A CFO opens the renewal packet expecting the usual movement in payroll taxes, admin fees, and benefits rates. Instead, one line drives the conversation. Workers' compensation is up sharply, or the medical renewal no longer behaves like the prior year. Somewhere in the notes sits the phrase experience rating adjustment.

That phrase matters more than most buyers realize.

In a PEO relationship, the rating model isn't just an insurance technicality. It determines who absorbs bad claims years, who benefits from strong loss control, how much budget volatility the company carries, and how much bargaining power exists at renewal. A company can sign with the right service team and still end up in the wrong pricing structure.

For HR directors, finance leaders, and owners reviewing PEO options, the useful question isn't just “experience rating vs community rating, what's the definition?” The better question is, which model is helping or hurting the business inside this contract right now?

Table of Contents

- The Rating Model Hiding in Your PEO Renewal

- What Are Experience Rating and Community Rating

- How Each Rating Model Is Calculated

- The Real Cost Impact on Your PEO Partnership

- Comparing Rating Models Side by Side

- Negotiation Tactics and Contract Clauses

- Your PEO Rating Model Decision Checklist

The Rating Model Hiding in Your PEO Renewal

A common renewal problem looks like this. The PEO admin fee barely moves, payroll assumptions look normal, and service language is unchanged. Yet the total cost rises enough to force a board-level question. The answer often sits inside the insurance rating method rather than the visible service fees.

That's why experienced buyers read the workers' compensation and benefits sections before they debate the relationship manager or the HR platform. The insurance engine usually moves the larger dollars.

Where the surprise usually starts

In practice, many employers don't learn the difference between experience rating and community rating until after a renewal lands. A company with a rough claims year may discover that its own loss activity is feeding directly into price. Another company with a clean record may realize it's being blended into a broader pool and subsidizing weaker performers.

Neither model is automatically wrong. The mistake is entering a PEO contract without knowing which one is driving the bill.

Practical rule: If a renewal increase isn't explained line by line, assume the rating methodology is doing more work than the sales presentation ever mentioned.

Why CFOs should care early

This issue affects three things immediately:

- Budget accuracy. A community-rated approach can smooth year-to-year swings, while an experience-driven model can make renewals more sensitive to the employer's own claims record.

- Risk allocation. One structure spreads pain across a pool. The other keeps more accountability with the individual employer.

- Negotiation position. A buyer who understands the model can ask better questions about pooling, surcharges, renewals, and claims handling before signing.

A lot of renewal disputes aren't really about “price.” They're about a mismatch between the company's risk profile and the PEO's pricing architecture. That's why contract review matters as much as carrier comparison. A strong starting point is a review of PEO renewal clause negotiation strategy, because the critical negotiating advantage is often found in renewal language, adjustment rights, and claims-related provisions rather than the headline fee.

The business takeaway

A company with disciplined hiring, training, and claims management usually wants credit for that discipline. A company with volatile claims, rapid operational change, or a rough recent history may prefer insulation from it.

That's the fundamental frame for experience rating vs community rating. It's not academic. It's a choice about whether the contract prices the company as its own risk or as part of someone else's pool.

What Are Experience Rating and Community Rating

The cleanest way to understand these models is to ignore insurance jargon for a minute and focus on who pays for whose risk.

Early in the process, this simple comparison helps.

| Criterion | Experience Rating | Community Rating |

|---|---|---|

| Core pricing logic | Prices reflect the employer's own loss or claims experience | Prices reflect the broader pool's combined experience |

| Main financial effect | Strong performers can benefit. Poor performers can pay more | Costs are spread across the pool, which can soften individual swings |

| Best fit | Employers that want price accountability tied to their own record | Employers that want insulation from their own recent claims history |

| Main downside | More exposure to adverse renewal movement if claims worsen | Less reward for a clean record and stronger controls |

| Negotiation focus | Data accuracy, claims handling, mod treatment, loss runs | Pool quality, pooling rules, renewal methodology, transfer terms |

A visual summary helps clarify the split.

