A finance leader signs a PEO agreement to reduce HR admin, stabilize benefits, and simplify payroll. Months later, unemployment charges start surfacing in board discussions, renewal pricing, or exit planning. That’s when a key question emerges. Who bears the risk under PEO unemployment insurance?

For companies with 10–2,000 employees, that question matters more than most sales decks admit. State unemployment tax rarely breaks a deal on day one. It becomes expensive later, when a termination wave, a disputed claim, or a PEO exit exposes how little control the client kept over claims handling, attribution, and future experience rating.

The mistake is treating unemployment insurance like a back-office line item. It isn’t. It’s a long-tail liability with contract language attached.

Table of Contents

- The Hidden Liability in Your PEO Agreement

- How PEOs Take Over Your State Unemployment Tax

- Comparing The Three PEO Unemployment Liability Models

- Your Experience Rating After a PEO Relationship

- Managing Unemployment Claims Within a PEO

- Contract Red Flags and Negotiation Points

- Your Action Plan for PEO UI Evaluation

The Hidden Liability in Your PEO Agreement

A common scenario goes like this. A company outsources payroll, HR admin, and tax filing to a PEO. The leadership team assumes unemployment is now “handled.” Then an ugly surprise hits. It may be a renewal increase tied to claims activity, a chargeback allocation, or a post-termination dispute over who should absorb the cost of a former employee’s claim.

That surprise doesn’t happen because unemployment claims are rare. They’re constant. As of the week ending June 27, 2026, U.S. initial unemployment claims were 215,000, with continued claims at 1.747 million, according to the U.S. Department of Labor weekly data. That volume matters because every PEO is operating inside a system where claims keep moving, adjudications keep happening, and somebody pays.

What buyers usually miss

Many employers hear “co-employment” and translate it as full liability transfer. That’s too simplistic. A PEO can take over reporting and tax remittance mechanics, but the financial consequences still flow back to the client through fees, pooled-rate adjustments, claim allocation language, or exit terms.

The risk gets worse when the agreement treats unemployment as a bundled administrative function instead of a priced liability category. That’s how HR and finance teams miss the parts that deserve real scrutiny:

- Rate structure: Is the unemployment component pooled, client-specific, or adjustable mid-term?

- Claim attribution: If a former employee files, where does that cost land economically?

- Exit treatment: What happens to the client’s own history when the relationship ends?

Practical rule: If the contract doesn’t clearly explain how unemployment claims affect current pricing and future rates, the client is carrying more risk than the sales process suggested.

A good parallel comes from broader diligence work on revealing hidden financial problems. The issue isn’t just today’s cost. It’s the liability that sits unnoticed off to the side until a stress event exposes it.

Payroll outsourcing changes the risk shape

Outsourcing payroll doesn’t erase unemployment exposure. It changes who files, who responds, and how cost gets passed through. That’s why buyers need to understand the legal and tax transfer rules behind the service model, not just the admin workflow. A useful starting point is this breakdown of PEO payroll tax liability transfer rules.

For a CFO, the takeaway is simple. PEO unemployment insurance isn’t an admin detail. It’s a contract risk. If no one models the downside before signing, the bill shows up later.

