A Chicago company usually starts shopping for a PEO at the exact moment internal HR stops being “manageable.” Payroll runs through one system, benefits sit with a broker, onboarding lives in spreadsheets, and someone on the leadership team is suddenly responsible for questions about leave, workers' comp, handbook updates, and hiring in another state. That's when the search for a professional employer organization in Chicago starts.

Most buyers then make the same mistake. They compare provider demos, skim the benefits deck, ask whether support is “dedicated,” and assume the decision is mostly about convenience. It isn't. A PEO is a co-employment arrangement. The client still runs the business and manages employees day to day, while the PEO takes on payroll, benefits administration, workers' compensation, and compliance support through that structure, as outlined in the PEO model overview.

Table of Contents

- Why Your Chicago PEO Decision Needs a Playbook

- How to Define Your PEO Requirements

- Decoding Chicago PEO Pricing and Benefits

- Choosing Between National and Local Chicago PEOs

- Navigating Illinois Compliance and PEO Contract Red Flags

- Using Data to Negotiate Your PEO Agreement

Why Your Chicago PEO Decision Needs a Playbook

A Chicago company with 35 employees can drift into a bad PEO deal faster than most owners expect. Payroll is still running. People are still getting hired. Then the first renewal hits, the admin fee is higher than expected, the medical rates did not improve enough to offset it, and the termination clause makes it expensive to leave. By then, the mistake is no longer theoretical. It is sitting in the P&L.

That is why this decision needs a playbook.

Chicago buyers are not choosing from a small local pool with predictable pricing. They are buying in a national market, and that creates wide variation in fees, service models, underwriting appetite, and contract terms. A polished proposal from a national firm can look safer than it is. A local or regional provider can look more expensive at first glance, then come out ahead once service access, workers' comp handling, and implementation support are priced accurately.

The cost difference can be material. A 50 employee company with a $4 million annual payroll might see one proposal priced as a per employee monthly fee and another priced as a percentage of payroll. On paper, both can sound reasonable. In practice, the spread can turn into tens of thousands of dollars a year once broker commissions, payroll processing charges, benefits administration fees, and year two increases are fully loaded. In Chicago, where employer health costs, wage pressure, and multistate hiring are common for growing firms, that spread matters.

A disciplined buyer should start with three assumptions:

- Pricing formats will obscure comparison unless you normalize them. Percentage of payroll, PEPM pricing, pass-through charges, and benefit-related fees need to be translated into one annual employer cost.

- Service language is often softer than the operating reality. "Dedicated support" can still mean a shared service team, slow escalations, or a rep who changes after implementation.

- Benefit savings claims can hide weaker economics elsewhere. Lower medical rates do not help much if the PEO adds higher admin fees, narrower plan choice, or contribution rules that do not fit your workforce.

Treat the decision as an operating model change. It affects cash flow timing, tax filing responsibility, employee experience, claim handling, and who owns problems when something goes wrong.

Co-employment raises the diligence standard. A business is not just handing off paperwork. In reality, it is entering a relationship that touches payroll execution, benefits eligibility, workers' compensation administration, employee records, and parts of compliance accountability. That is a different level of commitment than hiring another software tool or payroll processor.

Chicago adds its own pressure points. Employers here often need to weigh city and state leave requirements, a competitive hiring market, and the practical question of whether the PEO can support both Illinois employees and staff in other states without creating service gaps. The firms that buy well usually test the provider on those specifics early, before the sales process turns into a generic HR outsourcing conversation.

One useful starting point is a governance checklist that forces finance, HR, and leadership to agree on decision rights before provider meetings begin. This PEO workforce governance playbook helps structure that review so the buyer controls the process, not the sales deck.

A PEO can reduce workload and improve benefits access. It can also lock a company into a pricing and service model that is hard to unwind. Chicago employers should judge the offer on year one cost, year two risk, contract exit terms, and how the arrangement performs when there is a payroll error, a claim dispute, or a benefits problem that needs a same-day answer.

