The renewal packet is on the desk. The PEO says EPLI is included. HR assumes that box is checked. Finance is focused on medical trend, payroll taxes, and the admin fee. Then legal asks a simple question: who owns the policy, controls the claim, and has access to the limit if a manager is accused of retaliation next quarter?

That's where most PEO buyers realize they haven't evaluated EPLI insurance carriers at all. They've evaluated a bundled service arrangement. Those aren't the same thing.

For companies with 10 to 2,000 employees, especially those hiring across multiple states, the hidden issue isn't whether EPLI matters. It's whether the PEO's master policy is broad enough, transparent enough, and dedicated enough to protect the employer when a claim becomes expensive, public, and distracting.

Table of Contents

- Evaluating EPLI Beyond Your PEOs Master Policy

- Decoding Key EPLI Policy Terms and Red Flags

- A Framework for Comparing EPLI Insurance Carriers

- How EPLI Functions in PEO vs Standalone Scenarios

- Negotiating Your EPLI Coverage and Terms

- Making the Final Decision Key Takeaways

Evaluating EPLI Beyond Your PEOs Master Policy

The default assumption in many PEO deals is simple: if EPLI is bundled, the employer is covered. That assumption breaks down quickly under scrutiny.

Employment claims aren't rare edge cases. EPLI lawsuits have increased by 400% in the last two decades, which is why this coverage now sits squarely inside core risk management rather than in the “nice to have” category, according to Coalition's explanation of why employers need EPLI. When the frequency of claims rises that sharply, policy structure matters as much as policy presence.

What the bundled model often hides

A PEO master policy can be useful, but it comes with trade-offs that many buyers don't see during implementation:

- Shared limits: The employer may be one insured among many clients attached to a master program.

- Limited control: The PEO often controls carrier relationships, claim reporting flow, and some practical decisions once a dispute starts.

- Restricted customization: Terms may be standardized across the PEO's book rather than shaped around one employer's management practices, state footprint, or claim profile.

A CFO should read that as concentration risk. An HR director should read it as operational risk during a sensitive employee matter.

Practical rule: Bundled EPLI should be treated as a starting point for diligence, not proof that the employer's exposure has been solved.

Being covered isn't the same as owning coverage

The most important distinction is whether the company is merely participating in the PEO's policy or owns a standalone policy in its own name. Ownership affects control. It also affects visibility into exclusions, reporting obligations, and access to defense strategy.

A standalone policy usually gives the employer a direct relationship with the insurer and broker. That doesn't automatically make it better. It does make it clearer. The company can review endorsements, negotiate terms, and align coverage with its own risk profile instead of relying on a broad master structure designed to work across many clients.

A side-by-side review of PEO master policy vs standalone policy differences helps frame the issue the right way. The question isn't “Does the PEO include EPLI?” The better question is “What control, limits, exclusions, and reporting rights does the employer lose by relying on the PEO's form?”