How PEOs Take Over Your State Unemployment Tax

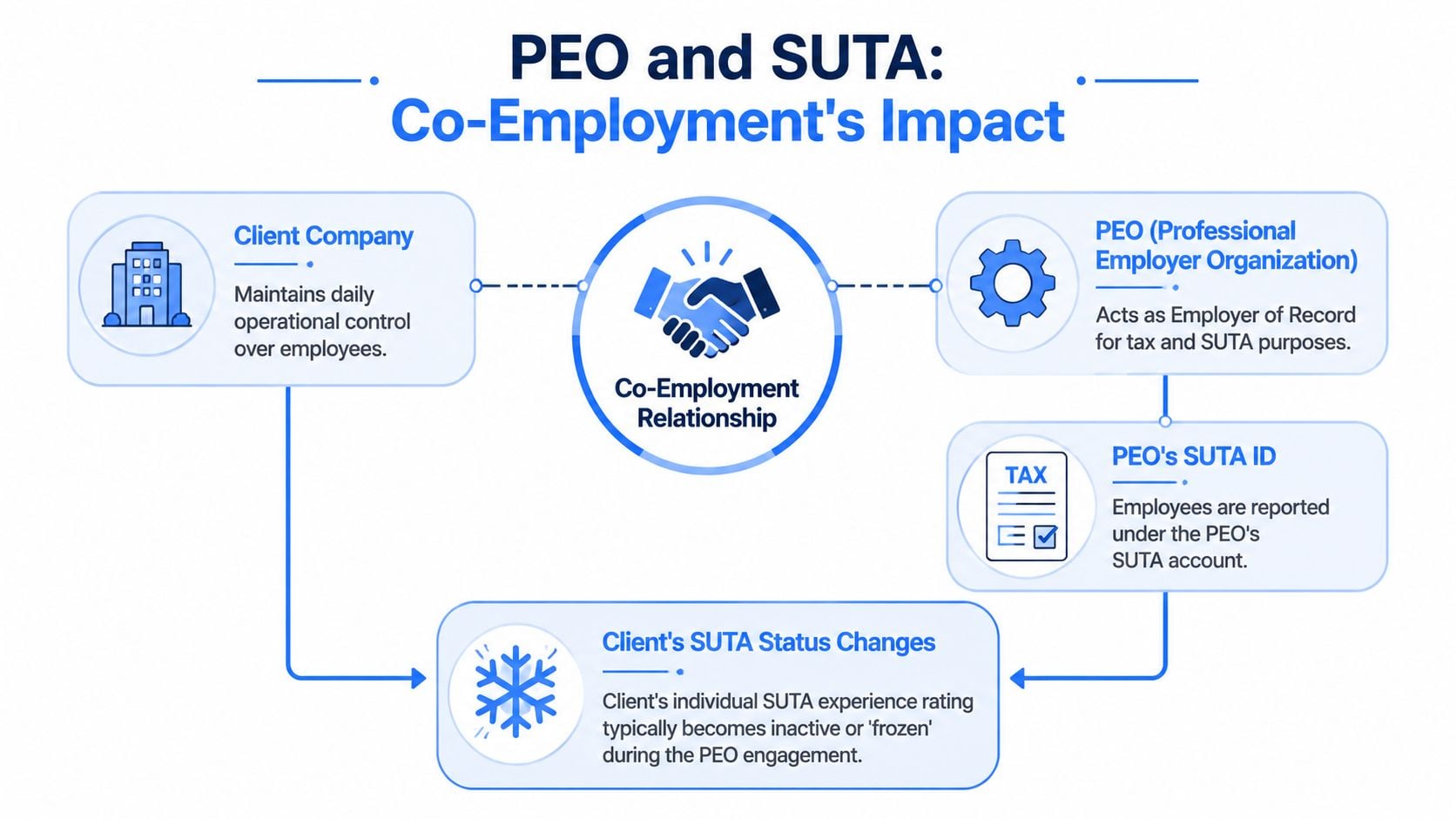

The core mechanic is straightforward. In many arrangements, the client stops operating under its own active state unemployment setup for covered workers, and the PEO reports wages and pays unemployment contributions through the PEO’s employer account. The client still manages the workforce day to day. The PEO becomes the employer of record for this tax function.

That’s why the easiest analogy is fleet insurance. A company may know the driving habits of its own team, but once those drivers move onto a fleet policy, pricing follows the fleet’s structure, claims history, and rules. State unemployment tax under a PEO often works the same way.

What actually shifts

Under most state laws, a registered PEO becomes primarily liable for UI contributions for covered employees, and the client’s UI cost is replaced by the PEO’s rate, which is calculated using the PEO’s claims history across its book of business. In some cases, a best-in-class PEO can reduce a client’s UI expenses by 10–30% compared to standalone rates, as described in the Maryland legislative analysis of PEO unemployment treatment.pdf).

That sounds attractive, and sometimes it is. But it only helps if the buyer understands what has changed:

- The reporting account changes: wages are generally reported under the PEO’s unemployment account for covered employees.

- The pricing logic changes: the client isn’t paying its old standalone rate in the same way.

- The control points change: the client may influence claims facts, but the PEO controls filing mechanics and state account administration.

