A finance leader reviews an EPLI quote, sees the premium, and immediately asks whether the number is reasonable. A second proposal lands from a PEO, and EPLI appears inside a bundled fee with little visibility into what portion pays for insurance, what portion pays for HR support, and what portion buys administrative convenience. That's where bad comparisons start.

EPLI insurance cost isn't just the premium line. It's the combination of premium, deductible, coverage design, exclusions, claims handling, and how much employment risk the company is shifting off its own balance sheet. A standalone policy and a PEO's master policy can both say “EPLI,” but they don't create the same financial outcome when a claim arrives.

For an HR director or CFO, the practical question is simple. Which structure creates the better total cost of risk for this workforce, in these states, with this management team, and with this claims profile? That requires reading past the headline price and looking at who controls the policy, who participates in defense, and which employment issues are covered narrowly, broadly, or not at all.

A useful starting point is to separate insurance from education. Basic overviews of employment practices liability coverage explain the core function of the policy, while a PEO evaluation also requires understanding how PEO insurance works inside a co-employment arrangement. Those are related decisions, but they're not the same decision.

Table of Contents

- Introduction Beyond the Premium

- Deconstructing EPLI Cost Averages Ranges and Per-Employee Metrics

- The 6 Factors That Actually Drive Your EPLI Premium

- Standalone EPLI vs PEO Coverage A Head-to-Head Comparison

- Actionable Strategies for Reducing Your EPLI Costs

- Your Checklist for Benchmarking EPLI in a PEO Proposal

Introduction Beyond the Premium

Most employers don't misjudge EPLI because they ignore risk. They misjudge it because the quote format hides the true economics. A standalone policy shows a visible annual premium and deductible. A PEO often embeds employment risk financing inside a broader service fee, which makes the insurance look cheaper than it may be, or more expensive than it really is, depending on how the proposal is structured.

That distinction matters most in the middle market. A company with multiple supervisors, active hiring, terminations, and operations across more than one state doesn't have a simple insurance-buying problem. It has a workforce-risk-financing problem. EPLI is only one part of that equation. HR process quality, handbook discipline, manager training, and claim escalation procedures all affect the cost that ultimately lands on the employer.

Practical rule: If the review starts and ends with premium, the buyer is measuring accounting cost, not financial exposure.

A CFO should look at EPLI the same way any other contingent liability gets evaluated. Start with the expected cash outlay under a claim. Then review defense structure, retention, sub-limits, exclusions, and whether the policy sits cleanly with the company's actual employment practices. The PEO question comes after that. It doesn't replace it.

The smartest comparison isn't “standalone policy versus bundled policy.” It's “which structure leaves fewer surprises once counsel is involved, documents are requested, and the company has to decide whether to defend, settle, or both.”

Deconstructing EPLI Cost Averages Ranges and Per-Employee Metrics

A CFO reviewing two EPLI options can get misled fast. One quote shows a $2,665 annual premium and a $10,000 deductible. Another comes through a PEO with no clean standalone premium line at all. If the review stops at the visible insurance number, the company can miss the larger cost structure behind the risk.

For a small business, Insureon's EPLI cost data puts the average premium at $222 per month or $2,665 per year, with an average deductible of $10,000. The same source shows how wide the spread can be by industry. Healthcare facilities average $409 per month, consulting firms $355, nonprofits $92, and insurance professionals $202.

What the baseline numbers tell a buyer

Use those figures as orientation, not as a buying rule.

The average premium gives a rough starting point for a small employer. The deductible matters just as much, because it is immediate working-capital exposure once a claim is opened. And the industry spread explains why generic “average EPLI cost” articles are often least useful to the employers that most need the coverage.

That is the first trade-off to keep in view. A low premium can still produce a bad financial result if the retention is too high for the company's cash position or if the policy structure leaves too much of the defense bill with the employer.

Per-employee pricing can help with budgeting, but it is only a rough normalization tool. Underwriters do not price EPLI the way they price a simple benefits line item. Two companies with the same headcount can land far apart on premium because one has frequent terminations, inconsistent documentation, or employees spread across tougher legal venues.