| Decision point | PEO master policy | Standalone policy |

|---|---|---|

| Policy ownership | Usually controlled by PEO | Controlled by employer |

| Limits | Often shared | Dedicated to employer |

| Custom endorsements | Often limited | Usually negotiable |

| Claim communication | May run through PEO | Direct with insurer |

| Fit for complex operations | Varies widely | Can be tailored |

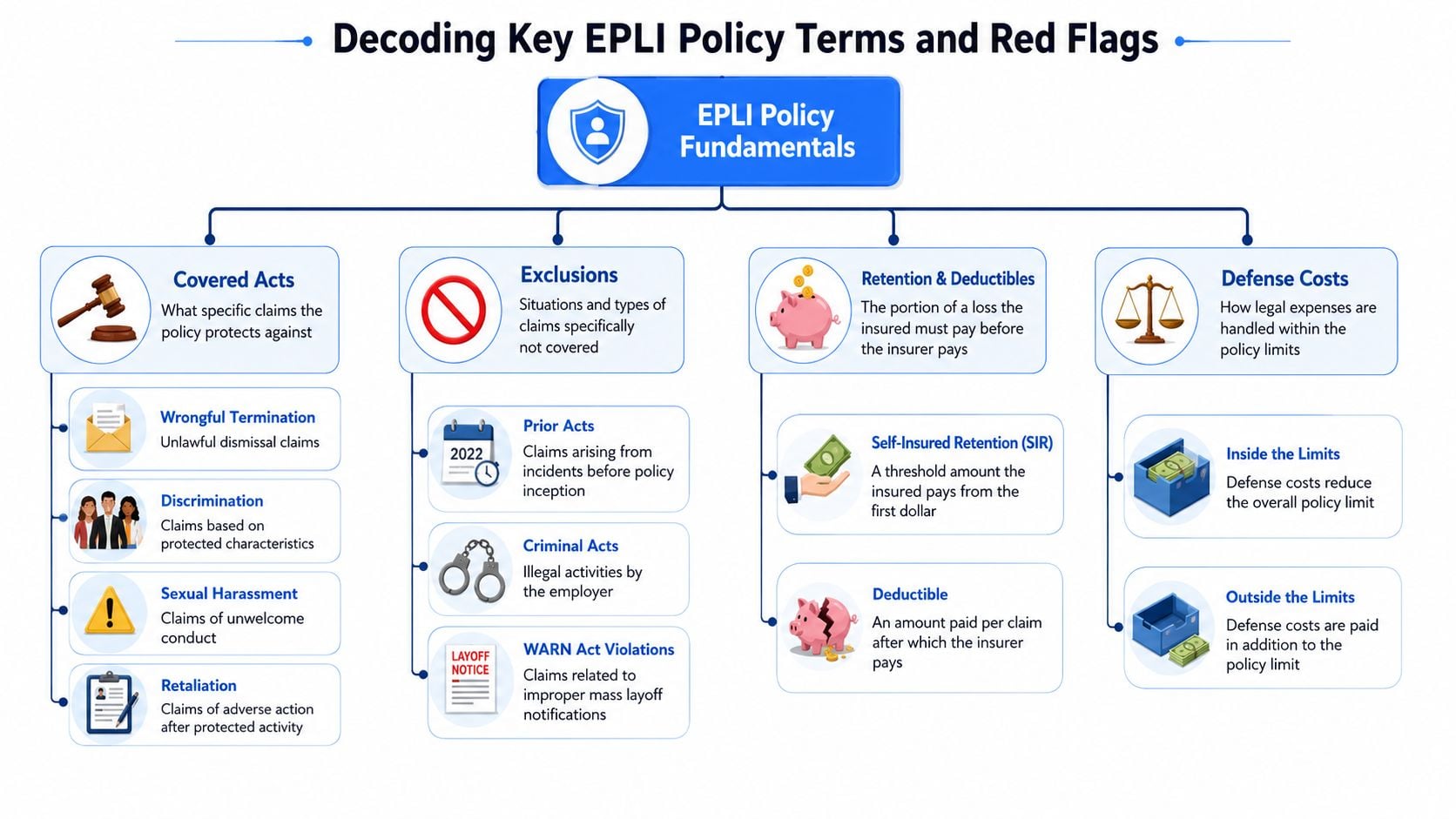

Decoding Key EPLI Policy Terms and Red Flags

A lot of bad EPLI decisions happen because the buyer focuses on premium and skips the definitions page. That's where the expensive surprises live.

Claims-made and why timing matters

EPLI policies are typically written on a claims-made basis. That means the policy in force when the claim is made and reported is what usually responds, not necessarily the policy that was in place when the underlying conduct began. IRMI also notes that EPLI commonly includes shrinking limits, meaning defense costs reduce the amount left for settlement or judgment. That explanation is laid out clearly in IRMI's definition of employment practices liability insurance.

That has two immediate implications:

- Reporting discipline matters. HR, legal, and leadership need a clear escalation process for demand letters, agency notices, and facts that could mature into a claim.

- Defense spend can erode the effective cap. A policy limit can look adequate on paper and feel inadequate after counsel has been working for months.

Red flags that deserve a second read

The most common problem language usually sits in exclusions, definitions, and defense provisions. Buyers should review these points closely:

- Prior acts language: If a complaint surfaces after onboarding to a new PEO or replacing one carrier with another, prior acts wording can determine whether there's any response at all.