Why this matters in practice

A stable employer with low turnover may benefit from a PEO’s stronger aggregate experience rating. Another employer may enter a blended arrangement and discover it’s effectively subsidizing weaker performers in the pool. The savings story depends on the model, not the brochure.

That’s also why companies evaluating broader SME payroll solutions should separate payroll convenience from unemployment cost allocation. Those are related, but they are not the same buying decision.

A buyer should ask one blunt question early: “Are unemployment costs tied to the PEO’s book, our own claim history, or a reimbursement formula?”

For a deeper look at who carries which piece of the tax burden, this overview of PEO unemployment tax liability allocation is worth reviewing before pricing discussions get too far.

The operational mistake to avoid

The worst assumption is that a lower quoted administrative fee means lower unemployment cost. It may. It may also mean the contract has broad language that lets the PEO reprice, allocate claims, or recover losses later. The account shift is real. So is the need to read the mechanics behind it.

Comparing The Three PEO Unemployment Liability Models

Not all PEO unemployment insurance arrangements work the same way. That’s where many buyers get burned. They compare one monthly fee against another without isolating the unemployment model underneath it.

Three structures show up most often in the market.

Pooled or blended rate model

In a pooled model, the PEO uses its broader unemployment profile to price the coverage or fee component. The client effectively joins the PEO’s larger risk pool.

This can work well for companies with shakier claims history, recent layoffs, or inconsistent retention. It can work poorly for stable employers that already run a tight operation and don’t want to subsidize a noisier pool.

Client-level or pass-through model

In a client-level setup, the PEO administers the process, but the economic result stays closer to the client’s own claims pattern or assigned treatment. The structure preserves more direct accountability, which some finance teams prefer because it’s easier to model.

The trade-off is obvious. If the client has ugly claims activity, the cost signal hits faster and more directly.

Reimbursing model

A reimbursing model is commonly discussed with organizations that don’t fit the standard contribution approach. Instead of operating through a standard rate concept, the employer reimburses claim costs under the governing rules that apply to that structure.

This can be sensible for certain organizations, but it requires discipline. Finance teams need strong controls around claim review, reserve planning, and response timing because there’s less cushion from a broad pooled mechanism.

PEO unemployment insurance models compared

| Model | How It Works | Best For | Key Risk |

|---|---|---|---|

| Pooled / Blended | Client enters the PEO’s broader unemployment rate structure | Employers seeking risk spreading or potentially lower cost through the PEO’s aggregate history | Strong employers may subsidize weaker ones |

| Client-Level / Pass-Through | Costs track more closely to the client’s own claim activity or state treatment | Employers that want cleaner cost attribution and clearer forecasting | Bad claims experience hits the client more directly |

| Reimbursing | Employer reimburses actual claim-related obligations under the applicable structure | Organizations that need a non-standard approach and can manage claim volatility | Cash flow swings and weak claim controls can get expensive |

What usually works and what usually doesn’t

A stable company with low turnover often prefers transparency over pooled optimism. If the workforce is predictable, a vague blended formula may hide more than it helps.

A company with uneven hiring cycles, branch closures, or a recent claims spike may prefer the shelter of a broader pool, but only if the agreement clearly limits repricing and explains attribution. If those terms are loose, the pool stops being protection and starts being a black box.

The model isn’t “good” or “bad” on its own. The problem starts when the PEO sells one economic outcome and the contract preserves another.

Before agreeing to any structure, buyers should map the liability path from termination to claim filing to cost recovery. This breakdown of PEO unemployment claim liability allocation helps frame the questions legal and finance should ask together.

Your Experience Rating After a PEO Relationship

A CFO approves a PEO deal based on lower unemployment costs, then gets hit two years later with a state rate that no longer reflects the company’s history the way finance expected. That is the part many sales conversations skip.

The primary question is not whether the PEO gives you a lower unemployment number during the contract. Instead, the critical question is what your company owns after the relationship ends, what claims follow you, and how the state rebuilds your account.

The overlooked financial trap

A low rate inside the PEO can hide a bad exit.

If your employees were reported under the PEO’s unemployment structure, your own experience record may not come back cleanly when you leave. In some states, your prior account history matters. In others, the transition is messier. Claims filed after termination can still tie back to wages paid during the PEO period, and that attribution can affect what you pay later under your own account or with your next provider.