Community rating means the pool matters more than the employer

In U.S. small-group health insurance, community rating became a major policy milestone in the early 1990s. New York law defines it as a method where the premium for all people covered by a policy form is the same based on the experience of the entire risk pool, without regard to age, sex, health status, or occupation, and the state applies it to groups with 50 or fewer eligible members for rate-determination purposes, according to Connecticut General Assembly analysis of New York small-group law.

Put plainly, community rating says the employer is buying into a shared pool. The company's own history matters less than the overall book of business or the legally defined rating structure.

That can be attractive when the employer wants protection from being singled out after a bad year. It can be frustrating when the employer has controlled costs well and sees little direct reward.

For buyers trying to connect theory to PEO bills, this explanation of PEO workers' comp experience rating is useful because many PEO proposals blur the line between true pooling and employer-specific pricing.

Experience rating means the employer's own record carries weight

Experience rating works more like commercial auto or a company-specific safety scorecard. The insurer looks at the employer's own payroll and loss history and uses that record to estimate future cost.

That creates a straightforward business trade-off:

- Cleaner claims history can improve pricing position.

- Poor claims experience can push renewals up.

- Operational discipline matters because claims, return-to-work, and safety activity have financial consequences.

Community rating spreads risk broadly. Experience rating makes the employer live closer to its own record.

Why the distinction matters inside a PEO

Many employers assume joining a PEO automatically means broad pooling and stable pricing. Sometimes that's true. Sometimes it isn't. Some PEO structures preserve more individual accountability than buyers expect, especially in workers' compensation.

That's why experience rating vs community rating should be treated as a contract question, not just a textbook definition. The company needs to know whether the PEO is really offering shelter from volatility, or repackaging an experience-sensitive program under a bundled service model.

How Each Rating Model Is Calculated

Definitions are useful. Calculations decide the invoice.

Experience-rated pricing is more data-heavy and usually more defensible if the underlying data is clean. Community-rated pricing is simpler from the employer's perspective, but that simplicity can hide important assumptions about the pool.

How experience rating is built

The National Council on Compensation Insurance explains that the formula typically uses the latest available three years of an employer's payroll and loss data, and that the experience period can range from less than 12 months to 45 months depending on effective date and state rules. NCCI also notes a core principle: the larger the premium size, the more reliable the actual record is in predicting future losses, which means larger employers generally have more credible loss experience, according to NCCI's explanation of experience rating.

The practical meaning is straightforward. A larger employer usually has enough payroll and claims volume for its record to carry more statistical weight. A smaller employer can see sharper movement because one or two claims can distort the picture.

For a CFO, that means volatility isn't just about the claims themselves. It's also about how much credibility the formula gives the employer's history.

What the inputs usually tell a buyer

When a PEO or broker says a program is experience-sensitive, the employer should expect pricing to reflect some combination of these company-specific inputs:

- Payroll history tied to class codes and exposure.

- Loss history including claim frequency and severity.

- Timing of losses within the applicable historical window.

- Employer size because credibility rises with premium size.

That's why finance teams should ask for a documented explanation of the premium mechanics, not just a rate sheet. A useful companion is this breakdown of PEO workers' comp premium calculation methods, especially when a proposal mixes manual rates, mods, pooled factors, and internal adjustments.

A familiar analogy exists outside commercial insurance. In personal auto coverage, an insurer often uses a driver's own record rather than treating every driver in a city the same. Buyers who want a simple version of that idea can look at insurance advice for traffic violations, because it shows how prior behavior can influence future pricing in a more familiar line of insurance.

How community rating is built

Community rating starts from a different premise. The employer is priced from the broader risk pool rather than from its own detailed historical record. In practical terms, the PEO or carrier is saying, “This group enters a shared pricing structure.”

For the buyer, that usually means:

- the employer's own claims history has less direct impact on pricing,

- renewal movement is influenced more by the pool's performance and applicable rating rules,

- and individual employers have less ability to argue, “our own record is better than this bill suggests.”

Financial reality: Community-rated pricing often feels easier to budget until the employer realizes it has limited ability to separate itself from the pool.

What this means during underwriting

When an employer asks how each model is calculated, the key question is who controls the story told by the data.

Under experience rating, the company's own history speaks loudly. Under community rating, the pool speaks for everyone. That difference affects pricing, but it also affects what can be negotiated, corrected, challenged, or defended.