How to Define Your PEO Requirements

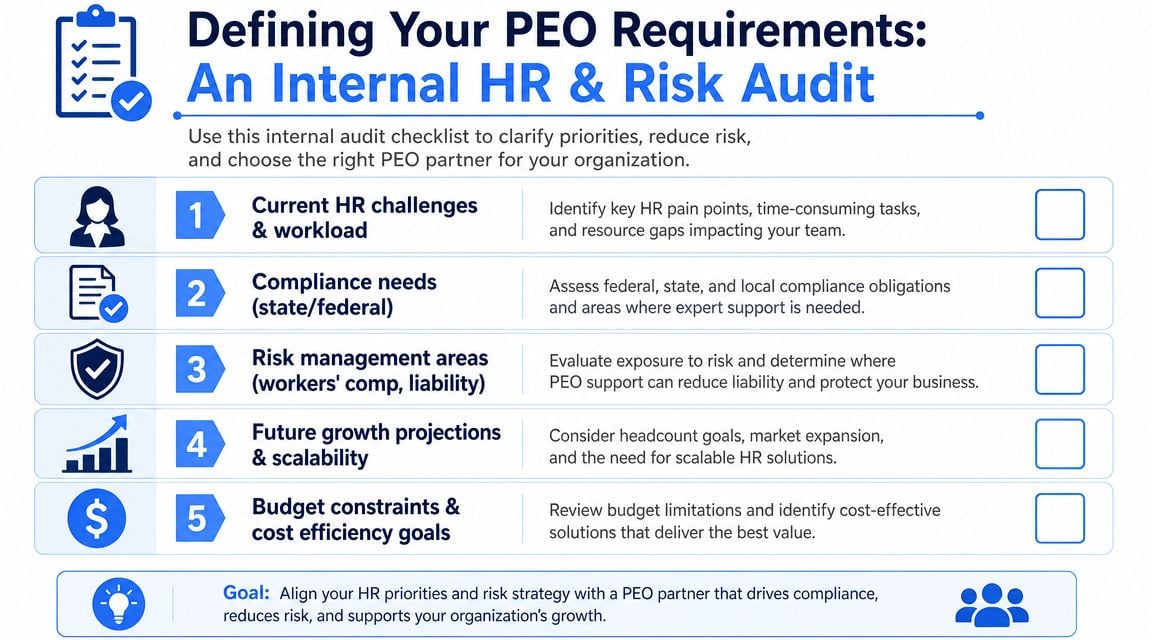

The fastest way to get bad PEO proposals is to give vague requirements. If a company tells providers it wants “better HR support,” “good benefits,” and “help with compliance,” every proposal will look polished and impossible to compare.

A strong buying process starts internally. Before asking any PEO for a quote, the business should decide what problem it is trying to solve.

Start with operational friction

The first screen is workload. Not sentiment. Not provider branding. Actual work.

Ask the internal team where time is being spent today:

- Payroll administration: Who reviews payroll, fixes errors, handles tax notices, and manages new-state setup?

- Benefits administration: Who answers enrollment questions, resolves carrier issues, and handles eligibility changes?

- Employee lifecycle work: Who owns onboarding, handbook acknowledgments, terminations, and document retention?

- Compliance handling: Who tracks state and local requirements, updates policies, and coordinates outside counsel when needed?

If the same two or three people are carrying all of it, the business already has a concentration risk problem. A PEO may help, but only if the RFP identifies the exact tasks expected to shift.

Build a buyer scorecard before issuing an RFP

A practical scorecard usually has four categories.

| Category | What to define internally | What to ask the PEO |

|---|---|---|

| HR administration | Current pain points and recurring manual work | Which tasks move to the PEO, which stay in-house |

| Compliance | States involved, leave complexity, policy maintenance needs | Who monitors changes and who is accountable for action items |

| Benefits | Plan competitiveness, employer contribution strategy, employee expectations | What plans are available and how pricing is structured |

| Strategic HR | Hiring support, training, performance process, manager guidance | Which advisory services are included versus extra-cost |

This exercise does more than organize requirements. It forces finance and HR to agree on what's worth paying for.

Industry research cited by NAPEO says businesses using a PEO grow twice as fast, have 12% lower employee turnover, and are 50% less likely to go out of business, which is useful context for ROI discussions, but those outcomes only matter if the provider solves the client's real operating issues, according to NAPEO industry research data.