I have seen buyers focus on the visible invoice discount and ignore the future tax position. That is backwards. The rate you inherit after exit can erase several years of apparent savings.

A realistic exit scenario

A company enters a pooled arrangement and enjoys lower unemployment charges while it is inside the PEO. Everyone is happy because the current spend looks better and budgeting gets easier.

Then the company exits after layoffs, a restructuring, or a provider change. Finance expects its old state position to restart with minimal friction. Instead, the company learns that its account must be reactivated, its historical data is incomplete, or claims tied to the PEO period are still affecting the economics. The savings from the contract term stop mattering very quickly when the post-exit rate comes back higher than modeled.

This is why I tell finance teams to review unemployment treatment the same way they review PEO liability insurance coverage and exclusions. The contract may look fine during the relationship and still leave you holding the long-tail cost.

Where contracts fail

The weak point is usually not an explicit promise. It is silence.

PEO agreements often say claims will be handled under applicable law, provider procedures, or the reporting structure in place at the time. That language protects the provider. It does not tell you whether your pre-PEO experience will be restored, whether claims from the co-employment period can affect your future rate, or what records you will receive to support a clean transition.

That gap matters because state unemployment tax is not just an administrative item. It is a multi-year cost driver.

If the contract does not state how experience transfers, how claims are attributed, and what data you receive at exit, assume finance is carrying the risk.

What to pin down before signing

Get clear written answers to these four points:

- Post-termination claim attribution: If a former employee files after you leave the PEO, who absorbs the economic impact?

- State account treatment: Does your unemployment account reactivate, get reassigned, or start from a new rate category?

- Exit data package: Will the PEO give you complete wage, claim, separation, and state filing records in a usable format?

- Rate continuity: If you had an established experience history before joining, what evidence will be available to support that position after exit?

A short-term rate reduction is easy to sell. Recovering a damaged or unclear experience rating after you leave is expensive, slow, and often avoidable if you force the issue before signing.