- Defense costs inside the limit: If legal fees erode the cap, the finance team should model a long dispute rather than assuming the full limit remains available for resolution.

- Choice of counsel restrictions: Some policies or master programs steer claims to panel counsel. That isn't always bad, but it can create friction if the employer already has trusted employment counsel.

- Narrow wrongful act definitions: If retaliation, negligent evaluation, or failure-to-promote allegations are framed too narrowly, the policy may not respond the way the buyer expected.

A strong EPLI quote isn't the one with the shortest premium summary. It's the one the HR lead, CFO, and employment counsel can all read without guessing what happens after the first demand letter.

A useful primer outside the policy packet is PTL Insurance Associates' EPLI guide, which gives buyers a practical way to think through covered allegations and structure before going into carrier discussions.

What to verify before binding

Before accepting a quote or renewing through a PEO, buyers should confirm these operational points:

- Who reports the claim: If the manager hears about a charge on Friday afternoon, does HR report to the PEO, to broker counsel, or directly to the carrier?

- Who selects defense counsel: This affects speed, strategy, and legal spend.

- What the policy covers: A plain-language review of what EPLI insurance covers in practice helps separate broad marketing language from policy wording.

- How defense affects available limits: Finance should ask for a simple illustration showing what happens if counsel spend accumulates before settlement talks begin.

A Framework for Comparing EPLI Insurance Carriers

A buyer comparing EPLI insurance carriers shouldn't start with logos. Start with fit. The right carrier for a restaurant group with high turnover won't necessarily be the right one for a software company using AI screening tools or a distributor with multiple field locations.

The current market makes that especially important. AmTrust notes that carriers are excluding claims involving AI-driven hiring tools and algorithmic bias, with a 42% increase in rejected claims since early 2025, while 57% of SMBs now use AI in hiring, according to AmTrust's EPLI claims trends discussion. For employers using applicant tracking systems, resume filters, or ranking tools, that's no longer a niche underwriting issue.

EPLI Carrier Archetype Comparison

| Carrier Archetype | Best For | Key Feature | Potential Trade-Off |

|---|---|---|---|

| Broad national carrier | Employers that want predictable process and broad market familiarity | Standardized forms and established claims infrastructure | Less flexibility for unusual risks or specialized operations |

| Industry-focused carrier | Employers in sectors with recurring claim patterns | Underwriting often reflects sector-specific exposures | Appetite may be narrower outside target classes |

| PEO master-policy carrier | Employers prioritizing bundled simplicity | Administrative convenience inside the PEO relationship | Shared structure and less policy control |

| Standalone specialty market | Multi-state or more complex employers | Greater room for tailored endorsements | More diligence required during placement and renewal |

Four pillars that matter more than price

Financial strength

EPLI claims can take time to develop and resolve. Buyers should ask whether the carrier has the balance sheet and discipline to handle a contentious matter without creating unnecessary friction. This is less about marketing and more about staying power.

Claims handling philosophy

Some carriers manage claims more directly. Others rely heavily on outside administrators or tightly managed panel arrangements. The practical question is simple: when an agency charge arrives, who responds, how quickly, and how collaborative are they with the employer's legal and HR teams?

Underwriting appetite

Carrier distinctions become more pronounced. A carrier that likes healthcare staffing may not like light manufacturing. A carrier comfortable with a single-state workforce may react differently to a company hiring in several jurisdictions with different leave, accommodation, and retaliation standards.

Policy structure

Herein lie the crucial distinctions. Endorsements, third-party coverage, defense arrangement, and exclusions can change the usable value of the policy more than a modest premium difference will.

Buyers should ask carriers one uncomfortable question early: “What claim pattern are you trying not to insure?”

That question often surfaces the hidden exclusions faster than a polished proposal does.

A practical budgeting step is to pair the policy review with a look at how EPLI insurance cost is typically framed in a buying process. Cost still matters. It just shouldn't be the first or only filter.