A company that wants better benefits but doesn't need HR infrastructure should evaluate that differently from a company that needs payroll controls, compliance support, and manager guidance all at once.

A clean requirements document should separate must-haves from nice-to-haves. For example:

- Must-have items might include multi-state payroll support, benefits administration, workers' comp coordination, and named service contacts.

- Operational preferences might include a specific onboarding workflow, an integrated HRIS, or manager self-service features.

- Stretch asks might include recruiting support, training libraries, or more customized reporting.

That distinction matters during negotiation. If a provider bundles ten extras into the proposal but misses two must-haves, it's still a weak fit.

For buyers formalizing this process, a PEO master service agreement checklist is useful before proposals go out, not just before signature. It helps shape the questions that expose gaps early.

Decoding Chicago PEO Pricing and Benefits

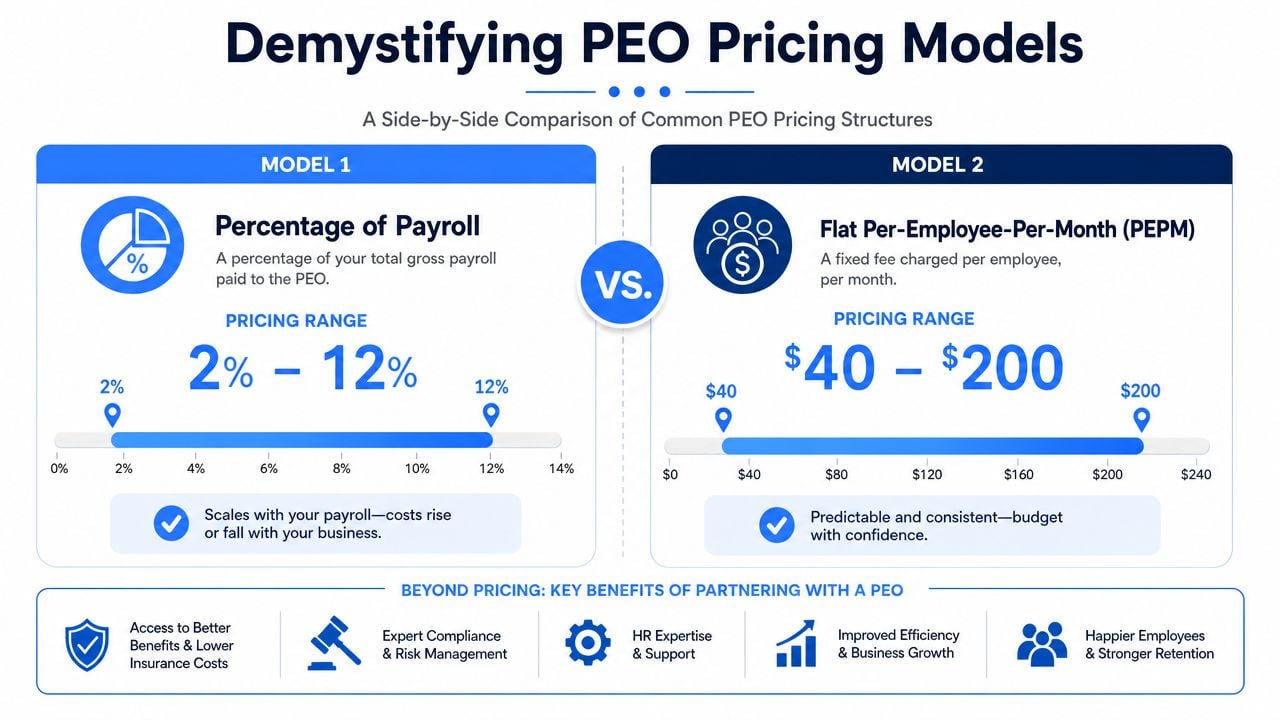

PEO pricing is confusing by design. A provider may quote a clean monthly fee and leave out implementation costs. Another may use a payroll percentage that looks modest until wage inflation pushes the fee up automatically. A third may talk about benefits savings while adding markup to the premium base.

That is why a Chicago buyer should convert every proposal into one number. Total all-in cost per employee.

