Most buyers ask the wrong question first. They ask whether PEO insurance is cheaper than going to market directly.

The better question is whether the company is buying an insurance policy, or entering a risk allocation and administration model that changes who handles payroll taxes, benefits administration, workers' compensation, and parts of employment liability. That distinction is where most expensive misunderstandings begin.

A Professional Employer Organization, or PEO, operates through co-employment. The client company still manages employees day to day, but the PEO takes on a defined set of employer functions, including insurance and benefits administration. Because PEOs pool employees from many businesses into a larger insurance group, they can sometimes negotiate stronger rates and broader coverage than a smaller employer could obtain alone. Industry research from NAPEO says businesses using a PEO grow twice as fast, have 12% lower employee turnover, and are 50% less likely to go out of business, according to Thatch's summary of PEO insurance research.

That's why what is PEO insurance isn't really a benefits-only question. It's an operating model question. It affects finance, HR, legal exposure, and how much administrative friction the company wants to carry internally. For teams trying to frame the decision more broadly as a business risk issue, outside perspectives on Lighthouse Consultants for risk advice can also help sharpen the evaluation.

For readers who want the foundation before getting into policy mechanics, this overview of what a Professional Employer Organization is is a useful starting point.

Table of Contents

- Introduction Why PEO Insurance Is Not Just Insurance

- Deconstructing the PEO Master Policy Model

- Key Coverages Within the PEO Umbrella

- Ownership and Liability Who Actually Holds the Risk

- The Financial Mechanics Premiums Audits and Total Cost

- Evaluating Contracts Common Red Flags and Negotiation Tips

- Conclusion Your PEO Insurance Evaluation Checklist

Introduction Why PEO Insurance Is Not Just Insurance

A CFO reviewing a PEO proposal usually sees a familiar line item structure. Admin fee. Benefits cost. Workers' comp. Payroll taxes. That format makes the arrangement look like a procurement exercise.

It isn't.

A PEO changes the mechanics of employment risk. Instead of the company buying and managing each coverage directly, the business enters a co-employment arrangement where the PEO handles major back-office employer functions and negotiates insurance access as part of that structure. That means the comparison isn't just premium versus premium. It's internal HR and risk capacity versus outsourced infrastructure.

The common mistake in PEO evaluations

Many finance teams treat a PEO quote like a broker quote. They compare health plan contributions, workers' comp pricing, and the monthly fee, then stop there. That misses the harder question: who is carrying operational responsibility when payroll taxes are filed, claims are opened, or an employee dispute triggers insurance response.

A PEO can reduce internal burden. It can also reduce fragmentation across vendors. But it may require the client to give up some control over plan design, carrier selection, and timing.

Practical rule: If the evaluation spreadsheet only compares premiums, the company is probably understating both contract risk and administrative value.

Why the business case is broader than benefits

The growth and retention figures often cited around PEOs matter because they suggest the arrangement is tied to broader operating performance, not just insurance shopping. As noted earlier, PEO use is often discussed as part of an HR and risk-management model rather than a stand-alone benefits product.

For decision-makers, the practical takeaway is simple:

- Treat insurance as one layer of the decision. Health, workers' comp, and EPLI matter, but so do service quality and compliance execution.

- Treat co-employment as a legal structure. The company isn't outsourcing leadership of employees. It is reallocating certain employer obligations.

- Treat the contract as a risk document. The legal terms determine how much of the marketing promise survives after a claim, renewal, or exit.

That's the frame that makes the rest of the PEO insurance discussion useful.

