Most advice about Employment Practices Liability Insurance treats it like a box to check in a PEO proposal. That's the wrong frame. A PEO can absolutely improve administrative support around HR and compliance, but the existence of EPLI on a proposal says almost nothing about how much risk moved off the employer's balance sheet.

What matters is the policy structure, the claimant definitions, the exclusions, the sublimits, the carrier, and the contract language that decides who controls the claim when something goes wrong. A CFO reviewing a PEO quote should treat EPLI the same way they'd treat debt covenants or indemnity language. Small wording differences can decide whether the insurer funds a serious claim or whether the employer pays lawyers out of pocket while arguing about coverage.

Table of Contents

- Why EPLI Is Not Just Another Line Item in Your PEO Quote

- What EPLI Actually Covers and Why It Matters

- Understanding Critical EPLI Exclusions and Gaps

- Deconstructing Your EPLI Policy Structure

- Evaluating EPLI Within a PEO Proposal A Practical Checklist

- Key Takeaways for Negotiating Better EPLI Terms

Why EPLI Is Not Just Another Line Item in Your PEO Quote

A PEO sales sheet often makes Employment Practices Liability Insurance look interchangeable. It isn't. According to IRMI's definition of employment practices liability insurance, EPLI is designed to cover employment-related claims such as wrongful termination, discrimination, sexual harassment, retaliation, defamation, invasion of privacy, failure to promote, and negligent evaluation. It's typically written on a claims-made basis and commonly purchased to pay defense costs, settlements, and damages arising from alleged workplace misconduct.

That sounds straightforward until a buyer asks the questions that matter. Is the policy dedicated to the client or shared through a master program? Who is the named insured? Does the employer get separate limits or share capacity with other client companies? Does the PEO control reporting, panel counsel, and settlement decisions?

The real financial mistake

The common mistake is comparing EPLI by premium or by a marketing summary that says “included.” A buyer can end up with a broad-looking benefit that narrows sharply once a claim touches shared employment responsibility, wage practices, contractor status, or a non-employee claimant.

A better starting point is to compare PEO master policy vs standalone policy structures before discussing price. A master policy may work well in some settings. In others, it creates uncertainty because the employer is relying on a policy negotiated and controlled by someone else.

Practical rule: If the PEO won't provide the specimen wording, endorsements, and clear claims-reporting obligations, the buyer doesn't yet know what it's purchasing.

What robust protection looks like

A strong EPLI position inside a PEO relationship usually has three features:

- Clear insured status: The client entity and relevant managers are expressly included, not implied.

- Defined claims handling: The contract says who reports a claim, when it must be reported, and who selects counsel.

- Visible limits and carve-outs: The buyer can see where the headline protection stops, especially for high-friction scenarios.

A useful test is simple. If an HR director asks, “An applicant alleges discrimination after a rejected offer and names both the company and the PEO. Who tenders the claim, who hires counsel, and which limit applies?” the agreement should answer that in plain language. If it doesn't, EPLI isn't a line item. It's an unresolved risk.

What EPLI Actually Covers and Why It Matters

The practical value of Employment Practices Liability Insurance EPLI is that it funds the legal response to employment claims that can arise from ordinary management decisions. Hiring, discipline, performance feedback, promotions, investigations, and terminations all create points of friction. When the employee or applicant says the action was unlawful, defense costs start before the employer has a chance to prove it acted reasonably.

CRC Group reports that nearly 20% of EPLI claims against companies with fewer than 500 employees result in defense and settlement costs above $125,000, and Coalition states that EPLI lawsuits have increased by 400% over the last two decades. That's why this coverage belongs in a CFO conversation, not just an HR conversation.

