A common trigger for revisiting the retirement plan is growth. A company gets to 40, 60, or 150 employees, recruiting gets harder, and candidates start asking about the 401(k) before they ask about PTO. The business may already have payroll in place, maybe even a broker and an HR manager, but the retirement plan still feels stuck between “too small to get good economics” and “too exposed to manage casually.”

That's where the peo retirement plan conversation usually starts. Not because a PEO is automatically the right answer, but because it changes the structure of the problem. Instead of one employer carrying plan administration, compliance work, and vendor influence on its own, the employer joins a larger framework that can make retirement benefits more accessible, more standardized, and easier to run.

Most articles stop there. They focus on convenience and ignore the contract. A CFO shouldn't. The retirement plan inside a PEO can solve real problems, but it can also create future friction if the fee structure is opaque, the fiduciary language is weak, or the exit process is an afterthought.

Table of Contents

- Why Your Standalone 401(k) Is Holding You Back

- What Is a PEO Retirement Plan

- PEO Plan vs Standalone 401(k) A Detailed Comparison

- Understanding Fiduciary Liability in a PEO Model

- The True Cost of a PEO Retirement Plan

- How to Evaluate a PEO's Retirement Offering

- Negotiating Terms and Planning Your Exit Strategy

Why Your Standalone 401(k) Is Holding You Back

The usual problem isn't that employers don't want to offer retirement benefits. It's that a standalone plan asks a small or midsize company to act like a retirement specialist. That means vendor selection, fee review, plan governance, payroll coordination, annual testing, notices, filings, and ongoing fiduciary attention. For a lean HR and finance team, that's a lot of surface area.

The access gap is real. Among companies with 10 to 49 employees, 52% of PEO users offer a retirement plan, compared with 23% of companies that don't use a PEO, according to NAPEO industry research data. That's why the peo retirement plan has become a serious option for employers that need to compete for talent without building retirement-plan expertise internally.

The three blockers that usually stall a standalone plan

- Administrative drag: Someone has to own contribution timing, census data, plan notices, vendor questions, and annual compliance activity. In many companies, that “someone” is already overloaded.

- Liability concern: Finance leaders understand that retirement plans create fiduciary exposure, but they often don't get a clean explanation of what can be outsourced and what can't.

- Cost uncertainty: A low quoted admin fee can still hide expensive funds, service add-ons, or change-order style charges later.

Practical rule: If leadership is hesitating because the 401(k) feels too expensive, too risky, or too operationally messy, the issue usually isn't desire. It's structure.

That's also why fee literacy matters. Employers comparing a PEO plan to a standalone design should understand the full amount employees pay inside the plan, not just what the employer sees on an invoice. For a useful outside perspective on participant-level costs, this overview of understanding 401k hidden fees and protection helps frame the questions worth asking.

A PEO won't fix every retirement-plan issue. But for many growing employers, it removes the exact barriers that kept the standalone plan from working in the first place.

