A PEO renewal is often where EPLI questions surface. The payroll service works. Benefits are in place. HR support seems adequate. Then legal asks a simple question after a termination dispute: who is carrying the employment claim risk, under what policy, and with what limits?

That's when a lot of finance and HR teams realize they've accepted employment practices liability insurance, or EPLI, as a bundled feature instead of evaluating it like a material balance-sheet protection. That's risky. EPLI is generally written on a claims-made basis and is designed to cover financial losses from employment-related allegations such as discrimination, harassment, wrongful termination, retaliation, and defamation, with coverage typically extending to defense costs, settlements, and judgments rather than the underlying employment act itself, as outlined by the Insurance Training Center's explanation of EPLI.

For companies using a PEO, the issue isn't just whether EPLI exists. The issue is whether the structure works when a claim lands, when the PEO relationship ends, and when leadership needs clarity fast.

Table of Contents

- The Demand Letter Every Business Owner Dreads

- What EPLI Actually Covers And Excludes

- Decoding Your EPLI Policy Structure

- The Real Cost of EPLI and What Drives Premiums

- EPLI vs Workers Comp and Other Business Insurance

- Evaluating EPLI Within a PEO Agreement

- Key Takeaways for Your Leadership Team

The Demand Letter Every Business Owner Dreads

It usually starts with a former employee, outside counsel, and a certified letter that reaches the CFO, HR director, or owner late in the day. The allegations may read like a checklist: wrongful termination, discrimination, retaliation, reputational harm. The business problem starts immediately. Legal costs begin before anyone knows whether the claim has merit.

That's why Employment Practices Liability Insurance matters. It exists for one of the most common modern management risks: allegations tied to how a business hires, manages, disciplines, and separates employees. It's not a nice-to-have add-on. It's a financial backstop for a category of claims that can drain cash, management time, and lender confidence.

One industry summary notes that EPLI lawsuits increased by 400% over the last two decades, and that the EEOC received about 61,000 charges in 2021 versus an average of 86,354 over the prior 10 years, according to Coalition's overview of why businesses need EPLI. The exact trend line matters less than the operating reality. Employment disputes are routine business risk now, not an edge case.

For nonprofit and mission-driven employers, screening and hiring practices can create separate legal exposure that sits outside the classic EPLI discussion. Teams reviewing background check procedures may find this guide on understanding FCRA for charities useful because screening compliance failures often become part of a broader employment dispute.

The first mistake most employers make isn't mishandling the claim. It's assuming the insurance bundle in a PEO agreement answers every employment risk question.

In a PEO relationship, shared employment responsibilities can make the legal picture feel blurred. That's exactly why leadership teams should understand how co-employment affects accountability, especially in light of joint employment enforcement risks under DOL rules. If the claim names both the employer and the PEO, vague assumptions about “covered under the PEO policy” won't help much.