The two pricing models that hide the real cost

Published benchmarking shows PEO pricing usually falls into one of two models: $40 to $200 per employee per month or 2% to 12% of payroll, with annual admin fees starting around $2,500 and benefit markups of 5% to 20%, based on this PEO pricing benchmark.

Those numbers matter because they drive very different outcomes depending on workforce profile.

A percentage-of-payroll model often gets expensive for employers with higher wages. A flat PEPM model can be easier to forecast, but only if the quote includes all recurring service fees. Neither approach is automatically better. The better one depends on wage base, headcount mix, benefit elections, and whether the fee schedules are transparent.

How to normalize every proposal

A buyer spreadsheet should isolate the following:

- Core service fees: Either PEPM or payroll-based fees

- Annual administrative charges: Compliance or account fees that may sit outside the headline quote

- Implementation costs: Setup, onboarding, data migration, and training

- Benefit-related charges: Any markup or embedded load on medical or ancillary lines

- Pass-through costs: Items the employer would pay with or without a PEO, tracked separately from service economics

Then calculate a normalized figure:

(total annual service fees + annual admin charges + implementation allocated over the contract term + benefit markups) ÷ average enrolled headcount

That number won't answer every question, but it stops a weak proposal from looking cheap.

The cleanest quote is rarely the cheapest contract. The cheapest contract is rarely the lowest total cost.

Benefits require the same discipline. Large-group access can help, but buyers still need to ask what plans are available, how renewal changes are handled, and whether ancillary products are optional or subtly bundled. A proposal that improves employee access but narrows plan flexibility may still be the right choice. It just needs to be priced transparently.

Finance teams that want a better frame for evaluating service layers alongside HR spend should also understand small business accounting prices. It's a useful reminder that back-office outsourcing decisions should be compared on operating impact, not sales language.

For benefits specifically, employers comparing rich PEO benefit menus against broker-led alternatives need side-by-side enrollment and employer cost modeling. A resource like employee benefits benchmarking can help structure that comparison before renewal pressure takes over.