Why averages break down so quickly

Average-cost content compresses a messy market into one digestible number. That helps with search traffic. It does not help much with capital planning.

A better way to read the market is as a range of possible outcomes. Some very small employers can buy coverage near the low end of the market, while firms with a few dozen employees can see pricing move sharply higher once claims history, management practices, class of business, and state exposure start to stack up. The premium range matters because it shows how little decision value there is in a single headline average.

That matters even more in a PEO comparison. In a standalone purchase, the premium, deductible, and limit are usually visible. In a PEO arrangement, part of the value may come from shared HR infrastructure, policy templates, supervisor guidance, and earlier claim escalation. Those services can reduce claim frequency or improve defense posture, but they can also make the insurance cost harder to isolate.

So the right question is not, “What does EPLI cost on average?” The better question is, “What is my expected cash exposure under each structure if a manager decision turns into a defended claim?”

That is why I usually tell finance teams to build a simple side-by-side model with four lines: visible premium, deductible or retention, expected uncovered defense or carve-outs, and the value of any risk-control support tied to the arrangement. If the PEO quote looks lower, test whether the savings come from pooled buying power, different limits, narrower terms, or a service bundle that changes claim handling before counsel gets involved. A tool like this PEO insurance pooling savings estimator can help frame that comparison in cost terms instead of marketing terms.

The goal in this section is not to pin your company to an “average” EPLI number. It is to avoid using average numbers as a substitute for underwriting reality.

The 6 Factors That Actually Drive Your EPLI Premium

A CFO usually sees the quote first. The underwriter sees something else entirely: hiring volume, manager judgment, complaint handling, termination discipline, and the odds that a routine employee dispute turns into a defended claim.

Two companies can have similar payroll, similar revenue, and very different EPLI pricing because they create different claim conditions. Underwriters price frequency and severity. They also price how expensive your internal process failures may be once outside counsel gets involved.

What underwriters are pricing

The first factor is industry risk. High-turnover employers, healthcare groups, hospitality operators, staffing-heavy businesses, and companies with frequent employee discipline tend to draw more scrutiny than firms with stable teams and cleaner supervision structures.

The second is employee count. More employees create more hiring, promotion, accommodation, leave, discipline, and termination decisions. The underwriting issue is not just size. It is the number of opportunities for inconsistency.

Third is where your employees work. Multi-state employers bring more legal variation, more procedural complexity, and more room for technical mistakes. A company operating in one employer-friendly state is usually easier to underwrite than a company spread across several jurisdictions with stricter worker protections.

Fourth is loss history. Prior allegations matter even when they did not produce a settlement. An underwriter will still ask what happened, what changed, and whether the same management pattern could produce another claim.

Fifth is policy structure. Limits, retention, defense treatment, exclusions, and endorsements all move price. A lower premium can be a poor trade if it comes with a higher retention, narrower coverage, or terms that leave the employer absorbing more of the legal bill.

Sixth is HR control quality. Here, quotes often separate. Underwriters look for written policies, complaint intake procedures, manager training, documentation standards, investigation discipline, and consistent termination review. Companies with weak controls often pay more because the insurer expects more disputes and a harder defense.

Here is the six-factor view in plain terms:

Industry profile

Some sectors generate more employee friction and more claim activity than others.Headcount and supervisor count

More people usually means more decision-makers, and more decision-makers increase variance in how policies are applied.State exposure

Compliance gets harder as your workforce spreads across jurisdictions with different rules.Prior complaints and claims

Even weak allegations can shape the underwriter's view of future risk.Limits and retention

Higher limits and lower out-of-pocket retention usually cost more, but they may reduce balance-sheet volatility.HR process discipline

Good documentation and manager controls can improve both pricing and claim defensibility.

The factor many buyers underweight

The sixth factor often has the biggest strategic value because it affects more than premium. It affects how a claim behaves after it starts.

Boardroom takeaway: Underwriters reward documented controls, not verbal assurances.