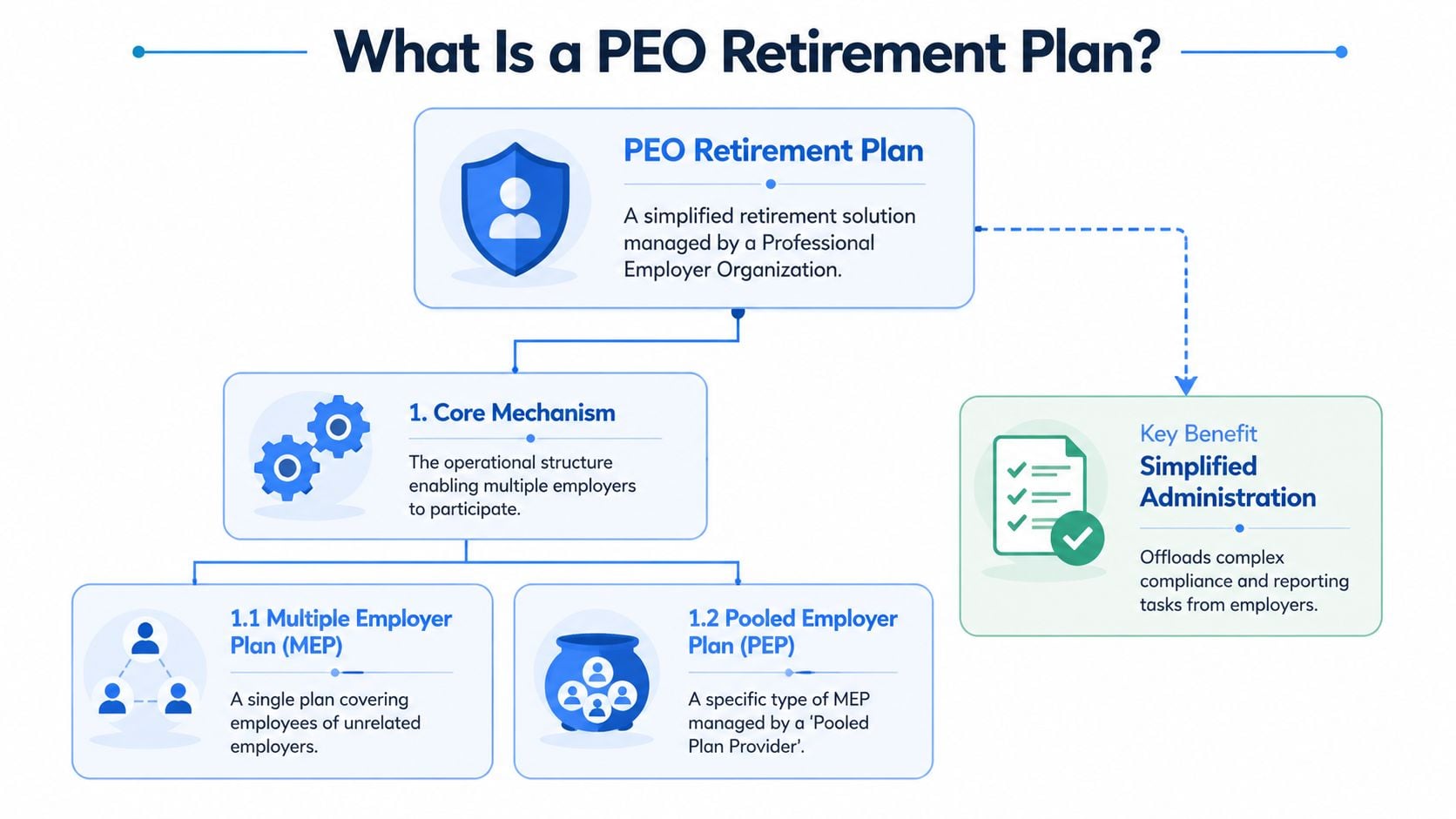

What Is a PEO Retirement Plan

A peo retirement plan is usually a retirement arrangement sponsored through the PEO's broader benefits platform rather than through one employer's standalone plan. In practice, that often means a Multiple Employer Plan (MEP) or related pooled structure where multiple unrelated businesses participate in one larger plan.

How the pooled structure works

The easiest way to think about it is group purchasing. One 60-person company on its own has limited influence. A PEO that aggregates many client companies brings a much larger participant base to recordkeepers, investment providers, and administrators. That pooled scale is what changes the economics and the operating model.

Instead of each employer building its own retirement-plan stack from scratch, the PEO provides a shared framework for plan administration, payroll integration, and compliance support. The employer still makes key business decisions such as whether to participate and what contribution approach fits its workforce, but much of the plan infrastructure sits with the PEO and its partners.

Why scale matters

Scale is not just a pricing story. It affects service levels, plan design discipline, and the ability to standardize processes across many employers. The PEO industry serves 173,000 small and medium-sized companies employing 4 million people, and within that ecosystem retirement plans are a foundational service. Client companies also grow 7 to 9 percent faster and see 10 to 14 percent lower employee turnover, according to NationalPEO PEO facts.

That doesn't mean the retirement plan alone creates those outcomes. It does mean retirement benefits are part of a much broader operating model that many growth-oriented employers already use.

For buyers reviewing structures, one useful starting point is a focused look at PEO 401(k) services, especially when comparing a bundled PEO retirement arrangement against a standalone redesign.

The right analogy isn't “outsourcing a benefit.” It's joining a larger plan architecture that can negotiate, administer, and govern at a scale a single employer usually can't reach alone.