The Real Cost Impact on Your PEO Partnership

Inside a PEO relationship, rating models stop being abstract fast. The company isn't just buying HR support or payroll administration. It's stepping into a structure where workers' compensation and benefits costs may be pooled, partially pooled, or tied back to the employer's own record.

That's why two companies can use PEOs with similar service menus and end up with very different financial outcomes.

When community style pricing helps

A company with a rough recent claims pattern may benefit from broader pooling. In that setup, its own adverse history may matter less than it would in a standalone, employer-specific pricing framework.

That can be valuable when the employer is rebuilding safety processes, recovering from operational disruption, or trying to stabilize cost after an ugly claims cycle. The PEO effectively gives the employer more insulation than a fully experience-sensitive structure would.

The trade-off is obvious. If that same employer improves quickly, the savings may not show up as directly or as fast because the pool still influences the result.

When experience sensitivity helps

A cleaner-risk employer often feels the opposite pressure. If the workforce is relatively low hazard, supervisors close incidents quickly, claims are managed tightly, and return-to-work is disciplined, that employer may want a structure that recognizes its own performance.

In that case, broad pooling can become expensive. The company may be carrying weaker participants in the PEO's book and receiving little pricing credit for better behavior.

Consequently, a review of how a PEO can affect an experience modification factor becomes important. The company needs clarity on whether its claims identity and future rating profile are being improved, diluted, or merely obscured.

The hidden issue is not just price

Most buyers focus on headline cost. Strong operators focus on cost behavior.

A PEO partnership needs to answer questions like these:

- Will one bad claim year hit this employer directly, or be spread across a pool?

- If safety performance improves, will the employer capture that value?

- Does the PEO have internal pooling rules that mimic community rating without calling it that?

- If the company exits, what claims history follows it and in what form?

The wrong model can make a good PEO look overpriced, or make a risky PEO look cheap until renewal arrives.

What works and what doesn't

What works is alignment.

A volatile employer that needs shelter usually does better with more pooled protection. A disciplined employer that wants economic credit for that discipline usually does better when pricing reflects its own record.

What doesn't work is accepting a generic “master policy advantage” statement without asking how the master policy allocates cost. Some PEOs pool aggressively. Some segment clients by risk band. Some use internal methodologies that sit somewhere between pure experience rating and true community rating.

For the CFO, the decision isn't whether pooling is good or bad. The decision is whether the PEO's structure matches the company's actual risk posture and appetite for volatility.

Comparing Rating Models Side by Side

The easiest way to evaluate experience rating vs community rating is to stop asking which one is “better” in general. The better question is which one fits the company's economics, claims profile, and tolerance for renewal surprise.

Here's the side-by-side view that matters in a PEO decision.

| Criterion | Experience Rating | Community Rating |

|---|---|---|

| Cost predictability | Can move more with the employer's own claims history | Usually smoother because costs are spread across a broader pool |

| Reward for safety | Stronger direct incentive because results can affect pricing | Weaker direct reward because individual results are blended |

| Exposure to bad years | Higher if the employer's own record deteriorates | Lower if the pool cushions the employer |

| Fairness test | “Pay closer to your own way” | “Share risk across the group” |

| Negotiation leverage | Stronger for employers with good history and good controls | Stronger for employers seeking insulation or transitional stability |

| Administrative simplicity | Often requires deeper data review and explanation | Often easier to present, harder to dissect |

Cost control versus cost protection

The core trade-off is simple.

Community rating offers protection from volatility, while experience rating offers more control over whether performance changes show up in cost.

A mature employer with stable operations, formal safety protocols, and confidence in its claims handling may prefer the accountability of experience-sensitive pricing. That employer wants a line of sight between operating discipline and insurance spend.

A company going through rapid hiring, acquisitions, new locations, or front-line turnover may prefer pooled stability while operations settle. In that environment, insulation can be worth more than perfect pricing precision.

Fairness depends on where the company sits

Both models can be called fair. They just define fairness differently.

Experience rating says it's fair for the employer's own record to matter. Community rating says it's fair to spread risk across a larger pool so one employer's bad stretch doesn't crush renewal pricing.