This is also the point where the standalone versus PEO decision starts to matter. A PEO does not make employment claims disappear, but co-employment can change supervision standards, documentation practices, escalation paths, and termination review. If those controls are stronger, the risk profile can improve. If responsibilities are vague, the arrangement can create its own friction. That is why finance teams should examine not just the insurance line item, but also who owns each employment decision and how disputes are documented. The exposure in a termination claim often turns on that split, which is why this guide on PEO liability in wrongful termination claims is relevant to cost modeling as much as legal responsibility.

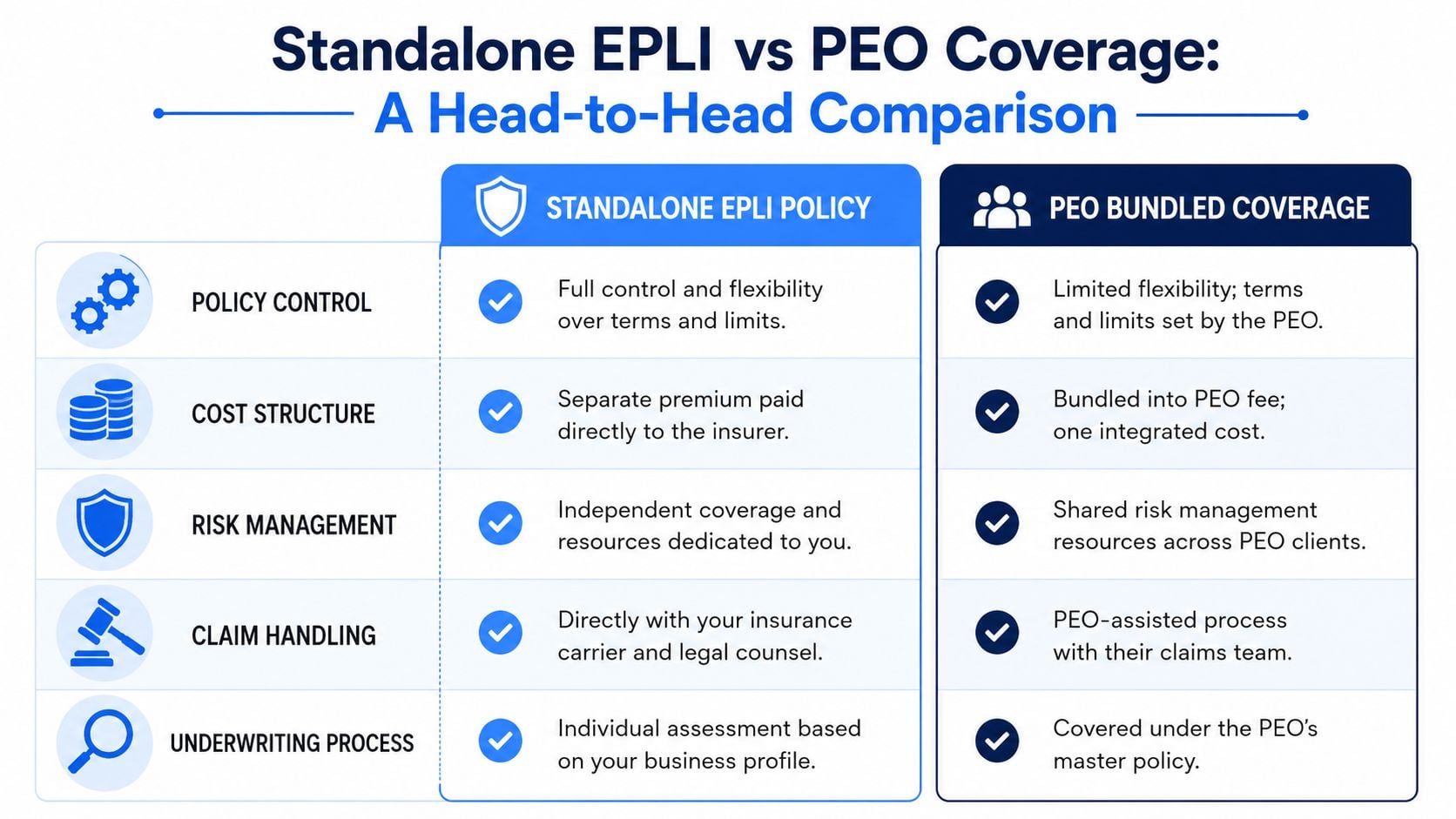

Standalone EPLI vs PEO Coverage A Head-to-Head Comparison

This is the decision that matters for many employers. A standalone policy buys direct control and direct visibility. A PEO arrangement may buy a different package entirely: EPLI access, shared processes, HR infrastructure, and co-employment mechanics that can either improve risk discipline or create confusion if the contract language is weak.

Where the financial trade-offs really sit

A standalone policy is usually simpler to model. The employer sees the premium, sees the deductible, negotiates limits, and knows which broker and carrier are involved. That's useful for companies that want direct control over terms and don't want insurance embedded in a broader outsourcing relationship.

But standalone EPLI doesn't solve process failures. If managers are poorly trained, terminations are inconsistent, or complaint handling is weak, the employer may still be buying insurance after the risk has already formed.

A PEO can change that equation because the value isn't only the policy. The value may also sit in standardized onboarding, handbook support, compliance guidance, and more disciplined HR workflows. That matters because some of the claim types employers worry about today sit outside the narrow examples often used in basic EPLI discussions. Coalition's discussion of EPLI exposure notes that EPLI can extend beyond wrongful termination and discrimination into areas such as wage-and-hour disputes, overtime issues, invasion of privacy, defamation, illegal background checks, and employee benefit plan mismanagement. The same discussion also notes that some of these exposures may be limited, excluded, or only partially addressed depending on the form.

That creates an important comparison point. A standalone policy may provide clearer insurance wording, but a PEO may reduce the chance of certain administrative mistakes in the first place.

The cheaper insurance structure often isn't the one with the lower visible cost. It's the one that reduces both claim frequency and claim friction.