The catch is that pooled efficiency often comes with less customization. That trade-off becomes much clearer in a direct side-by-side comparison.

PEO Plan vs Standalone 401(k) A Detailed Comparison

A PEO plan and a standalone 401(k) solve different problems. One is built for efficiency, economies of scale, and reduced internal burden. The other is built for control.

PEO Retirement Plan vs. Standalone 401(k)

| Feature | PEO-Sponsored Plan (MEP/PEP) | Standalone 401(k) |

|---|---|---|

| Administrative Burden | Much of the operational work sits with the PEO and its providers | The employer coordinates vendors, filings, testing, and plan administration |

| Fiduciary Liability | The PEO typically assumes significant co-sponsorship and administrative responsibility | The employer carries more direct plan oversight and governance responsibility |

| Cost Structure | Shared plan economics can lower certain fees | Costs may be higher and less predictable at smaller scale |

| Investment Options | Often curated and standardized across the pooled plan | Usually more customizable by the employer |

| Implementation | Usually easier if payroll and HR are already inside the PEO | Can require more project management across separate vendors |

| Exit Flexibility | Leaving can be more complex because the employer is exiting a pooled structure | Changing TPAs or providers is often more straightforward |

Where a PEO plan usually wins

The strongest case for a PEO plan is operational relief. Employers that don't want retirement administration to become a permanent internal project often prefer the PEO structure because it reduces the number of moving parts. Payroll, eligibility, contributions, and compliance support often sit closer together.

A PEO model can also make matching strategy easier to communicate because the retirement plan is folded into a broader benefits package. When employers review match design, participant behavior, and education strategy, practical resources such as Financial Footwork's 401k matching tips can help frame what employees value.

Another advantage is visibility. Employers that are trying to compare a current PEO's benefit pricing against the market should review broader plan packaging, not just retirement in isolation. In these situations, PEO benefit plan transparency issues often become part of the retirement discussion too.

Where a standalone plan still has the edge

A standalone plan still makes sense for employers that want direct control over plan design, investment lineup, and vendor relationships. That can matter for companies with unusual workforce demographics, specific governance standards, or an internal finance team that wants a custom setup.

Standalone plans also tend to be cleaner when a company expects major structural change. Mergers, acquisitions, spinouts, or a likely switch away from the PEO can all make portability more valuable than convenience.

A CFO shouldn't ask which model is “better.” The better question is which burden the company wants to carry: more administration now, or more constraints later.

The wrong decision usually happens when a company buys the PEO model for convenience and never stress-tests the contract for flexibility.

Understanding Fiduciary Liability in a PEO Model

A CFO signs with a PEO expecting fiduciary relief. Twelve months later, an employee complaint, a late remittance issue, or a messy divorce order exposes the part many buyers miss. Liability shifted, but not all of it, and not always in the way the sales team implied.

What shifts to the PEO

In a well-structured PEO retirement arrangement, the PEO or its appointed fiduciaries may take responsibility for core plan functions such as Form 5500 filing, annual audit coordination, investment menu oversight, and day-to-day compliance administration. That reduces the employer's operational burden and usually gives the finance team fewer retirement tasks to manage internally.

That matters in practice. If a qualified domestic relations order lands on your desk in a standalone plan, your team may need to coordinate counsel, the recordkeeper, and plan interpretation while keeping deadlines straight. In a stronger PEO model, that workflow is already defined, with named parties handling review and processing.

The operational relief is real. The legal relief depends on the contract.

What the employer still owns

The employer still has meaningful fiduciary and operational duties. Payroll must be accurate. Contributions must be remitted on time. Eligibility data must be correct. The company also has to decide whether joining the PEO-sponsored plan was prudent in the first place, and whether staying in it continues to be prudent.

That last point gets ignored too often. A PEO can accept fiduciary roles, but it does not erase the employer's duty to select and monitor the provider competently. If fees rise, service slips, or the plan design stops fitting your workforce, the employer cannot hide behind the co-employment structure.

For employers with teams in several states, retirement oversight also connects to broader benefits compliance. This guide to navigating state-specific employee benefit mandates is a useful reminder that retirement administration rarely sits alone.

