination documentation. Then compare those workflows to the policy language and any PEO claim-reporting instructions. If there is a mismatch, the process or the coverage needs to change.

For CFOs, treat EPLI as a financial volatility tool. Compare the annual premium and retention against the cash impact of an uninsured employment dispute, including legal defense, executive time, HR disruption, and possible settlement pressure. The premium discussion gets clearer when leadership models the downside as a budget event instead of as an insurance line item.

For founders and CEOs, the questions should be blunt:

- Who is the carrier and what type of policy is it

- Is the coverage standalone or part of a shared master program

- Are defense costs inside the limit

- Is third-party coverage included or endorsed separately

- What happens to coverage if the company leaves the PEO

The takeaway is simple. The right EPLI policy doesn't just answer what does EPLI insurance cover. It answers whether the company's actual people-risk decisions are covered when the claim arrives, who controls the response, and what balance-sheet exposure remains after the policy starts working.

PEO decisions often turn on details that don't show up in the sales presentation, especially around EPLI, shared limits, and post-termination coverage. PEO Metrics helps employers compare PEO options, benchmark contract terms, and identify liability language worth negotiating before signing or renewing an agreement.