What EPLI Actually Covers And Excludes

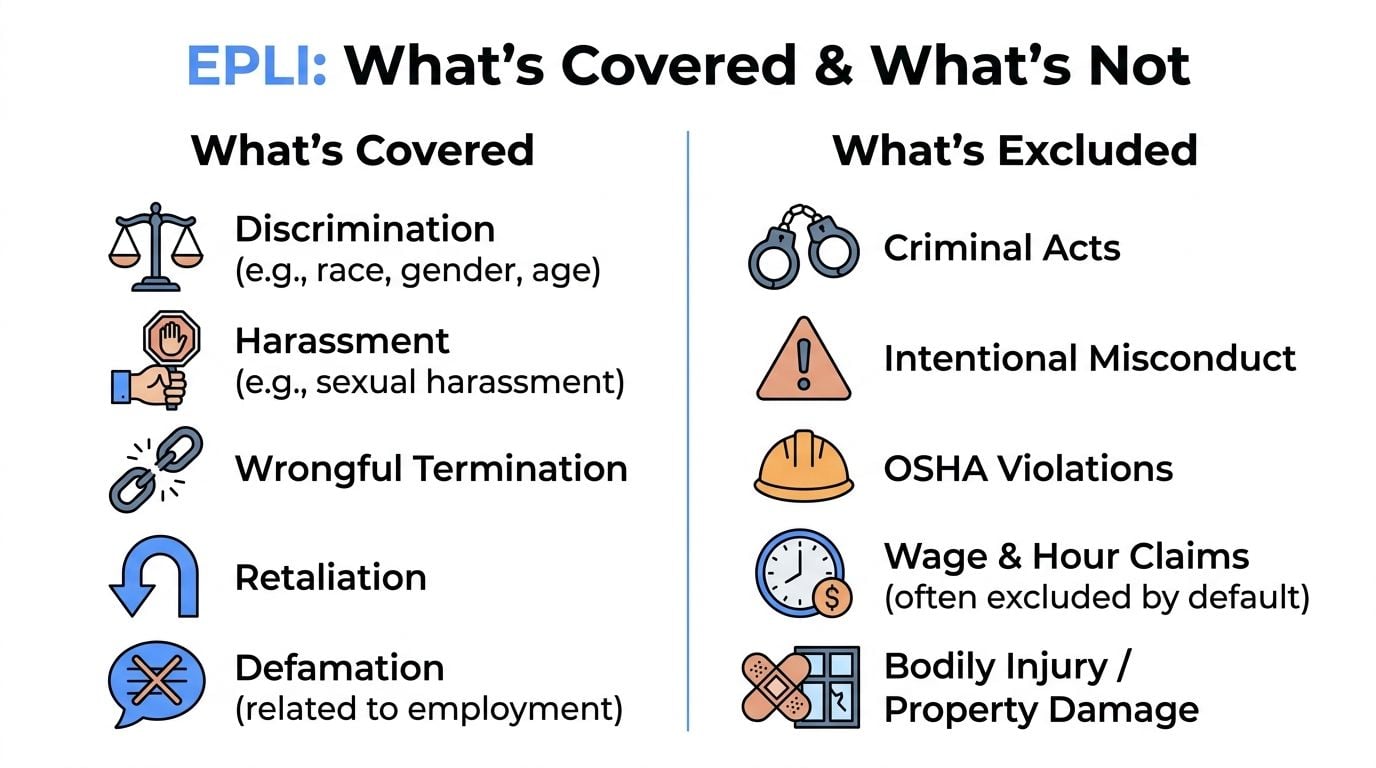

The most expensive misunderstanding in this category is treating EPLI like a catch-all employee lawsuit policy. It isn't. The policy usually protects against certain employment-related allegations and usually leaves other categories with the employer.

Covered allegations that usually trigger EPLI

Standard EPLI is designed to respond to allegations such as discrimination, harassment, wrongful termination, retaliation, and defamation tied to employment. That basic scope is summarized in this explanation of EPLI coverage fundamentals, and it aligns with common market practice.

A few examples make the boundary clearer:

- Discrimination claims can arise when a former employee alleges a layoff decision was based on age, disability, sex, race, or another protected characteristic.

- Harassment claims often involve a hostile work environment allegation tied to a manager, coworker, or weak reporting response.

- Wrongful termination claims may follow a firing that the employee says violated public policy or masked another unlawful motive.

- Retaliation claims often show up after an employee reported misconduct, requested leave, or raised a workplace concern.

- Defamation in an employment context can emerge when the company's statements about the employee's departure allegedly damaged reputation.

What the policy generally pays for is just as important as what it covers. The insurance is meant to address the financial loss from the allegation, including defense costs, settlements, and judgments.

Exclusions that create the biggest surprises

The hidden risk in EPLI is almost always in the carve-outs.

Benchmark policy guidance says many EPLI forms exclude or sharply limit contract-based claims and certain statutory exposures. Some insurers offer defense-cost coverage for allegations involving FMLA or wage-and-hour law violation, often through endorsements or sublimits, as discussed in ABHE's guidance on EPLI design issues.

That leads to a practical covers-versus-excludes framework:

| Issue | Often covered | Often excluded or limited |

|---|---|---|

| Wrongful termination allegation | Yes | No |

| Harassment allegation | Yes | No |

| Retaliation allegation | Yes | No |

| Unpaid overtime class claim | Sometimes defense only, if endorsed | Often excluded by default |

| Breach of employment contract | Limited or excluded | Often excluded |

| Employee physical injury at work | No | Falls to workers' comp or employer's liability |

| Criminal acts | No | Excluded |

Practical rule: If a claim sounds like “you treated me unlawfully as an employee,” EPLI may respond. If it sounds like “you underpaid me under a statute,” “you breached a contract,” or “I was physically injured,” assume there's a gap until the policy proves otherwise.