That's why buyers should test “fairness” against facts on the ground:

- A low-incident professional services firm may see community-style pooling as hidden subsidy.

- A higher-risk operator with recent losses may see the same pooling as needed protection.

- A growing multi-state employer may value stability more in one year, then seek performance-based pricing later.

For companies comparing pooled and standalone structures, this overview of PEO master policy versus standalone policy options helps frame where the trade-offs usually land.

The practical decision rule

The right model is usually the one that supports the company's strategy, not the one that sounds best in a sales meeting.

If leadership wants predictable budgeting and can accept less direct reward for strong performance, community-style pricing may fit. If leadership wants stronger accountability and believes claims control is a competitive advantage, experience-sensitive pricing may fit better.

The mistake is mixing those goals. A company can't ask for full insulation from bad years and full credit for good years under the same structure.

Negotiation Tactics and Contract Clauses

Most employers lose their advantage on rating issues because they negotiate too late. By the time the renewal arrives, the PEO already knows whether the company understands the pricing mechanics.

A buyer that asks detailed rating questions during selection gets better answers and usually better paper.

Questions that change the conversation

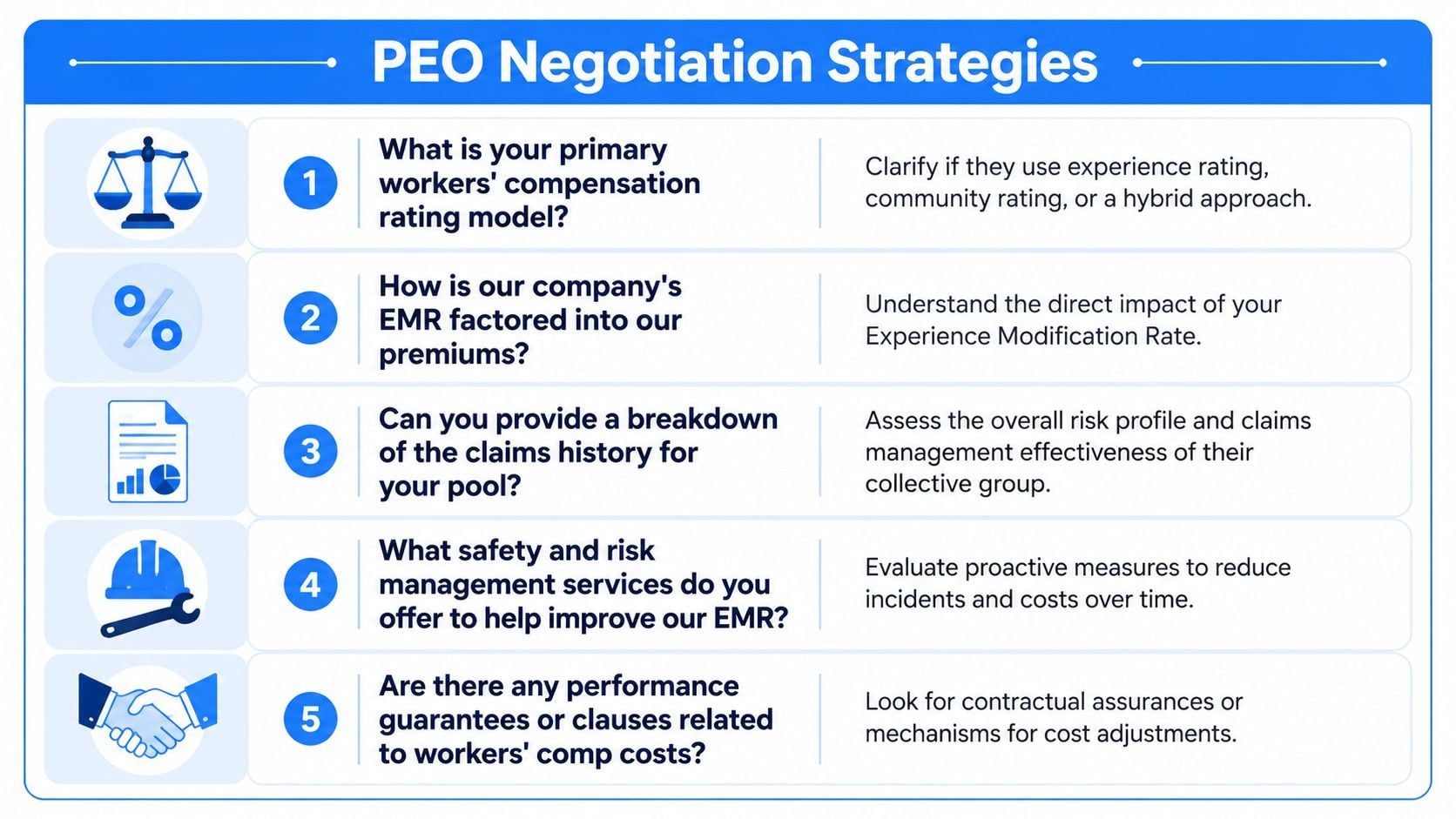

The fastest way to sharpen negotiations is to ask direct, uncomfortable questions early:

- What is the actual rating model in workers' compensation? Don't accept “master policy” as the answer.

- How is the employer's own claims history used? If the answer is vague, keep pushing.

- Is there internal pooling by industry, risk band, or client segment?

- What happens to claims history if the employer exits mid-term or at renewal?

- Who has discretion to surcharge, reclassify, or non-renew based on claims activity?