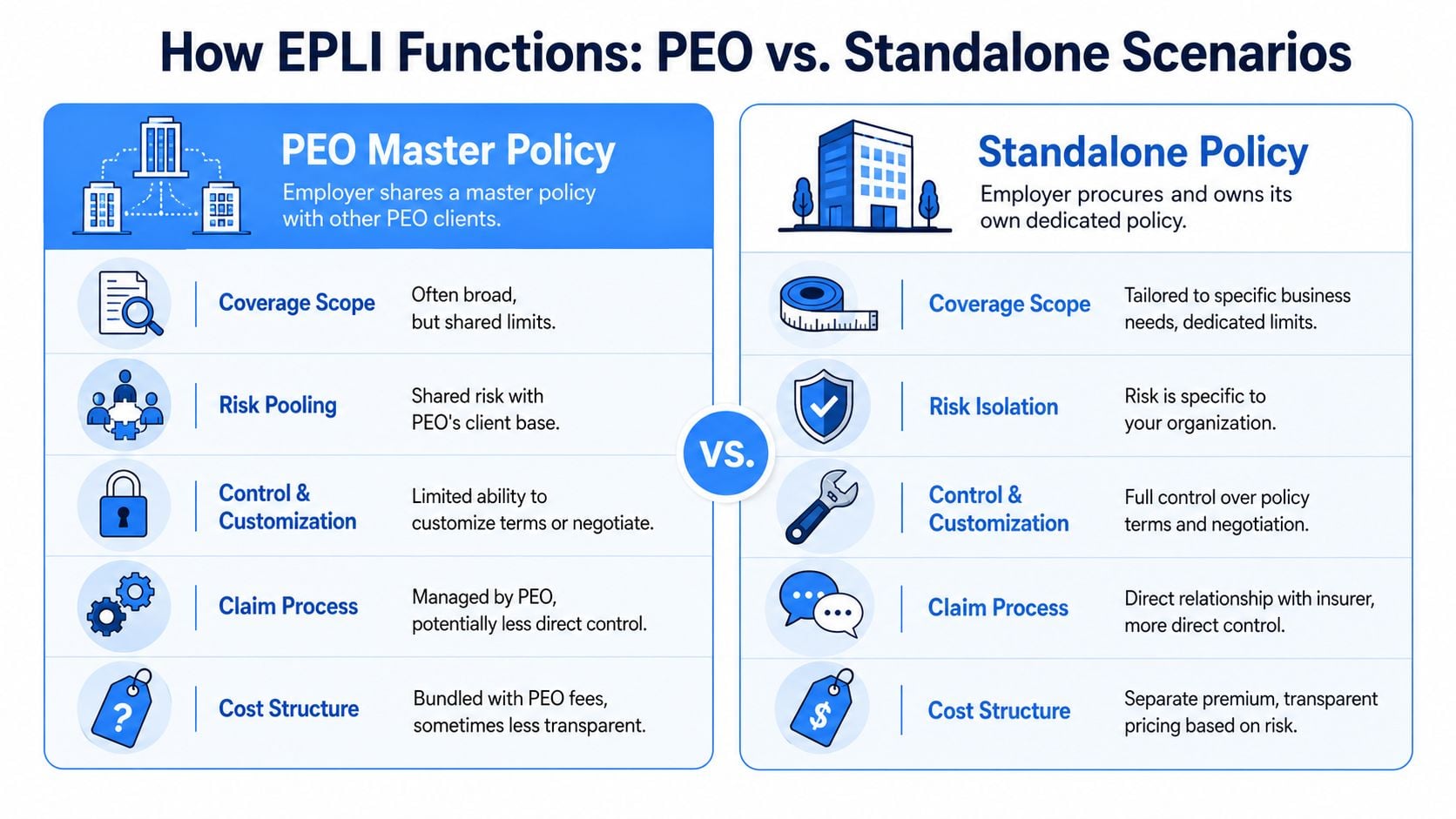

How EPLI Functions in PEO vs Standalone Scenarios

Most employers understand the theory once they see how claims unfold. The difference between a PEO master policy and standalone EPLI becomes obvious under pressure, not at renewal.