For employers inside a PEO, those exclusions matter more because the bundled policy may look broad in a proposal but narrow in the actual form. Wage-and-hour defense coverage, third-party coverage, and contract exclusions deserve line-by-line review.

Decoding Your EPLI Policy Structure

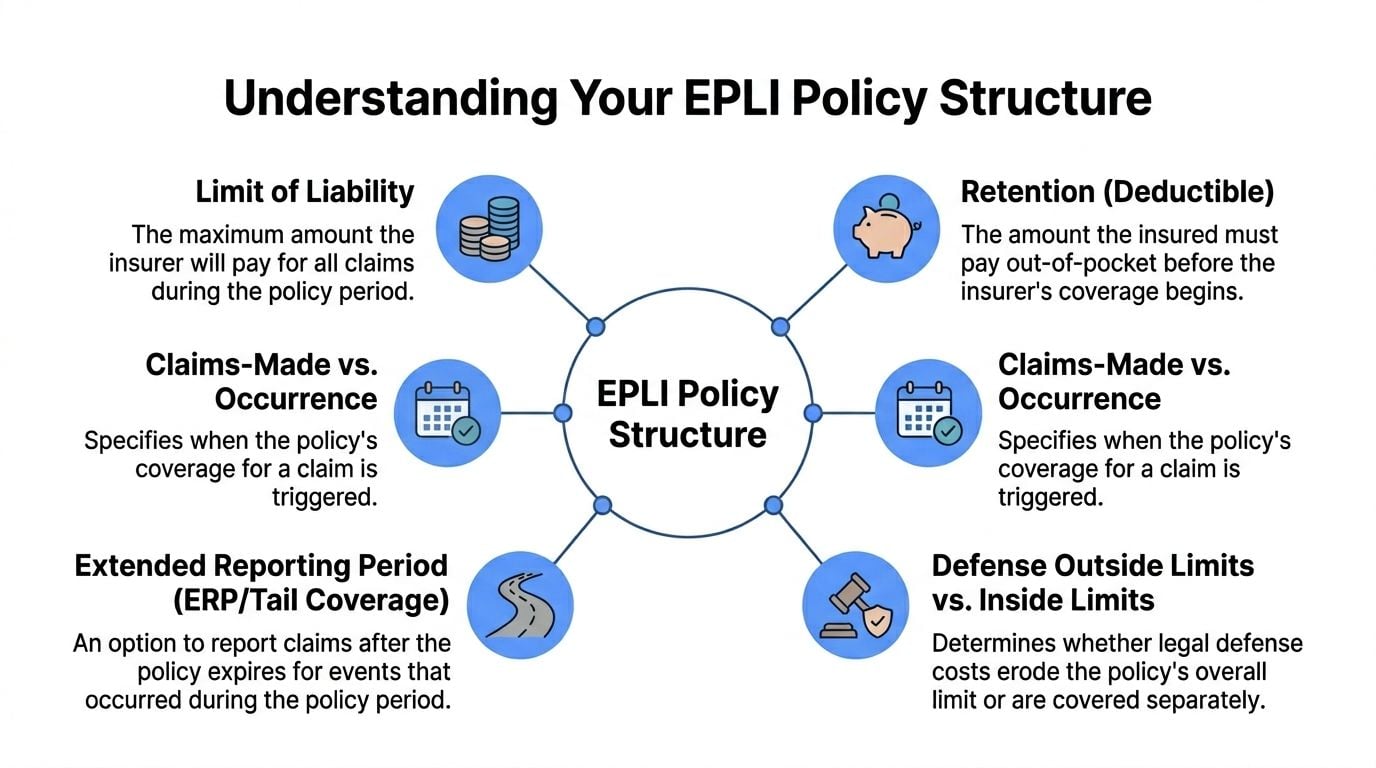

Most buyers focus on the limit first. That's understandable, but it's incomplete. EPLI is contract language plus timing rules. If those rules don't line up with the company's history, the policy can look solid on paper and still fail when needed.

Why claims-made changes the buying decision

EPLI is usually written on a claims-made basis, meaning coverage is triggered when the claim is first made and reported during the policy period, not when the underlying employment act occurred. That structure makes continuity, prior-acts dates, and extended reporting provisions especially important in switches, mergers, and renewals, as explained in IRMI's definition of EPLI.