The negotiation visual below captures the core areas worth pressing on.

Contract language that deserves legal and finance review

Clauses worth special attention include:

- Renewal adjustment language that allows broad insurance repricing with limited explanation.

- Claims-based surcharge rights that let the PEO impose additional cost after adverse experience.

- Termination or non-renewal provisions tied to loss ratios, safety performance, or underwriting changes.

- Data access provisions covering loss runs, claim reporting, and post-termination history.

- Allocation language explaining whether the employer participates in broad pooling or a narrower internal pool.

One underappreciated negotiation issue is threshold movement in small-group markets. New York guidance shows that community-rating applicability can depend on eligible member count at application or renewal, and that some small-group contexts may still permit limited adjustments within a modified community-rating framework. The practical result is that the same company can face very different premium dynamics depending on market size, eligibility count, and state rules, as discussed in New York DFS guidance on rating rules and eligibility thresholds.

That matters when a company is near a size threshold, changing census composition, or adding states.

Where leverage actually comes from

Negotiation leverage increases when the buyer can explain exactly how the rating method shifts risk at renewal.

A PEO will often negotiate harder on fees than on opaque insurance methodology, because fees are visible and methodology is harder for buyers to benchmark. That's why astute employers ask for transparency before they ask for discounts.

The strongest asks usually sound like this:

- clearer renewal formulas,

- advance notice of claims-based adjustments,

- access to supporting loss data,

- defined treatment of the employer's history at exit,

- and tighter limits on discretionary surcharges.

A company that knows how the rating model works isn't just better informed. It's harder to price against loosely.