Comparison table

| Factor | Standalone EPLI | PEO-Provided EPLI |

|---|---|---|

| Policy control | Employer usually has more direct input on limits, deductible, endorsements, and broker relationship | Terms may sit inside a master policy or bundled structure with less direct customization |

| Cost structure | Separate premium and separate deductible are easier to isolate in a budget | Insurance cost may be blended into broader service pricing |

| Risk management | Employer builds or buys its own HR controls and training support | PEO may bundle handbook, HR guidance, and workflow support alongside coverage |

| Claim handling | Employer typically works through its broker, carrier, and appointed counsel structure | PEO may play a central role in notice, intake, defense coordination, or escalation |

| Underwriting lens | Carrier underwrites the employer on its own profile | Coverage may reflect pooled or master-policy dynamics within a co-employment framework |

| Coverage fit for newer exposures | Depends heavily on policy wording and endorsements | May be paired with compliance support that helps reduce some operational risks before they become claims |

A serious buyer should review the master-policy question carefully. If the PEO relationship relies on pooled insurance economics, the right comparison isn't just “what are the limits?” It's also “how does this master arrangement apply to this employer's actual claim behavior?” A master policy versus standalone policy comparison can help isolate that issue.

Which model tends to fit which buyer

A standalone approach often fits employers that already have mature internal HR, want direct broker access, and prefer to negotiate insurance language independently from payroll and benefits administration.

A PEO structure often fits employers that want operational support tied to risk control. That can be especially relevant for businesses with lean HR teams, rapid hiring, or uneven supervisor experience.

Neither option is automatically better. The right question is narrower:

- Choose standalone EPLI when direct policy control matters more than bundled HR infrastructure.

- Lean toward a PEO model when the employer needs process discipline as much as insurance.

- Push deeper in either model when the company has multi-state complexity or concern about modern claim categories that standard forms may address unevenly.

One practical note belongs here. If a buyer wants outside help evaluating the insurance and contract structure inside PEO proposals, firms such as PEO Metrics can isolate those components as part of a side-by-side comparison. That's useful when bundled pricing makes the EPLI piece hard to benchmark cleanly.