A business analogy helps. A claims-made policy works less like a permanent warranty and more like an active subscription. If the company cancels, moves to a different carrier, or exits a PEO without preserving continuity, an old employment act can turn into a newly uncovered claim.

That's where buyers get burned during transitions. A manager terminates an employee in June. The employee hires counsel months later, after the company has already moved out of the PEO or shifted carriers. If the reporting rules and prior-acts terms don't line up, leadership may discover the claim falls between policies.

For readers who want a plain-language overview of employment practices liability insurance, broker resources can be useful. The key point for finance leaders isn't the definition. It's the continuity risk.

The terms that deserve CFO attention

A serious review should focus on five items.

- Retroactive or prior-acts date. This tells the company how far back the policy reaches for wrongful acts that are later reported as claims.

- Extended reporting period, often called tail coverage. This can allow claims to be reported after the policy ends for acts that took place while the policy was active.

- Retention. This is the amount the employer pays before insurance starts responding. In a PEO arrangement, the retention may sit with the PEO, the client company, or both depending on contract wording.

- Defense costs inside or outside the limit. If defense erodes the limit, attorney fees reduce what remains for settlement or judgment.

- Run-off treatment during a PEO exit. If the company terminates the relationship, coverage continuity has to be handled deliberately.

A strong EPLI structure doesn't just insure the claim. It survives the company's organizational changes.

This is one reason bundled PEO insurance needs extra scrutiny. A buyer may not control the carrier, the form, or the renewal strategy. Before signing, it's worth understanding how PEO insurance is structured overall because the EPLI piece rarely operates in isolation.

The Real Cost of EPLI and What Drives Premiums

A CFO evaluating EPLI should price more than the annual premium. The harder question is how much employment-claim volatility the company is still carrying after the policy is in place.

That distinction matters because EPLI losses are uneven. Many companies go years without a major matter, then one termination, harassment allegation, or retaliation claim turns into six months of legal fees, management distraction, and a settlement discussion that was never in the budget. Advisen's employment claims research, summarized by IRMI, shows defense costs can be substantial even before a case reaches trial, which is why limit size and retention deserve as much attention as premium. See IRMI's discussion of employment practices liability trends and loss drivers.

What usually pushes pricing up or down

Underwriters price EPLI based on how the business hires, manages, disciplines, and terminates people.

- Headcount and growth rate affect claim frequency. More employees usually means more manager decisions and more opportunities for inconsistency.

- Industry mix affects severity. High-turnover, labor-intensive employers often present a different risk profile than firms with stable professional staff.

- State footprint affects both law and litigation behavior. Multi-state employers need to account for local compliance standards and a wider range of claim venues. That is one reason HR and finance teams should track workers' compensation requirements by state alongside EPLI exposures. A company operating in ten states rarely has a simple employment-risk profile.

- Turnover, layoffs, and complaint history matter. A company with repeated separations, weak documentation, or prior allegations will usually pay for that history.

- Manager quality matters more than many buyers expect. Underwriters know that poorly trained front-line supervisors generate expensive facts.

In practice, pricing often reflects process discipline as much as company size.

What carriers and PEOs tend to reward

The strongest submissions show that the company can prevent small employee issues from becoming formal claims.

A carrier or PEO underwriting team will usually look for:

- A current employee handbook that matches actual practice

- Manager training records for harassment, discrimination, retaliation, and leave issues

- A documented complaint and investigation process

- Termination review procedures for higher-risk separations

- Clear leave, accommodation, and wage-hour administration

For leadership teams comparing options, this guide to EPLI insurance cost benchmarks and buying variables can help frame the numbers.

One buying mistake shows up often in PEO arrangements. Leadership sees a competitive bundled price and assumes the EPLI piece is efficient. Sometimes it is. Sometimes the lower price comes from a shared limit, a high retention pushed back to the client, defense costs that eat into the limit, or narrow treatment of third-party claims. Those are finance issues, not technical footnotes.

Cheap EPLI can be expensive risk retention in disguise.

EPLI vs Workers Comp and Other Business Insurance

Leadership teams often discover coverage gaps because they assumed another policy would respond. The names sound similar. The triggers aren't.