Choosing Between National and Local Chicago PEOs

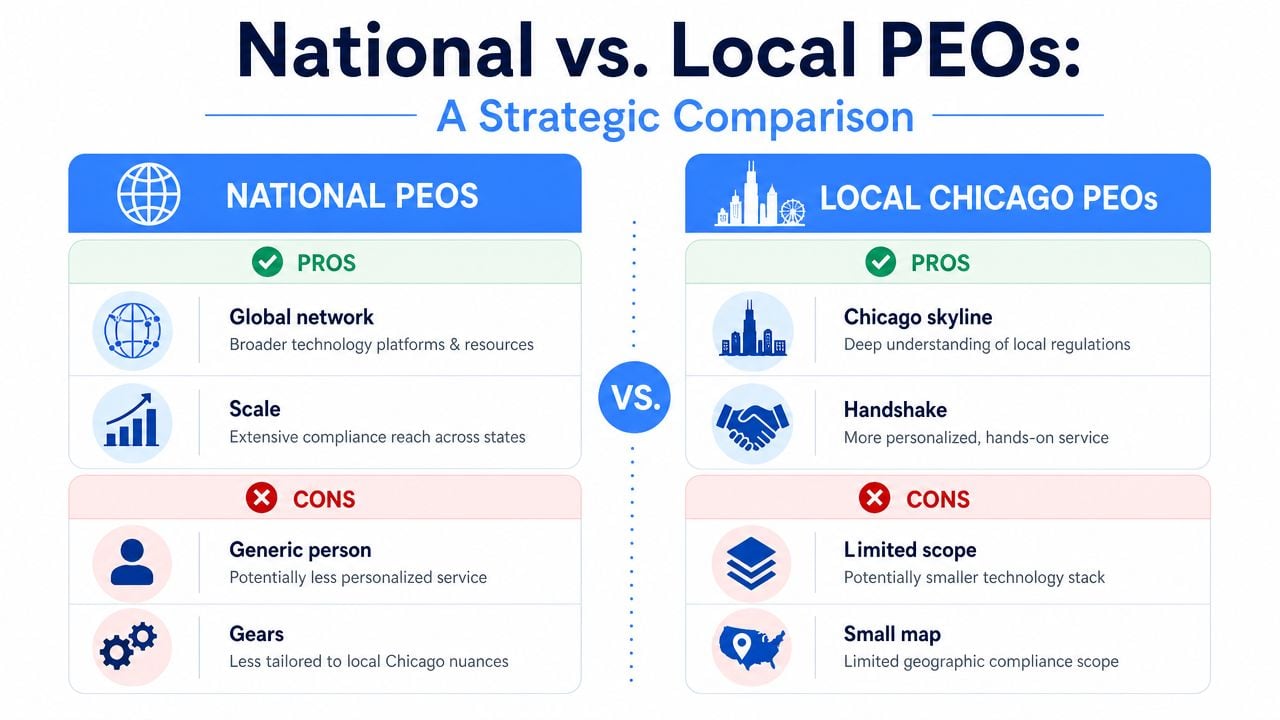

The national-versus-local choice gets oversimplified. Buyers are often told that national firms have better technology and local firms give better service. Sometimes that's true. Sometimes it isn't. The key issue is fit.

A company with employees only in Illinois may prioritize responsiveness and flexibility. A company with remote hires spreading across several states may care more about process discipline, broader compliance coverage, and system standardization.

When a national platform makes sense

National PEOs tend to work well when the employer needs consistency more than customization.

That usually applies when:

- The workforce is multi-state. Policy administration, leave handling, payroll setup, and tax coordination need repeatable process.

- Leadership wants one system. HR, payroll, onboarding, and benefits administration are easier to manage when they sit in a single operating environment.

- Reporting matters to finance. Larger providers often have more mature controls, data exports, and standardized workflows.

The trade-off is service intimacy. A large platform may route requests through teams instead of one relationship manager. Escalation can become process-driven rather than personal. Some buyers like that. Others hate it.

When a local Chicago PEO has the edge

A local or regional provider can be the better fit when leadership wants direct access, more adaptation, and a service team that understands how the business runs.

That can matter if the employer has:

| Buyer profile | Why local can work |

|---|---|

| Single-state operations | Less need for broad national compliance infrastructure |

| Complex employee relations issues | Easier access to the people handling day-to-day service |

| A strong internal finance team | Less dependence on a large platform for reporting discipline |

| Preference for flexible workflows | Greater chance of negotiated process exceptions |

A local PEO can also be effective for Chicago employers that don't want to feel like a small account inside a giant service model. But local service should not excuse weak technology, unclear implementation plans, or vague contract terms.

A provider doesn't get credit for being local if the onboarding process is sloppy, the reporting is weak, or support quality depends on one person staying employed.

The best way to compare the two is to write down the company's actual operating constraints. Number of states. Payroll complexity. Benefit expectations. Internal HR depth. Preferred service model. Then test each provider against those variables instead of the sales narrative.

For businesses weighing neighborhood familiarity against broader platform depth, this guide to a professional employer organization near me is a practical way to frame the trade-offs.

Navigating Illinois Compliance and PEO Contract Red Flags

The proposal deck does not control the relationship. The service agreement does. That's where the buyer finds out whether the PEO is really taking operational responsibility or administering tasks while the employer keeps most of the risk.

This matters more in Illinois than many sales teams admit. Local leave rules, payroll practices, and policy requirements create risk if responsibilities are fuzzy. A Chicago employer should ask direct questions: Who tracks ordinance changes? Who updates policies? Who handles notice requirements? Who responds if payroll tax handling becomes disputed?

The clauses that deserve legal review

Three areas need careful scrutiny.

First, renewal and fee escalation language. A contract may look competitive at signature and become expensive at renewal if the provider retains wide pricing discretion. Buyers should look for limits, notice requirements, and any language that allows repricing outside normal renewal events.

Second, termination provisions. Some agreements make it hard to exit cleanly. The red flags are long notice periods, automatic renewals, implementation cost clawbacks, and vague transition obligations. The provider's willingness to help during offboarding matters just as much as onboarding.

Third, liability allocation. Co-employment does not mean the PEO absorbs every problem. Contracts should clearly state who is responsible for payroll tax filings, employment practices support, workers' comp administration, and compliance task execution.