The claims buyers usually expect

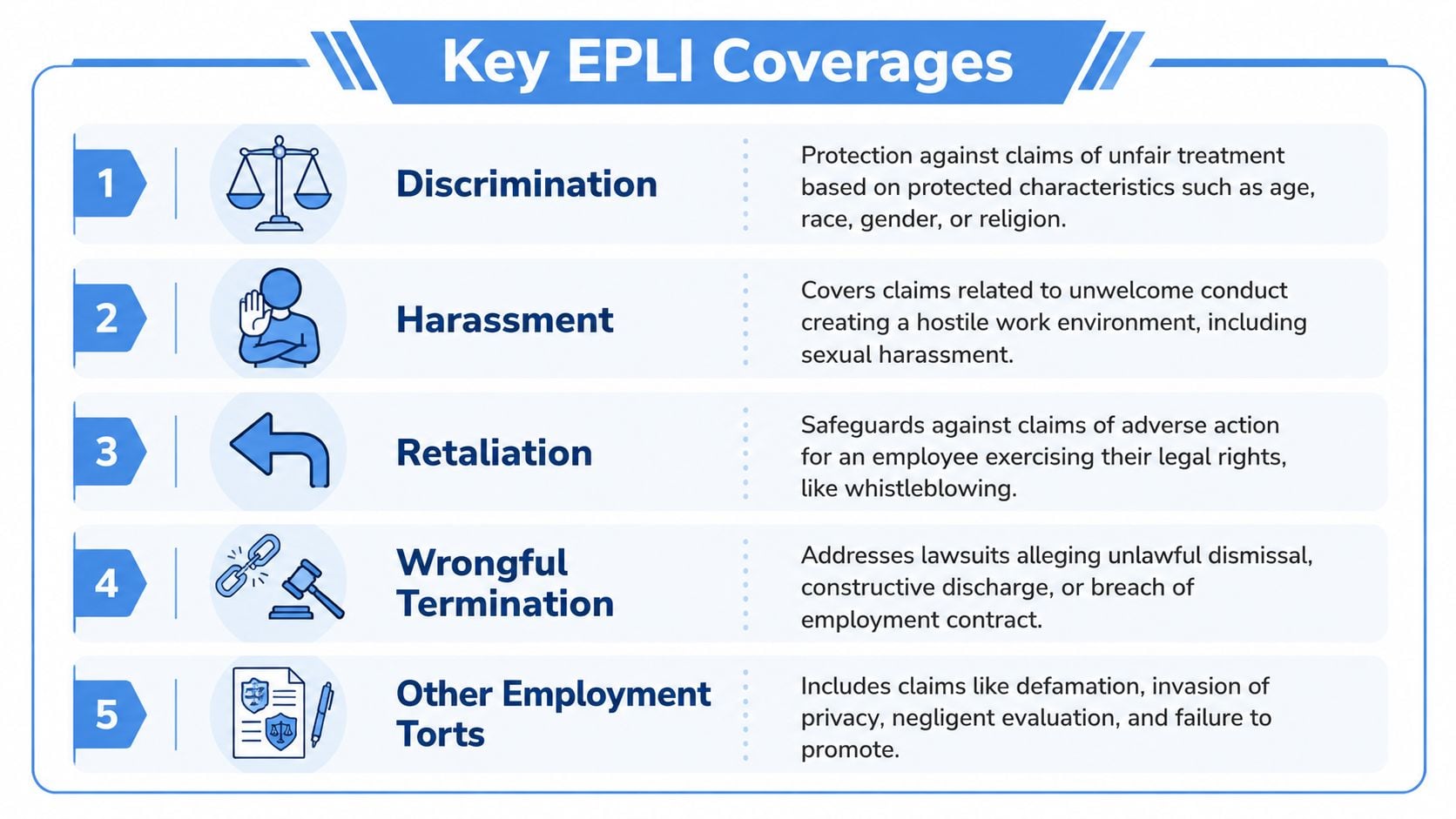

Most employers correctly think of EPLI as protection for the classic workplace claims.

- Wrongful termination: A terminated employee alleges the stated reason was pretext and that the actual motive was unlawful.

- Discrimination: A candidate says the hiring process treated them unfairly based on a protected characteristic.

- Harassment: A supervisor's comments, messages, or conduct allegedly created a hostile work environment.