Insurance training materials distinguish EPLI from workers' compensation and employer's liability insurance clearly: EPLI responds to employment-practices claims, while workers' comp and employer's liability address workplace injuries and illnesses. That distinction appears in the earlier cited Insurance Training Center material and is the starting point for clean program design.

A simple way to separate the policies

The easiest test is to ask what happened.

| Policy | Primary Purpose | Typical Triggering Event |

|---|---|---|

| EPLI | Covers financial loss from employment-related allegations | Employee alleges discrimination, harassment, retaliation, wrongful termination, or related employment misconduct |

| Workers' Comp | Covers workplace injury or illness | Employee slips on a wet floor, suffers a lifting injury, or develops a work-related illness |

| D&O | Covers claims tied to leadership decisions and governance | Investor, shareholder, or regulator alleges wrongful acts by directors or officers |

| General Liability | Covers third-party bodily injury or property damage | Visitor slips in the lobby or the company damages someone else's property |

A hostile work environment allegation points toward EPLI. A warehouse back injury points toward workers' comp. An investor claim tied to mismanagement points toward D&O.

For employers operating in several states, workers' compensation requirements by state can help clarify where workers' comp obligations start and how they differ by jurisdiction.

Where buyers get tripped up

The confusion usually comes from overlap in people, not overlap in policy trigger. The same supervisor can create an EPLI claim by retaliating against an employee and a workers' comp issue if the employee later reports a physical injury. Different facts. Different policies.

Coverage programs fail when the company buys by label instead of by claim trigger.

That matters in PEO arrangements because some buyers assume the PEO relationship automatically closes every insurance gap around employees. It doesn't. The company still needs to know which policy responds to which event and whether any important exposure sits outside the bundled structure.

Evaluating EPLI Within a PEO Agreement

A PEO can improve HR administration and give a smaller or mid-sized employer access to broader insurance purchasing. It can also hide risk behind convenience. “You're covered under our master policy” is not a sufficient answer for a CFO, HR leader, or board-level operator.

EPLI is generally written on a claims-made basis and is designed to cover financial losses from employment-related allegations such as discrimination, harassment, wrongful termination, retaliation, and defamation, with coverage extending to defense costs, settlements, and judgments, according to the already cited Insurance Training Center reference. Inside a PEO, the business question becomes more specific: what part of that protection belongs to the client, on what terms, and what happens when the relationship changes?

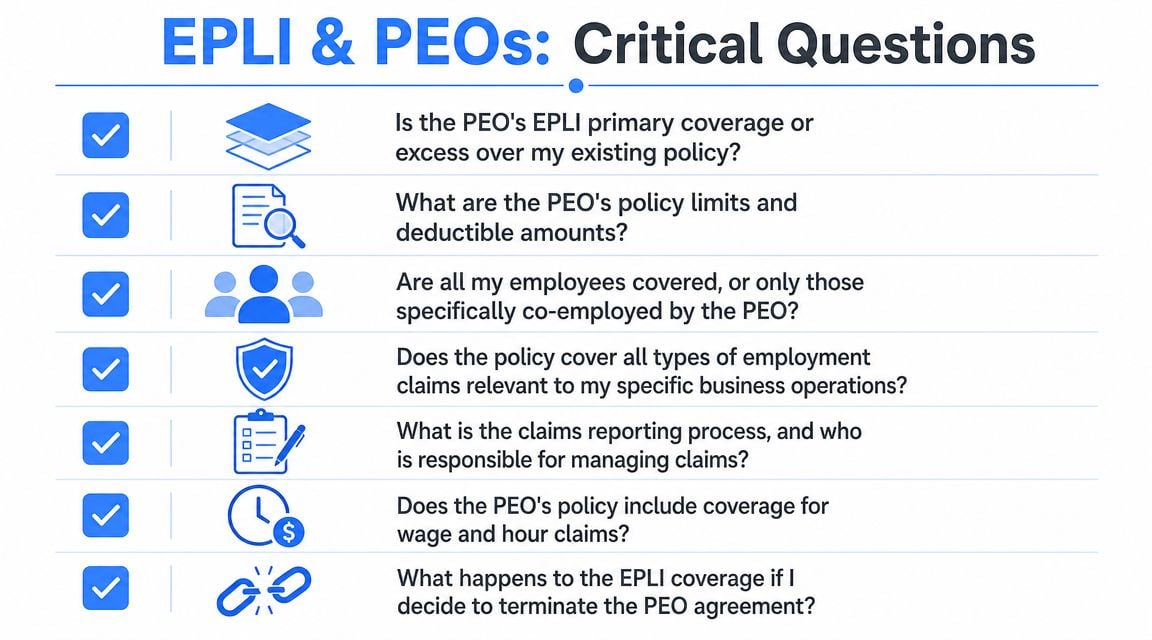

Questions that belong in every PEO review

These questions tend to quickly surface the inherent trade-offs:

- Is the PEO policy a master policy shared across many clients? Shared limits can work, but finance should know whether one client's large claim can reduce available protection for others.

- Who controls defense counsel and settlement decisions? If the PEO controls the defense, the client may have less say over strategy, messaging, and timing.

- Are wage-and-hour allegations covered at all, or only defense costs through a sublimit? This is one of the most common misunderstandings in bundled EPLI.

- Does the policy include third-party coverage? Customer, vendor, or visitor allegations can matter in retail, hospitality, healthcare, and service-heavy environments.

- Does defense spend erode the limit? If it does, the limit can shrink quickly in a hard-fought case.

- What happens at termination of the PEO agreement? This is often the most important question in a claims-made form.

A side-by-side review of PEO master policy versus standalone policy structures can help teams compare whether the convenience of a bundled structure is worth the control they may be giving up.

What a strong answer sounds like

The best PEO responses are concrete and documented. A strong answer identifies the insurer, the structure, the limit, the retention, who is insured, who controls claims, and what exit options exist. It also explains whether the client can buy separate standalone EPLI if the shared arrangement feels too thin.

Weak answers tend to sound broad and reassuring but vague. “Most claims are covered.” “This is standard.” “We've never had an issue.” None of those statements matter if the contract and policy form say something narrower.

A practical review meeting should ask for:

- The actual policy summary or specimen form.

- The client agreement language on indemnity and claims handling.

- Written clarification on tail coverage or extended reporting at exit.

- Confirmation of any sublimits for wage-and-hour, third-party, or defense-only features.

- A walkthrough of who reports claims and on what timeline.

If a PEO can explain its EPLI structure clearly before signing, it's usually a better operational partner after a claim arrives.

That's the true test. EPLI inside a PEO isn't just an insurance feature. It's a signal of how transparent the provider will be when risk becomes expensive.

Key Takeaways for Your Leadership Team

A claim often starts before anyone inside finance labels it a claim. A termination goes sideways, a manager is accused of misconduct, HR receives a lawyer's letter, and the first question is not whether coverage exists in theory. The question is whether the company can control cost, defense, and disruption under the policy structure it bought.

Leadership teams should treat EPLI like any other balance-sheet protection tool. Read it the way you would read a credit agreement or a vendor indemnity. If coverage sits inside a PEO arrangement, evaluate it as a financing and control decision, not just an HR benefit.

A final decision checklist

For CFOs, HR leaders, and owners, this is the most useful screen:

- Confirm the trigger. Identify which allegations are covered and which are carved out before a dispute forces the answer.

- Check the structure. Claims-made wording, prior-acts treatment, and tail options matter most at renewal, after leadership changes, and during a PEO exit.

- Test the economics. A low premium does not help if the company still carries a large retention, shrinking limits, or defense costs that burn through the policy.

- Map the overlap. Separate EPLI from workers' comp, employer's liability, D&O, and general liability based on what event activates each policy.

- Press on the PEO terms. Confirm whether limits are shared, who appoints counsel, who decides on settlement, whether defense reduces limits, and what protection remains after termination of the PEO agreement.

Specific, written answers matter. Vague reassurance does not.

The primary exposure sits where the company faces a disputed termination, a manager misconduct allegation, a multi-party claim, or a PEO transition. That is why the key question is not only whether a PEO offers EPLI. It is whether the structure gives the company enough control and enough limit when a claim becomes expensive.

If a company is comparing PEOs, renewing an existing agreement, or trying to pressure-test bundled EPLI terms before signing, PEO Metrics helps HR and finance teams evaluate the trade-offs side by side. That includes policy structure, shared-limit concerns, exit provisions, contract language, and overall PEO risk so leadership can make a cleaner decision before a claim tests the paperwork.