Scenario one multi-state retaliation claim

A company with 150 employees operates in three states. A director terminates a manager after an extended dispute involving leave administration, performance warnings, and a complaint about unequal treatment. The former employee alleges wrongful termination and retaliation. The claim touches records, manager training, policy consistency, and state-specific leave obligations.

That's exactly where many employers discover the limits of a generic bundled arrangement. Zurich notes that buyers often don't understand when a PEO's default EPLI is insufficient for multi-state employers facing complex FMLA or retaliation claims, and that 68% of EPLI claims stem from wrongful termination and harassment across state lines, as discussed in Zurich's EPLI overview.

Under a PEO master policy, the employer may face several practical constraints:

- Shared policy mechanics: The employer may not know how much aggregate capacity has already been affected elsewhere in the program.

- Less control over claim posture: The PEO may be the first point of contact with the carrier.

- Potential mismatch on jurisdictional detail: The employer's three-state footprint may involve nuances not central to the master form.

Under standalone coverage, the same employer can usually align reporting, endorsements, and counsel strategy around its own operating map. The company also gets a direct line of accountability between broker, insurer, HR lead, and legal team.

Scenario two third-party harassment allegation

A services business sends employees into customer locations every day. A client alleges that one of the company's supervisors engaged in discriminatory or harassing conduct toward a non-employee on-site. HR may assume the claim falls under EPLI because the allegation sounds employment-related. That assumption can be wrong.

Some base EPLI forms focus on employee claims and leave gaps for allegations brought by customers, vendors, or other non-employees. In a PEO setting, that issue can stay hidden because the buyer never negotiated the endorsement set directly. If the master policy doesn't include the right third-party feature, the employer may be defending the matter without meaningful insurance support.

A standalone policy with the right endorsement is far more likely to make that risk visible during placement. That doesn't guarantee every allegation is covered. It does mean the company had the opportunity to purchase for that exposure intentionally.

What changes in the real world

The contrast isn't abstract. It shows up in ordinary claim tasks:

| Claim task | PEO master policy | Standalone policy |

|---|---|---|

| Initial reporting | Often through PEO channel | Direct to insurer or broker |

| Policy wording access | Sometimes limited or delayed | Usually direct and complete |

| Endorsement tailoring | Constrained by program design | Negotiable around operations |

| Counsel selection influence | Often narrower | Usually more room to negotiate |

| Visibility into limit structure | Less transparent | More transparent |

For employers trying to map those trade-offs before renewal, this explanation of PEO employment practices liability structure is a useful checkpoint.

If a claim would materially affect operations, the employer should know before renewal who reports it, who controls it, and whether the policy was built for that exact fact pattern.