Actionable Strategies for Reducing Your EPLI Costs

Employers rarely reduce EPLI cost by shopping alone. They reduce it by becoming easier to underwrite and easier to defend. That starts before the application and continues through every hiring, discipline, leave, and termination decision.

For standalone buyers

The first move is tightening documentation. Weak records make even defensible employment decisions harder to support. A clean paper trail helps both underwriting and claims response.

The second move is manager discipline. Supervisors create most of the facts that later become exhibits. If managers improvise feedback, skip performance discussions, or treat similar situations differently, the policy may respond but the claim gets more expensive.

A practical checklist for standalone buyers:

- Rebuild the handbook: Update policies so they reflect actual practice, not copied language that no one follows.

- Train frontline managers: Focus on hiring, accommodations, complaints, discipline, and termination escalation.

- Document consistently: Performance notes, warnings, investigations, and exit materials should be complete and dated.

- Market the risk properly: A broker can only position the account well if the employer can show real controls.

For finance teams reviewing the broader insurance program, an outside framework such as this guide to reviewing business insurance can help pressure-test whether EPLI is being evaluated alongside the rest of the company's risk stack rather than in isolation.

For PEO buyers

The most effective way to lower total EPLI-related cost in a PEO setting is to use the PEO's infrastructure fully. Many employers buy co-employment support and then continue operating with inconsistent local practices. That wastes part of the value.

A better approach is to ask the PEO to standardize what creates claim noise. That often includes onboarding templates, separation review steps, handbook administration, manager escalation channels, and complaint intake procedures.

Good EPLI economics usually come from fewer preventable mistakes, not from finding the thinnest premium.

Useful actions in a PEO model include:

- Route sensitive terminations through a review process: Don't let local managers act alone on high-risk exits.

- Use the PEO's handbook and HR tools: Standardization improves consistency.

- Ask for claim-prevention support, not just claims reporting instructions: Prevention services are part of the value equation.

- Benchmark the prevention side as well as the policy side: A resource on PEOs for lawsuit prevention helps frame that discussion.