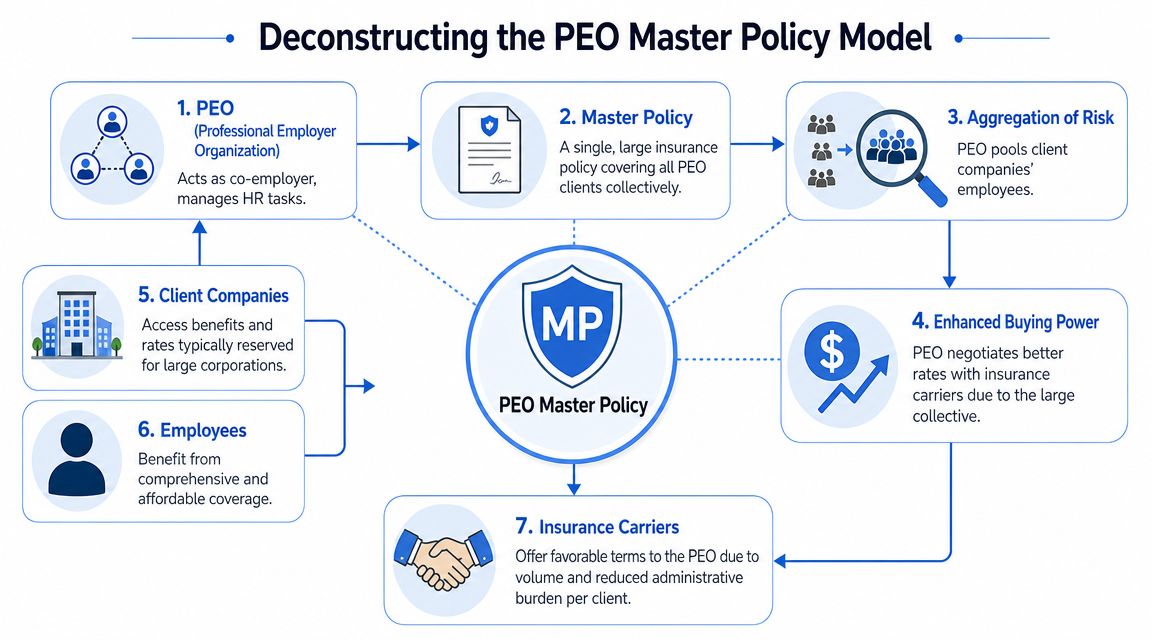

Deconstructing the PEO Master Policy Model

When buyers hear “master policy,” many assume the PEO is acting like an insurance carrier. That's usually the wrong mental model.

In most arrangements, the PEO doesn't sell the insurance itself. It sponsors or administers access to group coverage, and the insurance is still backed by an actual carrier. The distinction matters because it affects carrier choice, policy ownership, and what the client can and can't customize. PeopleKeep's explanation of the insurance relationship captures this well.

What the master policy actually means

The cleanest way to think about a PEO master policy is as a large buying and administration platform. The PEO pools employees from many client companies into one broader insurance structure. That scale can improve negotiation power with carriers and simplify administration for the client.

But pooled access comes with trade-offs.

A company buying through a broker often has more direct influence over carrier selection, plan design, and renewal strategy. A company joining a PEO usually gets access to a pre-built structure. That can be efficient, but less flexible.

Where buyers lose control

The marketing version says the company gains enterprise-style benefits. Sometimes that's true. The less-advertised part is that the company may lose authority over several decisions it would normally own.

Common examples include:

- Carrier choice limitations. The PEO may offer a set menu instead of the full market.

- Plan design restrictions. Custom carve-outs or unusual contribution structures may be harder to implement.

- Administrative dependency. Enrollment, eligibility corrections, and claims support often route through the PEO's systems and team.

That's why the service agreement matters almost as much as the policy package. Anyone reviewing the legal plumbing behind this arrangement should also understand master services agreements, because the PEO contract often functions as the operational rulebook for insurance access.

The question isn't only “What benefits are offered?” It's “Who controls the infrastructure those benefits sit on?”

PEO versus broker in plain terms

A broker helps the company shop and place insurance that the company generally owns directly. A PEO gives the company access to insurance within a co-employment framework that the PEO helps sponsor and administer.

That difference changes the buyer's advantage.

For a deeper breakdown of how pooling and control work together, this guide to PEO master policy risk pooling mechanics is worth reviewing.

Key Coverages Within the PEO Umbrella

Once the master policy structure is clear, the next question is practical. What coverages are usually sitting inside the PEO umbrella, and how do they behave differently than direct policies?

The answer varies by provider and contract, but four categories usually drive the decision: workers' compensation, employment practices liability insurance, employee benefits, and ancillary or business-side liability lines.

Workers' compensation

In a PEO arrangement, workers' comp is often one of the most operationally significant coverages. The PEO commonly administers coverage under its broader insurance structure, handles payroll-linked reporting, and coordinates claims processes. For the client, that can remove a lot of manual work.

It doesn't remove the need for discipline inside the company.