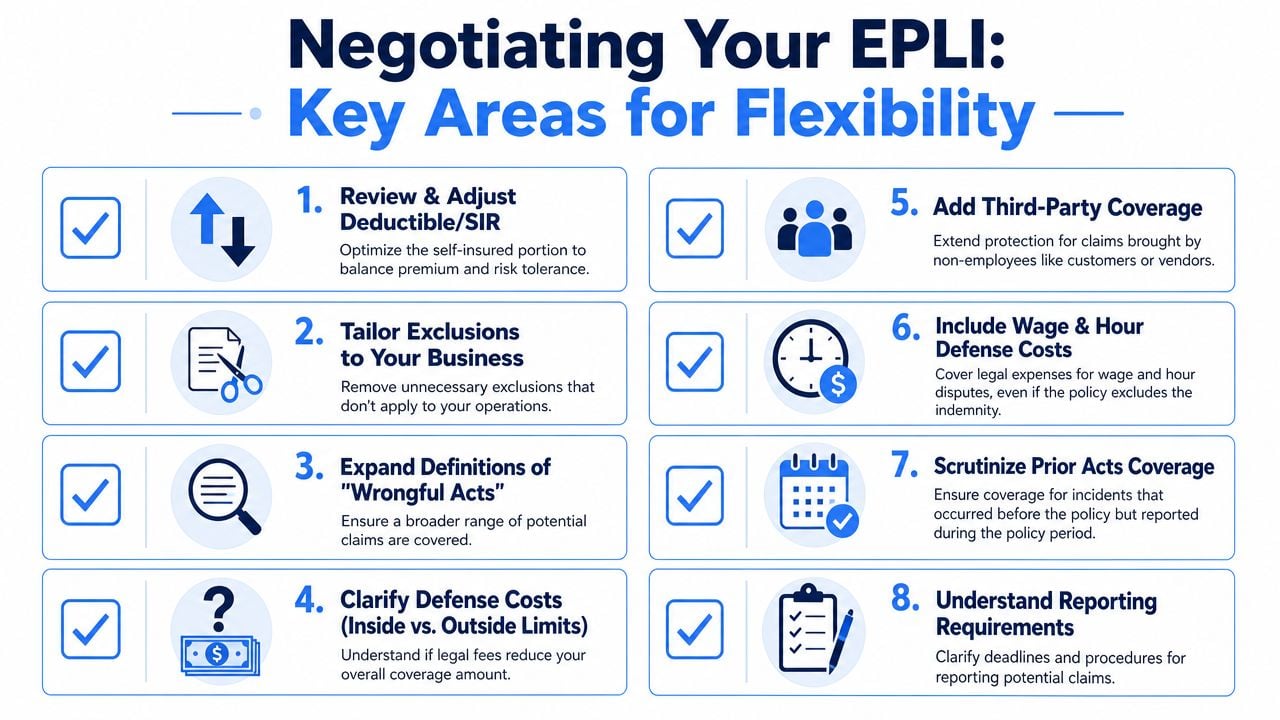

Negotiating Your EPLI Coverage and Terms

Too many buyers treat EPLI as filed-rate insurance. It isn't. Terms are often more flexible than the first quote suggests, especially when the employer has a solid handbook, documented training, disciplined performance management, and a clean reporting process.

Endorsements worth asking for

One of the most valuable negotiations involves third-party coverage. AmTrust explains that many national carriers offer an enhanced optional endorsement protecting against allegations from non-employees such as clients or vendors, and that this enhanced tier can include coverage for punitive damages that are otherwise typically excluded, as outlined in AmTrust's EPLI product overview.

That matters for employers in hospitality, healthcare, staffing, retail, field services, and any business where workers regularly interact with customers or partner personnel.

Other negotiation points deserve equal attention:

- Defense arrangement: Ask whether defense costs sit inside limits and whether the company can negotiate more flexibility around counsel.

- Prior acts coverage: This becomes critical during PEO transitions, acquisitions, and leadership turnover.

- Definition of wrongful acts: Broader wording can avoid disputes over whether the alleged conduct fits the insuring agreement.

- Reporting language: HR needs practical notice procedures, not vague language that creates technical reporting failures.

What actually improves leverage

Carriers respond to discipline. An employer negotiating EPLI should bring underwriting support, not just requests.

Useful items include:

- A current handbook: Recent policy updates help underwriters assess management controls.

- Training records: Documentation on harassment prevention, investigations, and manager escalation supports the risk story.

- Multi-state compliance notes: If the company operates in several jurisdictions, summarize how leave, accommodations, and discipline practices are handled consistently.

- Claim narrative: If there was a prior issue, explain corrective action clearly and directly.

A company also shouldn't ignore the PEO agreement itself. Liability allocation, indemnification wording, and insurance responsibilities can narrow or expand what's realistically recoverable when a dispute arises. Buyers reviewing those terms often benefit from a more detailed look at PEO indemnification negotiation tips.

Negotiation lens: The goal isn't to buy the broadest wording in the abstract. It's to buy the wording that matches how the company hires, manages, disciplines, and serves customers.