- Retaliation: An employee complains internally, participates in an investigation, or raises a legal concern, then says the company punished them for it.

- Other employment torts: Defamation, invasion of privacy, negligent evaluation, and failure to promote can also fall into the EPLI bucket.

What that looks like in the real world

A manager writes a performance review that says an employee “isn't energetic enough for this team.” The employee is later denied a promotion and claims age bias. Another employee reports harassment, then receives a final warning for conduct issues two weeks later and alleges retaliation. A recruiter rejects an applicant, but interview notes include comments about “culture fit” that read badly in discovery.

None of these scenarios requires the employer to be wrong for legal spend to begin. That's the point. EPLI often matters most when the company believes it behaved appropriately but still has to defend that position.

The expensive part isn't only the final outcome. It's the process of responding, preserving documents, dealing with agency inquiries, and retaining counsel.

Why this matters in a PEO setting

In a PEO relationship, the line between client action and PEO-supported process can blur. A handbook may come from the PEO, termination guidance may involve the PEO HR team, and payroll or onboarding records may sit in the PEO platform. Buyers should understand how PEO employment practices liability is structured before assuming a claim will move cleanly through insurance.

That's especially true for sensitive decisions involving pregnancy, accommodations, and leave. For HR teams reviewing process fairness and candidate communication, practical resources such as career guidance when pregnant can help leaders think more carefully about how workplace decisions are perceived long before a claim exists.

Understanding Critical EPLI Exclusions and Gaps

The most dangerous EPLI misunderstanding is believing the covered-claims list tells the whole story. It doesn't. The coverage grant matters, but the exclusions, definitions, and endorsements usually decide whether the policy responds the way the buyer expects.

One common fault line is who can bring the claim. According to Vouch's discussion of EPLI claimant definitions and contractor issues, coverage can change materially when the claimant is a customer, vendor, visitor, or contractor. The policy language around who qualifies as a claimant and whether independent contractors are included can create defense-cost gaps or outright claim denials.

Claimant definitions change outcomes

A buyer should never assume that “employment-related claim” automatically means any person alleging misconduct by staff is covered.

Consider a few scenarios:

- Customer harassment allegation: A restaurant manager allegedly harasses a customer during repeated visits. If third-party coverage isn't built in, the EPLI program may not respond.

- Vendor complaint: A long-term on-site vendor says a company supervisor made discriminatory comments. The dispute feels employment-adjacent, but coverage may turn on whether the vendor counts as a covered claimant.

- Independent contractor dispute: A contractor alleges retaliation after raising concerns about treatment. If the policy excludes contractors from the claimant definition, counsel may spend early weeks arguing coverage instead of defending the merits.

Wage and hour is the gap buyers miss

The second fault line is wage and hour exposure. Many articles mention it loosely, but buyers need to know whether the policy covers those allegations, partially covers them, or excludes them outright. That issue is covered in detail in the next section because it's often the most technical and financially misunderstood part of the program.

If a company has an hourly workforce, multiple states, variable scheduling, or contractor usage, the first question shouldn't be “What is the limit?” It should be “Which legal theories are carved out?”

What to ask when reviewing the proposal

A buyer should ask for the exact wording, not just a proposal summary. The practical review should include:

- Claimant scope: Are former employees, applicants, temporary workers, and contractors included?

- Third-party coverage: Does the policy address customers, visitors, and vendors, or is that endorsement missing?

- Defense language: Are defense costs inside the limit, and can the employer get stuck funding counsel while coverage is disputed?

- PEO coordination: If the allegation touches a PEO-managed process, who tenders the claim?

For employers that want a broader review of where legal liability can fall between insurance policies and service contracts, this guide to PEO insurance coverage for legal claims is a useful companion.