Managing Unemployment Claims Within a PEO

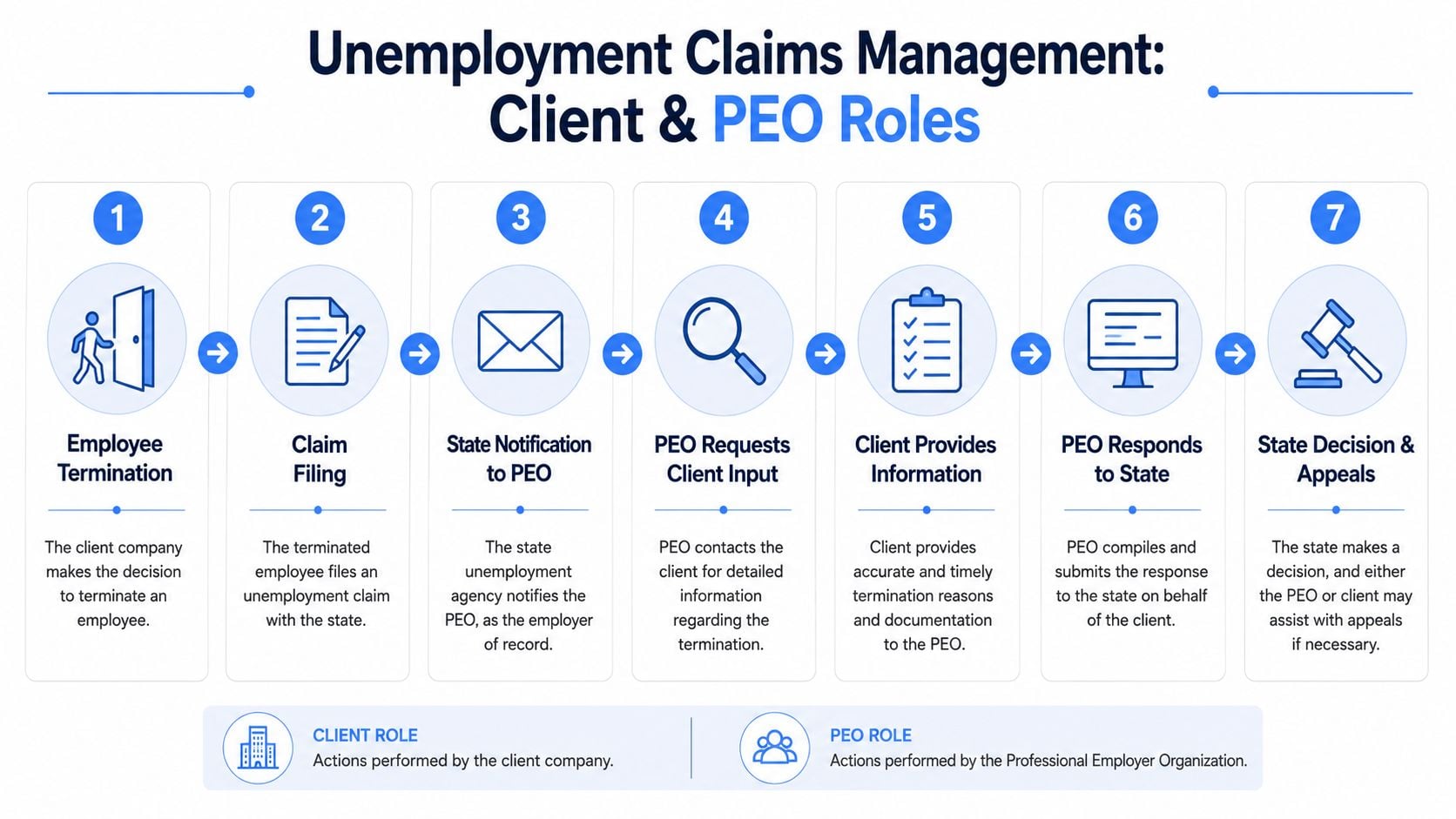

A manager fires an employee on Friday, sends a short email to HR, and moves on. Two weeks later, the unemployment notice lands with the PEO. By then, the witness notes are incomplete, the policy acknowledgment is missing, and the deadline clock is already running. That is how a routine separation turns into a paid claim.

Claims administration and claim control are not the same thing. The PEO usually handles the filing channel, state notices, and hearing logistics. The client controls the facts that determine whether the claim is defensible. If those facts are weak, slow, or inconsistent, the claim gets paid and the cost issue does not disappear just because the PEO submitted the form.

That matters more than many finance teams expect. A claim paid during the co-employment period can still matter later, especially if your own experience history comes back into play after exit. Sales presentations focus on current administration. Actual cost shows up over time if claims are mishandled, poorly documented, or impossible to trace back to the right separation record.

Who owns each part of the process

A workable process is simple, but it has to be assigned clearly:

- Client makes and documents the separation decision: managers and HR create the record through warnings, investigations, attendance tracking, policy enforcement, and the termination meeting.

- Employee files the claim: the state sends the notice to the employer of record or the reporting party on file.

- PEO manages the state response process: submission deadlines, forms, and agency communication often sit with the PEO.

- Client provides the evidence: resignation emails, misconduct records, signed policies, time records, and witness statements usually come from the client.

- Both sides prepare for appeals: the PEO may coordinate the hearing, but the client usually needs to produce the witnesses and explain the separation.

If that division of labor is fuzzy, expect avoidable claim losses.

State rules can put the PEO on the hook for reporting, not for your facts

New Jersey is a good example. State law now places defined reporting duties on PEOs for unemployment filings tied to separated covered employees. The PEO has to submit required information to the state in the required format, and penalties can apply when that reporting fails, as outlined in this update on New Jersey PEO reporting requirements.

That does not let the client off the hook. The PEO can only report what it receives. If your supervisors wait three days to explain a discharge, or send a one-line summary with no supporting documents, the PEO is filing a weak case on your behalf.

What disciplined claim handling looks like

The best client process is plain and repeatable.

- Same-day separation notice: HR sends the PEO the separation summary the day employment ends.

- Single claim file: keep the termination memo, warnings, investigation notes, policy acknowledgments, and final pay details in one place.

- One client-side owner: assign one HR or payroll lead to handle all unemployment communications with the PEO.

- Deadline tracking: log every response date, appeal date, and hearing date immediately.

- Hearing readiness: identify the manager who will testify before a hearing is even scheduled.

For teams comparing providers, this overview of state unemployment insurance handling under a PEO is a useful reference point because claim procedure still varies by state and PEO structure.