The negotiation point buyers miss

The question is not whether the PEO says it is a fiduciary. The question is which fiduciary role it accepts, which duties stay with the employer, and what happens when something goes wrong.

Ask for the service agreement, adoption agreement, and any fiduciary acknowledgments in one package. Then look for plain-English answers to four issues:

- Who is the named fiduciary for investment selection and monitoring

- Who decides on plan amendments and eligibility rules

- Who is responsible for correcting operational errors

- Who pays for correction costs, penalties, and legal review if the error started with bad payroll or census data

If those answers are vague, the liability transfer is limited.

Buyers that want a clearer allocation of responsibility should review this analysis of benefit fiduciary liability under a PEO model before signing. The wording matters. “Assist with,” “support,” and “coordinate” are service words, not liability words.

Plan for the exit before you join

Fiduciary risk is not only a signing issue. It is also an exit issue.

If the company leaves the PEO, determine in advance how participant balances move, who handles blackout notices if needed, how payroll files are mapped to the new recordkeeper, and who bears responsibility for transition mistakes. I have seen clean exits and expensive ones. The difference was usually in the contract, not in the sales presentation.

A prudent buyer treats fiduciary review as part legal analysis and part negotiation strategy. If a PEO wants credit for taking liability off your plate, it should state that clearly, accept specific duties in writing, and explain the handoff process if you decide to leave.

The True Cost of a PEO Retirement Plan

A CFO signs with a PEO because the retirement line item looks lower than the company's standalone 401(k). Twelve months later, the bill is still acceptable. The surprise comes during renewal or exit, when conversion fees, payroll remapping work, participant notice requirements, and asset-transfer support start showing up as separate costs.

The total expense of a peo retirement plan involves more than the stated admin fee. It is the full economic package over the life of the relationship, including what you pay to join, what employees pay while you are in the plan, and what it costs to leave cleanly.

Start with the pricing you can actually verify

Request the full retirement fee schedule and match it to the service agreement. Buyers need to see employer-paid administration, participant recordkeeping charges, investment expenses, loan and distribution fees, and any charges tied to onboarding or plan changes. If retirement pricing is blended into a broader admin bundle, force the provider to isolate it.

That step matters during negotiation. A quote that looks competitive can still be expensive if the PEO has broad discretion to reprice at renewal or pass through vendor increases without a cap.

The expensive items are often outside the headline fee

PEOs can reduce costs through scale. In practice, that may mean lower administrative pricing and access to less expensive share classes than a smaller standalone plan can usually get on its own. Those savings are real, but they do not answer the harder question: who pays for the frictions around implementation, exceptions, and exit?

I tell finance teams to model four buckets:

- Employer-paid administration

- Participant-paid investment and transaction fees

- Implementation and conversion costs

- Exit-related charges and internal labor

The fourth bucket gets missed often.

A company leaving a PEO may face recordkeeper transition fees, payroll file rebuilds, legal review of the plan conversion, blackout notice administration, and weeks of internal cleanup between HR, payroll, and finance. Even when the hard-dollar invoice is modest, the staff time is not. If payroll has to hand-correct census data or reclassify compensation fields for a new provider, the cost shows up in labor hours and avoidable error risk.

Renewal leverage matters as much as starting price

The first-year proposal is rarely the whole story. A practical review asks three negotiation questions up front:

- What retirement fees can increase at renewal, and by how much

- Which participant fees can be changed without employer approval

- What support is included if the company exits in year two or year three

Those terms affect total cost more than a small difference in the initial admin quote. I have seen employers save money in year one and give it back at renewal because the agreement gave them no pricing protection and no clear exit assistance.

Build the cost model before you sign

A usable TCO model should test at least two scenarios: staying with the PEO for three years, and leaving after 12 to 24 months because of M&A activity, a headcount change, or a decision to bring HR administration back in-house. If the economics only work when everything goes right and the company never leaves, the pricing is weaker than it looks.

Broader PEO benefit markup transparency review work also helps here. Retirement charges are often part of the same pricing structure that obscures margins in other benefit lines.

The cheapest proposal is often the one with the most missing detail.