A useful outside perspective on payroll-related exposure is this discussion of expert insights on business tax liability. It's a reminder that buyers should never assume outsourced administration eliminates accountability.

What clear contract language looks like

Clear language assigns ownership. Vague language assigns confusion.

A strong contract should make these points easy to answer:

- Compliance support: Does the PEO merely provide information, or does it maintain policies, workflows, and required updates?

- Payroll responsibility: Who files, who remits, who corrects errors, and who communicates with agencies?

- Service commitments: Are there named contacts, documented response expectations, and escalation steps?

- Exit mechanics: How are employee records, payroll histories, benefit files, and timing handled at separation?

Below is a simple review lens:

| Contract issue | Cleaner language | Red flag language |

|---|---|---|

| Renewal | Defined notice and review process | Automatic increases with broad provider discretion |

| Termination | Specific exit steps and data-transfer duties | Penalties or vague offboarding support |

| Liability | Named responsibilities by function | General disclaimers and broad client indemnity |

| Compliance | Task ownership tied to process | “Advisory only” wording without execution clarity |

Chicago employers don't need a perfect contract. They need one that removes ambiguity from the expensive parts.

For legal and finance teams reviewing those points line by line, this list of PEO contract negotiation red flags is a practical companion to counsel review.

Using Data to Negotiate Your PEO Agreement

A 75 person Chicago company gets a PEO quote that looks manageable at first glance. Then finance separates the numbers. A 3% admin fee on a $6.5 million payroll is $195,000 a year before benefit markups, setup fees, and renewal changes. That is the point where negotiation should start, not end.

PEO proposals are pricing packages, not fixed market rates. A serious buyer compares the full spend against the current broker and payroll stack, an ASO model, and at least one competing PEO bid. NAPEO notes in its industry overview that PEO adoption is established among small and midsize employers. In Chicago, that means providers know buyers have alternatives, and buyers should act like it.

What to ask for instead of accepting the first proposal

Start with a normalized cost sheet. If one provider quotes a percent of payroll and another quotes per employee per month, put both into annual dollars using the same headcount, payroll, and benefit assumptions. Without that step, the cheaper quote is often just the less transparent one.

The requests should be concrete:

- Get fee separation in writing: Break out admin fees, payroll charges, technology fees, implementation costs, and benefit-related loads.

- Push on setup charges: Ask for implementation fees to be reduced, credited in month one, or waived at a defined employee count.

- Control renewal exposure: Ask for a cap, or at minimum, a defined notice period and a line-item explanation for any increase.

- Reduce exit cost: Require clear data-return timing, payroll file transfer support, and narrow termination penalties.

- Set service terms: Name the account team, response expectations, and escalation path.

One market option buyers use at this stage is PEO Metrics, which compares pricing structure, benefits, service model, and contract terms across providers. The value is simple. It gives HR and finance teams a side-by-side view they can use in the room.

How to frame the negotiation

Keep the discussion commercial. Chicago employers get better terms when they show the provider exactly how the quote will be judged.

A useful position sounds like this:

“We are comparing this against our current broker, payroll, and HR admin costs on a matched basis. We need clear annual cost, predictable renewal language, and a workable exit process. If you can improve those points, we can evaluate the service model seriously.”

That changes the burden of proof. The rep now has to justify total cost and contract structure instead of repeating feature lists.

For example, if a provider quotes 2.8% of payroll for a company with $8 million in wages, that fee alone is $224,000 a year. If another provider quotes $145 per employee per month for 80 employees, the annual admin cost is $139,200. The percent-of-payroll offer may still win if benefits are materially better, but at least the trade-off is visible. That is the kind of math that creates negotiating room, especially in Chicago where medical plan differences can swing total employer cost fast.

Teams that connect this analysis to broader headcount planning usually make better decisions. Resources on smarter workforce strategies can help leadership tie PEO structure, hiring plans, and manager reporting back to operating decisions.

The strongest buyers do three things well. They benchmark total annual cost, document the contract terms they need before legal review, and run a real comparison between credible options. Asking for a “best price” rarely changes much. Showing a provider where its quote loses on dollars, renewal risk, or exit terms usually does.