If a warehouse manager ignores safety procedures, or a field supervisor fails to document an incident promptly, the claim still starts with the client's work environment. The PEO may manage reporting and carrier interaction, but poor operational controls still create losses, disputes, and renewal pressure.

Employment practices liability insurance

EPLI is where many buyers assume they're more protected than they really are. The existence of a policy doesn't mean every dispute is fully absorbed, and it doesn't mean managers can treat employee relations casually.

A PEO often assumes liability for employment practices liability insurance tied to the co-employment relationship, along with workers' compensation and unemployment insurance, because it acts as employer of record for payroll tax purposes under its federal employer identification number. That allocation is outlined in World Insurance's overview of PEO liability mechanics.

The practical issue is response coordination. If a termination was poorly documented or a supervisor went off-script in an investigation, the policy may still respond, but the client's conduct shapes the quality of the defense.

For a more detailed look at this coverage layer, this article on PEO employment practices liability structure is a useful companion.

A policy can fund defense. It can't rewrite a manager's email, undo weak documentation, or fix a process that should've been escalated earlier.

Employee benefits

Health, dental, and vision are usually what bring a buyer to the table first. PEOs can use pooled scale to provide access to broader benefits options than some smaller employers can negotiate on their own.

The trade-off is governance.

A company may gain stronger group access, but lose some direct control over the plan sponsor relationship, enrollment workflows, and exception handling. That matters most when the workforce has unusual needs, the company operates in multiple states, or leadership wants very specific contribution philosophy.

General liability and related lines

General liability is often misunderstood in PEO conversations because it doesn't always sit in the same way as employee-related coverages. In some cases, it remains outside the core PEO framework or is handled separately depending on the provider's model and the client's industry.

That's why a buyer shouldn't assume “PEO insurance” means every business risk has moved into one neat bundle.

A sharper way to evaluate coverage is to ask:

- Which policies are under the PEO structure? Request a coverage schedule in plain English.

- Which risks remain directly with the company? Site operations, professional exposures, and client-contract requirements often need separate review.

- Who handles claims intake and escalation? Delays usually happen when nobody knows whether HR, payroll, the PEO, or the carrier owns the first call.

What works and what doesn't

What works is a company using a PEO to streamline employment-related coverage while keeping tight internal controls around safety, documentation, and manager conduct.

What doesn't work is assuming the PEO relationship replaces internal risk management. It doesn't. It reorganizes it.

Ownership and Liability Who Actually Holds the Risk

This is the part buyers need to get right before they sign anything. A PEO can assume meaningful responsibility, but the client company doesn't hand over all liability just because the PEO's name appears in more places.

The client still runs the workforce day to day. The PEO handles defined employer functions inside the co-employment arrangement. That split needs to be understood in writing, not inferred from a sales presentation.

The legal split in plain English

Under a PEO model, the client keeps control over hiring decisions, supervision, scheduling, performance management, and workplace conduct. The PEO becomes employer of record for payroll tax purposes and typically assumes liability for workers' compensation, unemployment insurance, and employment practices liability insurance tied to that relationship, as described in the earlier-cited World Insurance explanation.

That's a meaningful transfer of responsibility. It is not total transfer.

If a supervisor retaliates against an employee, the insurance structure may involve the PEO. But the facts that created the claim usually sit with the client's managers, policies, and documentation.

PEO versus direct insurance responsibility matrix

| Responsibility Area | Traditional Model Client Manages | PEO Co-Employment Model |

|---|---|---|

| Health plan shopping | Client or broker leads market process | PEO usually offers access within its established structure |

| Benefits administration | Client HR and broker coordinate enrollment and service | PEO commonly handles administration workflows and support |

| Workers' comp claim administration | Client reports claim to carrier or TPA directly | PEO usually coordinates claim handling inside its program |

| Payroll tax filing | Client files under its own structure | PEO files under its employer-of-record tax setup |

| Day-to-day supervision | Client manages employees | Client still manages employees |

| Workplace safety practices | Client owns implementation | Client still owns implementation, even if PEO supports policy |

| Employment decisions | Client makes decisions | Client makes decisions, often with PEO guidance |

| Contract interpretation after dispute | Client relies on direct policy terms | Client depends on service agreement plus policy structure |

For teams reviewing how these splits are addressed legally, this guide to joint employer liability allocation in PEO contracts risk mitigation strategy is worth reading closely.