Deconstructing Your EPLI Policy Structure

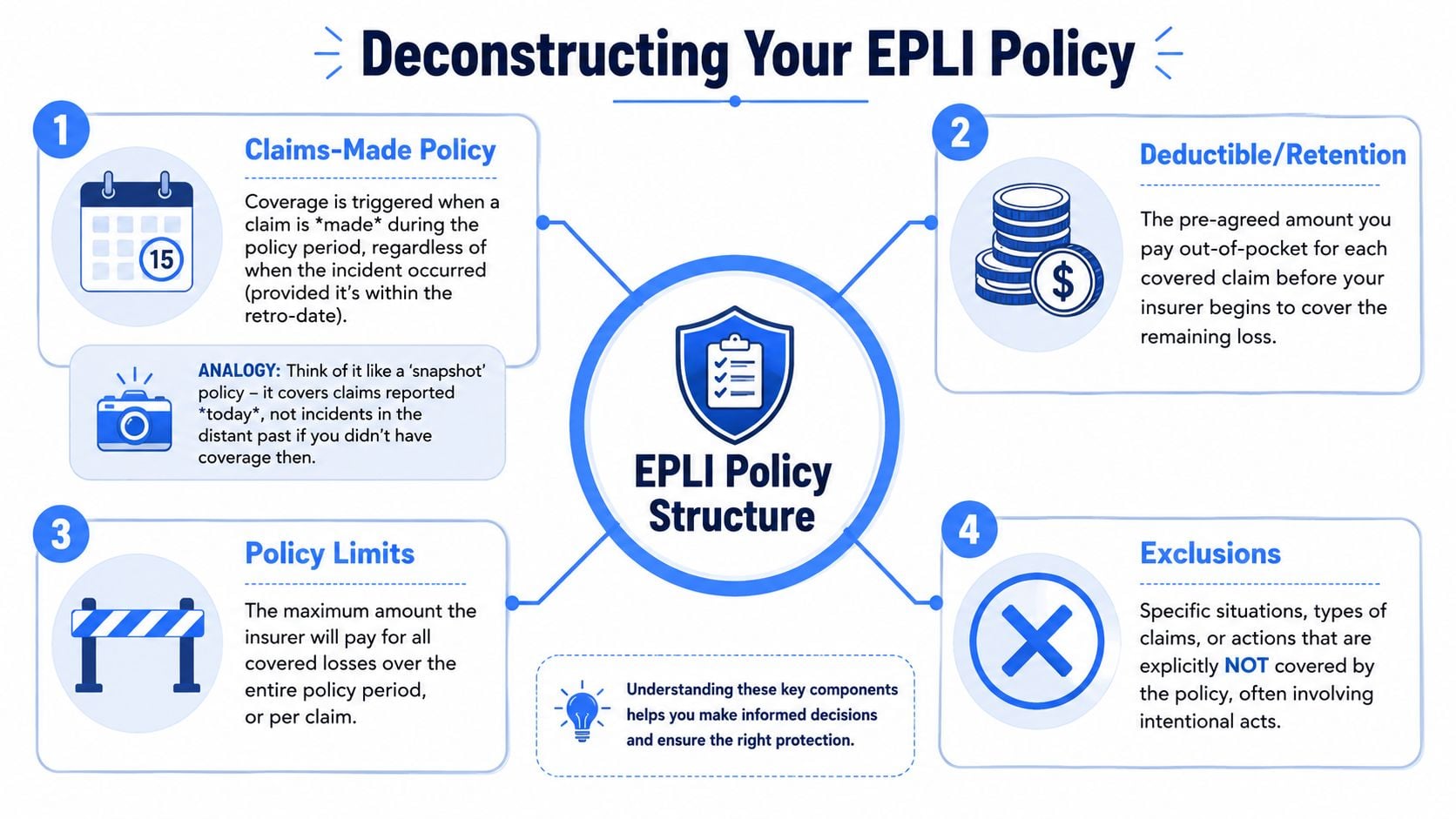

The mechanics of Employment Practices Liability Insurance EPLI matter as much as the coverage categories. Two policies can both say “EPLI included” and still behave very differently after a claim arrives.