A PEO can submit the response. It cannot fix missing documentation, a careless termination record, or a manager who will not show up for the hearing.

That is the operational reality CFOs need to price correctly. Weak claim handling is not just an HR process problem. It can feed future unemployment costs long after the PEO relationship ends.

Contract Red Flags and Negotiation Points

Most unemployment problems in PEO relationships start in the contract, not in the state filing system.

The agreement decides whether the provider can reprice, pass through losses, limit responsibility, or leave the client exposed after a tax failure. A polished implementation team can’t fix bad paper.

Clauses that deserve real pushback

Some provisions should trigger immediate negotiation:

- Vague pass-through language: if the contract allows the PEO to recover “taxes, claims, assessments, or related costs” without a clear formula, the client may be buying an open tab.

- No cap on unemployment repricing: the PEO may advertise efficiency up front and preserve broad pricing discretion later.

- Weak exit wording: if there’s no commitment on data delivery, claim history records, and transition assistance, the client is exposed at termination.

- One-sided indemnity: many agreements protect the PEO against client mistakes but say very little about provider tax failures.

CPEO status is not a small detail

If a PEO is not an IRS-Certified PEO (CPEO), the client business retains full federal tax liability for unpaid UI, because the IRS does not recognize co-employment under federal tax law. Buyers should also verify that the PEO carries errors and omissions insurance and will indemnify the client for unpaid taxes, as explained in this review of PEO tax liability and CPEO status.

That issue gets buried in sales conversations because it’s uncomfortable. It should be front and center in legal review.

Questions worth asking in the redline

A serious buyer should ask for written responses and contract edits on these points:

- Who absorbs unemployment assessments economically?

- Can the provider change UI pricing mid-term?

- Will the provider cap adjustments for an initial term?

- What records will the client receive at termination, and when?

- Will the PEO indemnify for unpaid taxes and filing failures?

- Does the provider maintain the right insurance coverage?

For teams reviewing broader risk transfer language, this page on PEO liability insurance is a useful companion.

Negotiation point: If the PEO says a clause is “just standard,” that’s a reason to review it harder, not a reason to waive it through.

One more state-level check

In New York, the Professional Employer Act requires PEOs to register annually with the New York Department of Labor, maintain workers’ compensation, disability, and unemployment insurance coverage, and demonstrate financial responsibility. Failure to renew or maintain coverage can trigger strict penalties, which makes active status verification a mandatory diligence step before signing, as noted in this guide to PEOs in New York.

That kind of compliance check won’t replace contract negotiation, but it can prevent the mistake of handing tax administration to a provider with weak standing.

Your Action Plan for PEO UI Evaluation

Organizations often don’t need more marketing material. They need a short list of questions and a clean internal review before they sign, renew, or exit.

Questions to ask the PEO

Start with direct questions that force a direct answer.

- Rate model: Is unemployment priced through a pooled model, a client-specific model, or another structure?

- Claims economics: When a claim is approved, how does that affect the client financially?

- Mid-term changes: Can the provider reprice unemployment charges during the agreement?

- Exit handling: What happens to the client’s experience position when the relationship ends?

- Records: What claim files, wage records, and separation documentation will be delivered on exit?

- Tax protection: Is the provider a CPEO, and what indemnity applies if taxes go unpaid?

Internal data to review

The company should also gather its own data before any negotiation call.

- Current state unemployment setup: pull the current SUTA rate notice and account details.

- Recent claim activity: identify terminations, contested claims, and any patterns in separations.

- Cost by employee group: map turnover by location, business unit, and manager if possible.

- Exit scenarios: model what happens if the company leaves after a short term versus a longer one.

The practical takeaway

A PEO can reduce administrative burden and sometimes improve unemployment cost. It can also hide future liability behind pooled rates, soft claim attribution language, and weak exit terms.

The right evaluation lens is simple. Don’t ask only whether the PEO will handle unemployment. Ask how, under whose account, with what pricing model, and what remains with the client when the relationship ends.

That’s the difference between buying efficiency and buying a delayed liability.

Companies that want an independent second look before signing or renewing can use PEO Metrics to compare providers, benchmark pricing, and pressure-test unemployment, tax, and exit-risk terms before they become expensive surprises.