Where confusion creates risk

The most common failure is operational. HR assumes the PEO is handling an issue. Finance assumes the fee covers it. Legal assumes someone else reviewed the allocation language. Then a claim arrives and everyone discovers the arrangement was narrower than expected.

Critical distinction: The PEO may hold and administer key policies, but the client still creates most employee-facing facts that trigger claims.

That's why ownership and liability need to be mapped before implementation, not after the first dispute.

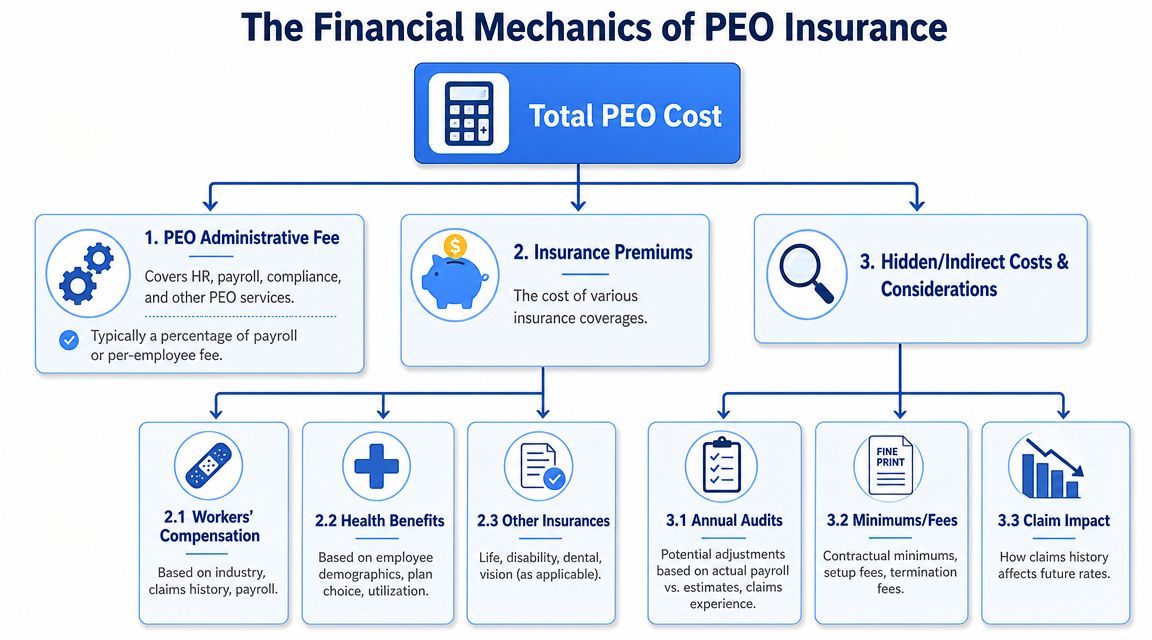

The Financial Mechanics Premiums Audits and Total Cost

A PEO quote can look clean on page one and become much messier by renewal. That's because the visible fee is only part of the economic picture.

The right question isn't whether the admin fee looks reasonable. The right question is what the company's total cost of ownership becomes after payroll changes, benefit elections, workers' comp activity, and contract rules all do their work. As the U.S. Chamber notes, PEOs can provide more predictable pricing and reduced volatility than open-market coverage, but they still commonly charge monthly fees as a percentage of payroll or a per-employee amount, so the ultimate decision is about total cost of ownership, service quality, and contract protections, not just headline savings in its discussion of PEOs versus insurance brokers.

What actually sits inside the bill

A typical PEO cost stack includes at least three buckets.

- Administrative fees. These cover payroll, HR support, compliance help, onboarding systems, and account management.

- Insurance-related charges. Workers' comp, health benefits, and other employment-related coverages may be passed through directly or blended into the pricing model.

- Variable obligations tied to payroll and headcount. As staffing changes, costs can move with it.

Many comparisons often fall short. One provider may show a lower visible fee but tighter benefit options. Another may show a higher fee but absorb more administration and claims coordination. Neither is automatically cheaper in practice.

Audits and reconciliations are where surprises appear

The company's estimated payroll and actual payroll rarely match perfectly over time. Classification changes, overtime patterns, bonuses, and seasonal staffing can all affect how costs settle out.

Workers' comp is especially sensitive to classification accuracy and payroll reporting discipline. Teams that don't understand coding exposure should spend time understanding NCCI risk fingerprints, because a classification problem can distort cost long after implementation.