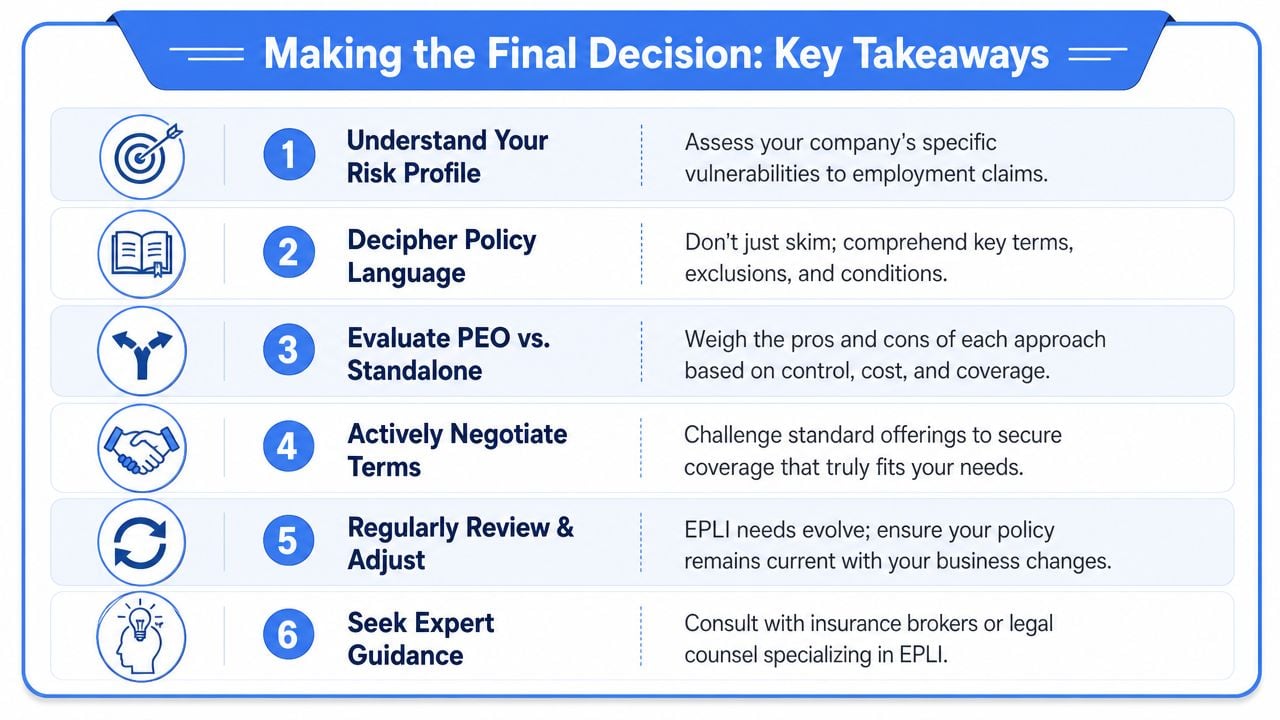

Making the Final Decision Key Takeaways

The final decision usually comes down to one business judgment: is EPLI being purchased for convenience or for claim performance?

For many employers in a PEO, the bundled answer is adequate until the workforce becomes more distributed, manager decisions become more complex, or customer-facing risk increases. At that point, standalone coverage often deserves a serious side-by-side review. The issue isn't distrust of the PEO. It's that insurance structure and service structure solve different problems.

Berkley Asset Protection states that a business is 3 times more likely to be sued by an employee than to experience a fire, which is a useful reminder from Berkley's EPLI facts page. Most companies would never accept vague answers about property coverage, limits, and claim control after a fire. Employment risk deserves the same standard.

Three actions to take next

- Review the actual policy structure: Ask whether the company is an insured under a master program or the owner of its own coverage, and request the full wording and endorsements.

- Model the claim path: Finance, HR, and legal should walk through who reports a claim, who appoints counsel, and how defense costs affect available protection.

- Pressure-test the exclusions: Focus on multi-state claims, third-party allegations, reporting requirements, and any hiring technology that could create a modern coverage gap.

The clean takeaway is straightforward. EPLI insurance carriers shouldn't be evaluated as interchangeable names behind a PEO bundle. They should be evaluated based on control, exclusions, claim handling, and how the policy performs when the allegation is serious enough to disrupt leadership time and financial planning.

PEO arrangements often look straightforward until the liability language, master-policy structure, and bundled insurance assumptions are tested. PEO Metrics helps employers compare PEO options, identify contract and coverage trade-offs, and negotiate stronger terms before renewal or transition decisions lock in risk.