How to Evaluate a PEO's Retirement Offering

A finance team usually finds gaps in a PEO retirement offer after the sales meeting, when someone asks three basic questions. Who is taking fiduciary responsibility. What can fees do at renewal. How hard is it to leave if the relationship stops working.

That is the right standard for review. Treat the retirement plan like vendor diligence, not like a benefits demo.

Questions that belong in every finalist review

Start with documents, not presentations. A polished meeting matters less than what the PEO will commit to in the service agreement, adoption paperwork, fee schedule, and transition materials.

Focus on five areas:

- Fiduciary status: Ask the PEO to specify, in writing, which party is handling plan administration, investment oversight, and day-to-day compliance tasks. If the answer depends on side letters, carveouts, or vague references to shared responsibility, legal and finance should mark that as a risk item.

- Investment menu and constraints: Request the full fund lineup, expense ratios, any managed account or advice fees, and the process for changing the menu. The point is not to get the longest list of funds. The point is to confirm that participants have a credible range of low-cost options and that the committee process is documented.

- Security and operating controls: Ask for current audit reports, payroll integration controls, contribution timing standards, and the process for correcting errors. A retirement platform can look good in a demo and still create cleanup work for payroll every pay cycle.

- Fee transparency: Get every retirement-related charge in one place, including employer admin fees, participant recordkeeping fees, investment expenses, loan fees, setup costs, correction fees, and any charges tied to a future conversion out of the plan.

- Portability: Ask for a written explanation of what happens if you exit in 12 months, 24 months, or after an acquisition. Review the timeline, blackout process, data delivery obligations, and who pays for what.

What strong answers look like

Good providers send paper. Weak providers rely on reassurance.

A solid finalist package usually includes a clean fee exhibit, sample employee notices, a clear statement of fiduciary roles, payroll file specifications, and a written transition process for both onboarding and offboarding. If any of that is "handled later," assume the work and risk stay with the employer until proven otherwise.

This review should not sit only with HR. Pull in payroll, finance, legal, and the person who will own the vendor relationship after implementation. I have seen retirement issues surface because compensation codes did not map correctly, bonus deferrals were mishandled, or eligibility rules were configured one way in payroll and another way in the plan.

One practical option is an outside contract and pricing review. PEO Metrics offers side-by-side analysis of PEO fees, terms, and operating risk, and their guide to leaving a PEO and handling the cancellation process is useful for pressure-testing how portable a retirement arrangement really is before you sign.

If finance cannot model the retirement fees and legal cannot explain the responsibility split, the offer is not ready for approval.

The right question is not whether the retirement offering looks competitive in a presentation. The question is whether your company can defend the decision after a fee increase, an operational error, or an exit. That is how a CFO should evaluate it.

Negotiating Terms and Planning Your Exit Strategy

The time to negotiate the exit is before the contract is signed. That point gets ignored because implementation gets all the attention. It shouldn't.

Verified data shows that 40% to 50% of SMBs switch PEOs every 3 to 5 years, and unwinding a PEO 401(k) can involve weeks-long blackout periods, complex asset transfers, and exit fees that can be 1% to 3% of assets under management, according to PEO.com's discussion of PEO retirement plan exit issues.

Terms worth negotiating before signature

- Portable plan language: The contract should explain how assets move if the employer exits and who is responsible for the transition steps.

- Fee controls: Renewal pricing, admin fee increases, and any transition charges should be capped or at least clearly disclosed.

- Fiduciary handoff process: The agreement should state how administrative and fiduciary responsibilities transfer out when the relationship ends.

What an exit plan should include

The company should know who will communicate with employees, how long payroll and contribution mapping will take, what the blackout process looks like, and what records must be delivered to the new provider. If those items are fuzzy during the sale, they'll be worse during a breakup.

For employers preparing to renegotiate or leave, this guide on leaving a PEO and managing the cancellation process is a useful checklist.

A peo retirement plan can be the right move. But a good retirement outcome doesn't come from the brochure. It comes from disciplined review, sharp negotiation, and a contract that works both on day one and on the day the company decides to leave.

Companies comparing or renegotiating a PEO don't need more sales language. They need a clear view of fees, benefits, contract terms, and exit risk. PEO Metrics helps HR, finance, and leadership teams evaluate PEO options side by side, benchmark pricing, and identify negotiation points before signing or renewing.