A low quoted rate doesn't mean much if the payroll assumptions are wrong, the classifications are too broad, or the contract lets fees reset aggressively at renewal.

Renewal risk is usually understated

A buyer may hear that pooled pricing stabilizes costs. Sometimes it does. But stable doesn't mean static.

A company's own claims activity can matter. The PEO's broader pool can matter. Workforce growth across states can matter. Contract language on repricing can matter even more. The operational lesson is simple: initial pricing is only one chapter.

Finance teams usually get the clearest view by modeling cost in layers:

- Fixed service expense

- Benefits spend

- Workers' comp and related insurance cost

- Audit and reconciliation exposure

- Exit or transition cost if the arrangement fails

For companies that want a cleaner side-by-side of workers' comp economics across options, PEO workers comp premium benchmarking can help frame the analysis.

Evaluating Contracts Common Red Flags and Negotiation Tips

A strong PEO presentation can hide a weak PEO contract. That's where buyers lose their advantage.

The legal agreement decides how renewal works, how quickly the company can leave, what happens to outstanding claims support, and whether liability language is precise or conveniently vague. A prudent buyer treats the contract review like a risk review, not a procurement formality.

Red flags that deserve immediate pushback

Some provisions should slow the process down immediately.

- Ambiguous liability wording. If the agreement says the PEO supports compliance but doesn't clearly allocate responsibility, that gap will matter when a claim or agency issue appears.

- Restrictive termination terms. Long notice periods and expensive exit mechanics can trap a client in a poor service relationship.

- Broad repricing language. If the provider can reset fees or insurance charges with minimal guardrails, the initial quote may be less meaningful than it looks.

- Unclear data and transition obligations. If the company exits, payroll records, claims files, and benefits history need to move cleanly.

What to negotiate instead

The goal isn't to eliminate every provider-friendly term. That won't happen. The goal is to remove unnecessary asymmetry.

A practical negotiation list includes:

- Clear liability allocation. Ask the provider to identify which employment-related risks it assumes, which it administers, and which remain fully with the client.

- Shorter termination windows. Push for a notice period the business can realistically live with if service quality deteriorates.

- Defined renewal mechanics. Ask how pricing changes are communicated, what can trigger changes, and whether any protections can be written into the agreement.

- Transition support language. Require operational cooperation if the company leaves, especially for payroll history, claims coordination, and benefits records.

The question that exposes weak contracts

Ask one direct question: if the relationship ends after a difficult claim or messy renewal, what exactly is the provider still obligated to do?

Weak providers answer this vaguely. Stronger providers answer it in operational detail.

“If a term matters during a dispute, it needs to appear in the contract before the dispute.”

This is the one place in the process where outside benchmarking can be useful. PEO Metrics is one example of a firm that reviews PEO pricing, contract terms, liability language, and renewal risk to help buyers compare providers on a side-by-side basis rather than relying only on provider explanations.

Conclusion Your PEO Insurance Evaluation Checklist

The clearest answer to what is PEO insurance is this: it's a co-employment insurance and administration structure that can change cost predictability, claims handling, and legal responsibility. It is not just a health plan shopping arrangement.

The companies that use it well don't chase the lowest visible fee. They verify how the master policy works, who owns which risks, what happens at renewal, and how hard it is to leave.

Use this checklist in every provider conversation:

- Confirm the master policy structure. Ask whether the PEO is the plan sponsor or administrator, and which carrier underwrites each coverage.

- Map retained liability. Identify what the PEO assumes versus what the client still owns operationally.

- Separate fees from insurance cost. Don't accept bundled pricing without understanding the components.

- Review audit exposure. Ask how payroll changes and classification issues affect final cost.

- Scrutinize renewal language. Find out how repricing works and what notice applies.

- Test claims handling. Ask who opens claims, who communicates with the carrier, and who stays involved after separation.

- Check exit terms. Make sure transition support is explicit.

- Match control needs to the model. If the company wants deep carrier and plan design control, a PEO may or may not fit.

If a company is comparing PEOs, renegotiating an existing agreement, or trying to understand whether a broker, ASO, or PEO structure makes more financial sense, PEO Metrics provides independent side-by-side analysis of pricing, benefits, contract terms, service model, compliance support, and key risk trade-offs.