Most EPLI is written on a claims-made basis. That means coverage is generally triggered when the claim is made during the policy period, subject to the policy's terms and timing requirements. For employers moving into or out of a PEO, that timing issue becomes critical because an employment event can occur under one arrangement and surface as a claim under another.

Why claims-made needs extra attention

A simple analogy helps. A claims-made policy is less like a permanent historical archive and more like a current reporting window. If the claim comes through the window correctly, the policy may respond. If the claim arrives after a switch in coverage, or gets reported late, the employer can end up in a dispute over which insurer, if any, has responsibility.

That's why a CFO reviewing a PEO transition should ask about retroactive dates, notice requirements, and post-termination reporting options. If a manager terminates an employee near the end of the PEO relationship and the demand letter arrives later, the gap often appears there.

Four terms that decide real-world outcomes

A useful policy review focuses on these mechanics:

- Limits: The maximum available amount. Buyers should confirm whether limits are shared under a master program or dedicated to their entity.

- Retention or deductible: The amount paid before insurance responds. The contract should say whether the client, the PEO, or both are responsible.

- Defense arrangement: Some policies give the insurer broad control over counsel. Others allow more participation by the insured.

- Reporting requirements: Late notice can damage an otherwise valid claim.

A surprisingly common negotiation failure is accepting summary language such as “coverage provided through carrier partner” without asking for the actual policy form and endorsements.

A proposal summary is marketing. The specimen policy is the operating document.

Wage and hour sublimits are where buyers get burned

The most misunderstood technical issue is wage and hour exposure. Industry guidance summarized by ABHE's EPLI overview notes that many policies either exclude these claims or provide only defense-only coverage with a sublimit, often in the range of $100k, $250k, or $500k. That amount can sit far below the main policy limit and may not cover settlements or judgments.

This creates a mismatch between expectation and reality. A PEO proposal might advertise a strong headline limit for discrimination or harassment claims, while the company's most likely pain point is a pay-practice dispute that only gets a small defense bucket.

A few examples make that tangible:

- Misclassification allegation: A group of workers says they should have been treated as employees rather than contractors. The policy may offer limited defense support, but not a meaningful path to settlement funding.

- Off-the-clock claim: Supervisors allegedly expected pre-shift work without proper pay. Counsel fees may erode the sublimit quickly.

- Meal-break and scheduling dispute: For a multi-state employer, a single practice can create repeated allegations across locations.

What works and what doesn't

What works is matching the policy to the workforce. Employers with concentrated executive headcount and low hourly exposure may find standard EPLI adequate. Employers with broad hourly populations, contractor use, or decentralized scheduling need much tighter diligence.

What doesn't work is focusing only on the top-line limit and assuming every employment dispute uses the same insurance bucket. In practice, the legal theory drives the coverage result.

Evaluating EPLI Within a PEO Proposal A Practical Checklist

A PEO buyer should review EPLI the way legal counsel reviews indemnity language. The question isn't whether coverage exists. The question is whether the contract and policy respond to the claim patterns the employer is likely to face.

Cornell's discussion of EPLI and moral hazard is especially relevant in PEO settings because claims tied to pay practices, scheduling, or contractor misclassification can blur responsibility across the employer, PEO, and insurer layers. That's exactly where buyers need a disciplined diligence checklist.

The questions that should be asked before signing

Start with the operating structure, not the premium.

Is the EPLI issued as a standalone client policy or through the PEO's master program?

Shared programs can be efficient, but the buyer needs to know whether limits, endorsements, and claims handling are customized or pooled.Who is the named insured and who qualifies as an insured person?

The employer entity, directors, officers, managers, and HR personnel should be addressed expressly.Who reports claims and on what timeline?

If the contract says the client must notify the PEO “promptly,” that's not enough. The process should identify the contact, the format, and what counts as a reportable event.Who controls defense counsel and settlement authority?

If the PEO or carrier can settle without meaningful client input, finance and HR need to know that before a dispute hits.What happens when the client leaves the PEO?