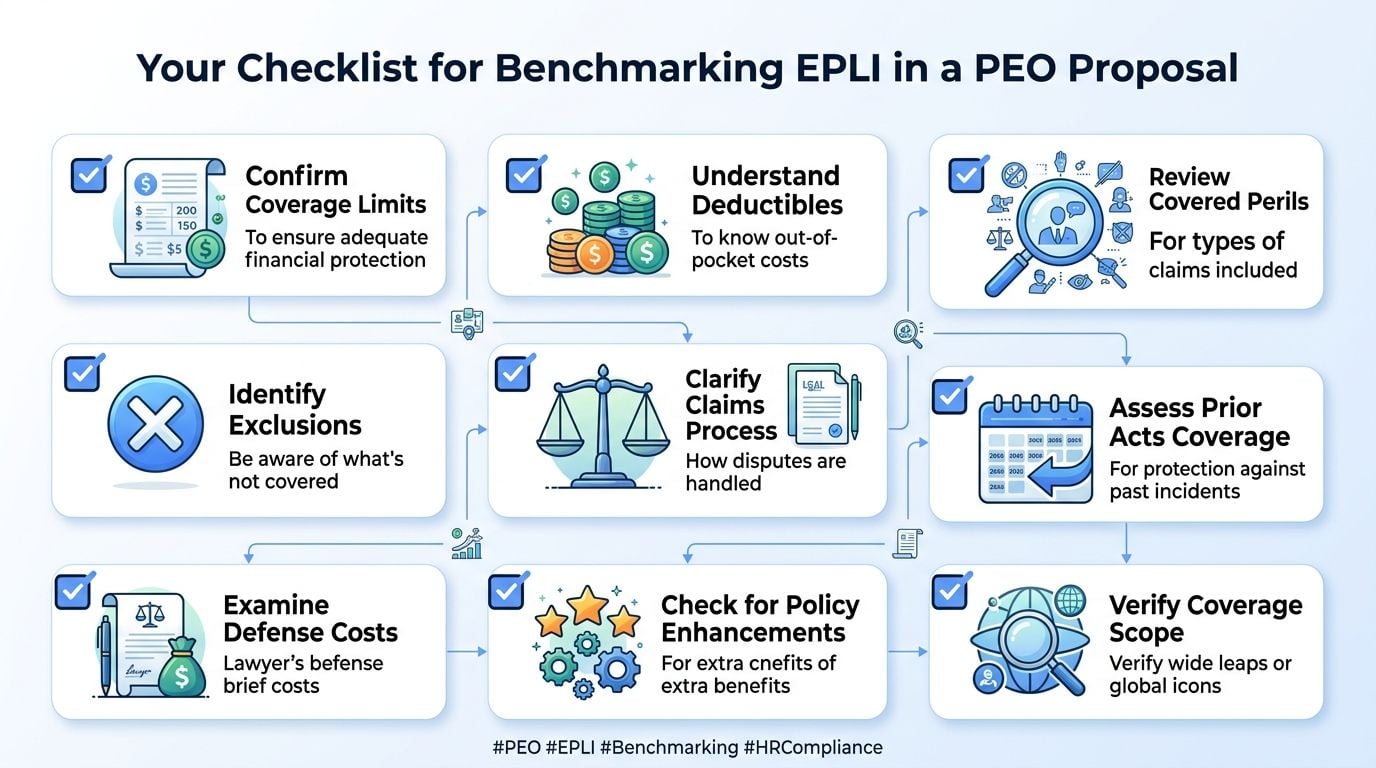

Your Checklist for Benchmarking EPLI in a PEO Proposal

PEO proposals often make EPLI sound simple. It isn't. The insurance may sit inside a service agreement, a master policy, or a summary that doesn't fully explain sub-limits, exclusions, defense control, or how the employer participates in a claim. A CFO should assume the default proposal is incomplete until the details are confirmed.

Questions that belong in every proposal review

Use this checklist in the proposal meeting, not after signature:

- What are the actual EPLI limits? Ask for the coverage amount, not a summary phrase.

- What deductible or retention applies to this employer? If the answer is “it depends,” ask on what.

- Who is the named insured and how is the client employer included? Co-employment language matters.

- Which claim types are covered, limited, or carved out? Ask specifically about wage-and-hour, privacy-related issues, retaliation, and benefit-plan administration concerns.

- Who controls defense counsel and settlement decisions? This affects both spend and strategy.

- How are claims reported? A delayed notice problem can become a coverage problem.

- Is prior-acts coverage addressed? Buyers need to know whether past conduct is within scope or excluded.

- What support is available before a claim? Handbook review, training, hotline support, and termination review change the actual cost equation.

What to push on in negotiation

PEO buyers sometimes assume bundled insurance terms are fixed. Large accounts know that's not always true. A useful real-world reminder comes from a public-sector example. In a 2025 board report, the Housing Authority of the City of Los Angeles approved $10 million of EPLI coverage for a premium not to exceed $424,050, down from $442,170 in 2024, a decrease of about 4.1%, according to the Housing Authority of the City of Los Angeles board report. That example doesn't map directly to the middle market, but it does prove the larger point. EPLI pricing and structure can move when underwriting conditions improve and buyers ask better questions.

That's why negotiation should focus on more than the fee.

Push on these items:

- Coverage clarity: Ask for actual policy wording or a detailed summary of terms.

- Employer-specific application of the master policy: Don't accept generic statements about pooled protection.

- Claims protocol: Confirm who takes the first call, who appoints counsel, and who approves strategy.

- Operational support: Tie the insurance discussion to termination review, handbook updates, and complaint escalation.

A PEO proposal with unclear EPLI terms isn't cheaper. It's just harder to model.

When a company is comparing PEOs and needs to isolate how EPLI is structured inside each proposal, PEO Metrics provides independent side-by-side analysis of pricing, insurance components, contract terms, and risk trade-offs so HR and finance teams can benchmark what they're buying before they sign.