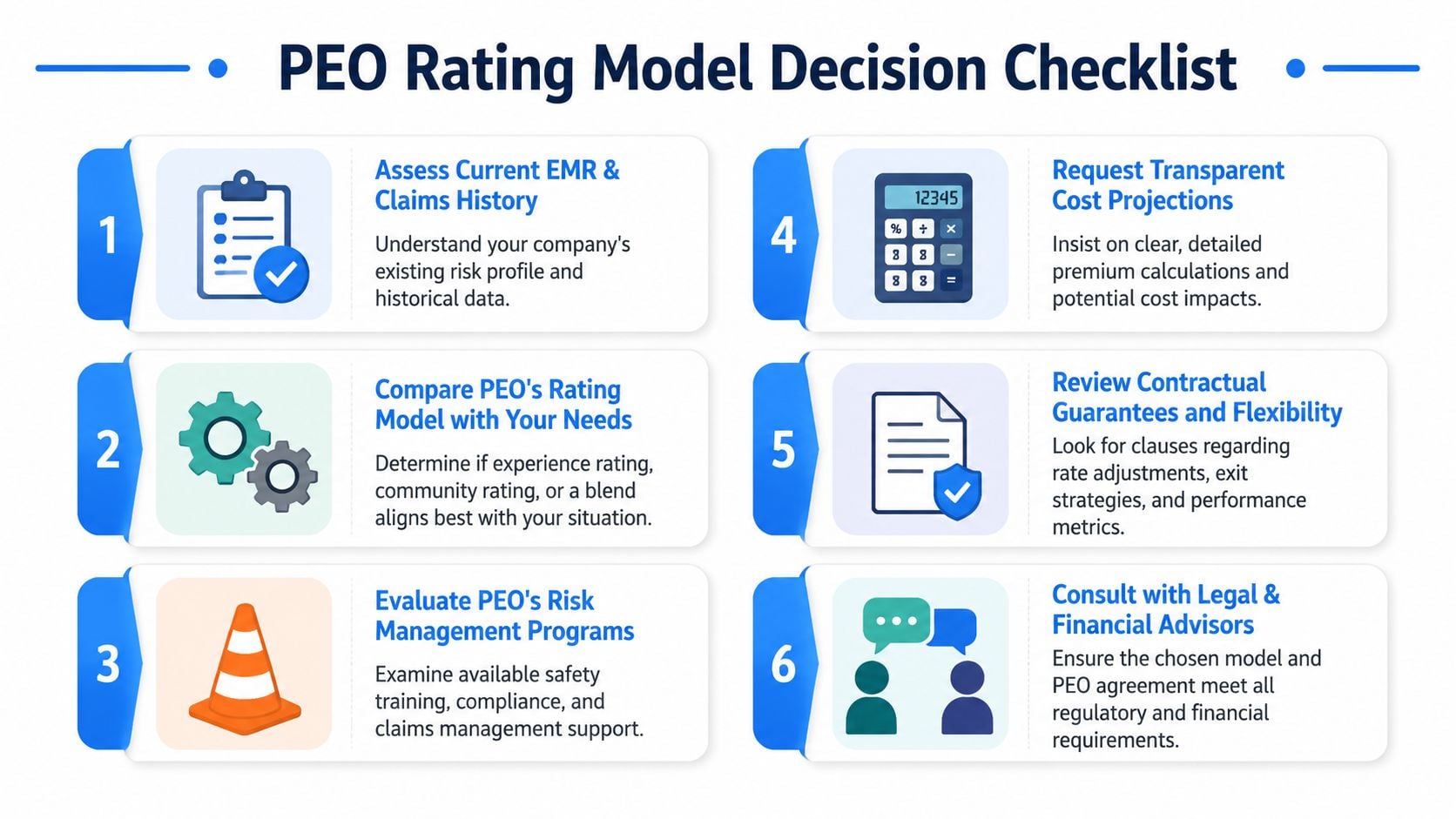

Your PEO Rating Model Decision Checklist

The final decision usually gets clearer when leadership stops evaluating the PEO in general and starts evaluating the fit between the company's own risk profile and the PEO's pricing structure.

This checklist keeps that discussion grounded.

Use this before reviewing the next proposal

- Pull the claims record first. Review recent workers' compensation and major benefits cost history before looking at any new PEO quote. The company needs to know whether its own record is an asset or a problem.

- Decide how much volatility the budget can handle. Some employers can absorb sharper renewals in exchange for better long-term alignment. Others need smoother year-to-year cost behavior.

- Test whether the company deserves individual credit. If safety, supervision, and claims management are robust, broad pooling may hide value that should show up in price.

- Check growth and headcount exposure. A company near rating or market thresholds should ask how census changes affect renewal treatment and negotiating power.

- Review the contract for claims discretion. If the PEO can reprice, surcharge, or terminate based on loss activity, leadership needs to understand that before signing.

- Match model to strategy. A company seeking protection from a rough period may want pooling. A company seeking financial reward for better risk control may want more experience sensitivity.

The clearest takeaway

The best choice usually isn't the cheapest quote. It's the rating structure that the company can live with after a bad year and still value after a good one.

That standard cuts through most sales language. If leadership can answer that question truthfully, the field narrows fast.

PEO buyers that want an independent review of pricing structure, contract terms, and renewal risk can work with PEO Metrics. The firm helps employers compare PEO options side by side, identify where experience rating or community rating is helping or hurting the deal, and negotiate stronger terms before renewal surprises show up in the budget.