Tail issues, transition reporting, and continuity of coverage should be reviewed before implementation, not during divorce.

Contract wording worth circling in red

Certain phrases deserve immediate follow-up:

- “As available under the master policy” often means the summary is not the full promise.

- “At PEO discretion” can signal claims-control asymmetry.

- “Client responsible for acts outside PEO-guided practices” sounds reasonable until the parties disagree about what the PEO guided.

- “Coverage subject to carrier approval” may leave too much unresolved at signing.

A buyer that wants a broader diligence framework can use a PEO master service agreement checklist alongside the insurance review so the policy and service contract are read together.

Standalone EPLI vs PEO Master Policy EPLI

| Attribute | Standalone EPLI Policy | Typical PEO Master Policy |

|---|---|---|

| Policyholder control | Employer usually has more direct visibility into policy wording and endorsements | PEO often negotiates and administers the program |

| Limits | May be dedicated to the employer | May be shared or structured through a broader client program |

| Claims reporting | Usually direct from employer to broker or carrier | Often routed through the PEO or coordinated with it |

| Counsel selection | Can be more transparent depending on the policy | Panel counsel and process may be controlled centrally |

| Coverage tailoring | Easier to align with specific workforce risks | May be standardized across many client profiles |

| Transition risk | Employer can manage continuity more directly | Offboarding can create questions about tail and prior acts |

| Wage and hour fit | Can sometimes be negotiated around the employer's exposure | May follow a standard endorsement structure |

| Administrative convenience | More work for the employer | Often easier operationally, but less bespoke |

A practical review workflow

A clean diligence process usually looks like this:

- Ask for documents, not summaries: specimen policy, endorsements, certificate, and claim-reporting instructions.

- Map claims to operations: compare the wording against actual hiring, discipline, payroll, scheduling, and contractor practices.

- Review the service contract with the policy: insurance language that looks fine in isolation can break down when the MSA shifts responsibility back to the client.

- Benchmark alternatives: broker quotes, standalone EPLI options, and independent advisors such as PEO Metrics can help compare whether the PEO's bundled coverage is efficient or opaque.

The goal isn't to reject every PEO master policy. Many work well. The goal is to know what has been transferred and what still sits with the employer.

Key Takeaways for Negotiating Better EPLI Terms

Most buyers have more influence than they think. The mistake is negotiating only the administrative fee, payroll spread, or medical renewal assumptions while letting EPLI stay in brochure language.

What to request

Ask for the documents that govern reality:

- Specimen policy

- All endorsements

- Certificate of insurance

- Claim-reporting instructions

- The contract section that allocates responsibility between the client and the PEO

If a PEO resists providing those materials, that's useful information. It means the buyer is being asked to trust a summary where precision matters.

What to say in negotiation

Direct language works better than broad objections.

“The company needs confirmation of claimant definitions, third-party coverage, wage-and-hour treatment, and post-termination reporting before final approval.”

That sentence tells the PEO the buyer understands the actual risk points. It also changes the conversation from “Do you include EPLI?” to “Show exactly how the program responds.”

Where the leverage usually sits

Negotiation advantage often stems from specificity:

- Narrow vague discretion clauses

- Clarify who pays the retention

- Define claims notice obligations

- Request transition language for departure from the PEO

- Tie service responsibilities to coverage assumptions

For contract support on the liability side, this guide to PEO indemnification negotiation tips is a practical companion to the insurance review.

The final takeaway is simple. Employment Practices Liability Insurance EPLI inside a PEO relationship shouldn't be accepted as a bundled feature. It should be underwritten, negotiated, and documented with the same care as any other meaningful risk transfer.

PEO buyers that want an independent review of EPLI structure, contract terms, pricing trade-offs, and side-by-side PEO comparisons can use PEO Metrics as part of the diligence process. The firm analyzes proposals, flags contract and coverage issues, and helps employers understand where bundled protection is clear, where it's limited, and which negotiation points are worth pushing before signature.