Most advice about what is PEO payroll gets the basic definition right and the buying decision wrong. It treats a PEO like a fancier payroll processor. That framing misses the part that matters to a CFO or HR leader: a PEO changes how payroll tax filing, compliance responsibility, benefits access, and contract risk are organized around the business.

That's why this isn't a simple vendor choice. It's a financial model, a liability decision, and an operating model decision rolled into one. The U.S. PEO industry has a footprint of $136 to $156 billion in gross revenues, serves 2.7 to 3.4 million worksite employees, and has added an average of 100,000 worksite employees and 6,000 net new clients annually over the past 30 years, which shows how established the model has become in the SMB market, according to World Insurance's summary of PEO industry statistics.

Finance teams that evaluate PEOs correctly usually start with accounting treatment, tax handling, contract structure, and total cost, not the sales demo. A useful companion on that front is this explanation of PEO accounting treatment, especially for teams deciding how to model expenses and liabilities before they sign.

Table of Contents

- PEO Payroll Is More Than an Expense Line Item

- How PEO Payroll Works The Co-Employment Model

- PEO Payroll vs ASO and In-House Payroll

- The Strategic Benefits and Hidden Risks

- Decoding PEO Pricing and Total Cost of Ownership

- How to Evaluate and Select the Right PEO Partner

PEO Payroll Is More Than an Expense Line Item

A Professional Employer Organization, or PEO, provides payroll and HR services through a co-employment arrangement. The PEO becomes the employer of record for certain tax and compliance purposes, while the client company keeps control of hiring, firing, pay decisions, and daily management. That's a very different setup from outsourcing payroll processing alone.

Most weak buying decisions start with one bad assumption: “Payroll is payroll.” It isn't. A payroll processor helps run a function. A PEO changes the structure around that function.

Why finance leaders should care

For finance, PEO payroll touches more than wage calculation. It affects tax filing mechanics, workers' compensation administration, benefits administration, compliance support, audit exposure, and the way service fees show up in planning models.

For HR, the decision is just as material. A PEO can strengthen infrastructure fast, especially for a company that has outgrown spreadsheets, a small HR team, or a patchwork of brokers and point solutions.

A PEO should be evaluated like a bundled risk-and-operations contract, not a commodity payroll line.

What basic definitions leave out

A generic explainer usually says the PEO handles payroll, taxes, benefits, and HR support. That's true, but incomplete. Discerning buyers need to know where liability shifts, where control stays put, and where costs can rise after year one.

The practical question isn't “What services are included?” It's “What business problem is being solved, and what new constraints come with the solution?” That's the difference between a useful PEO relationship and an expensive one.

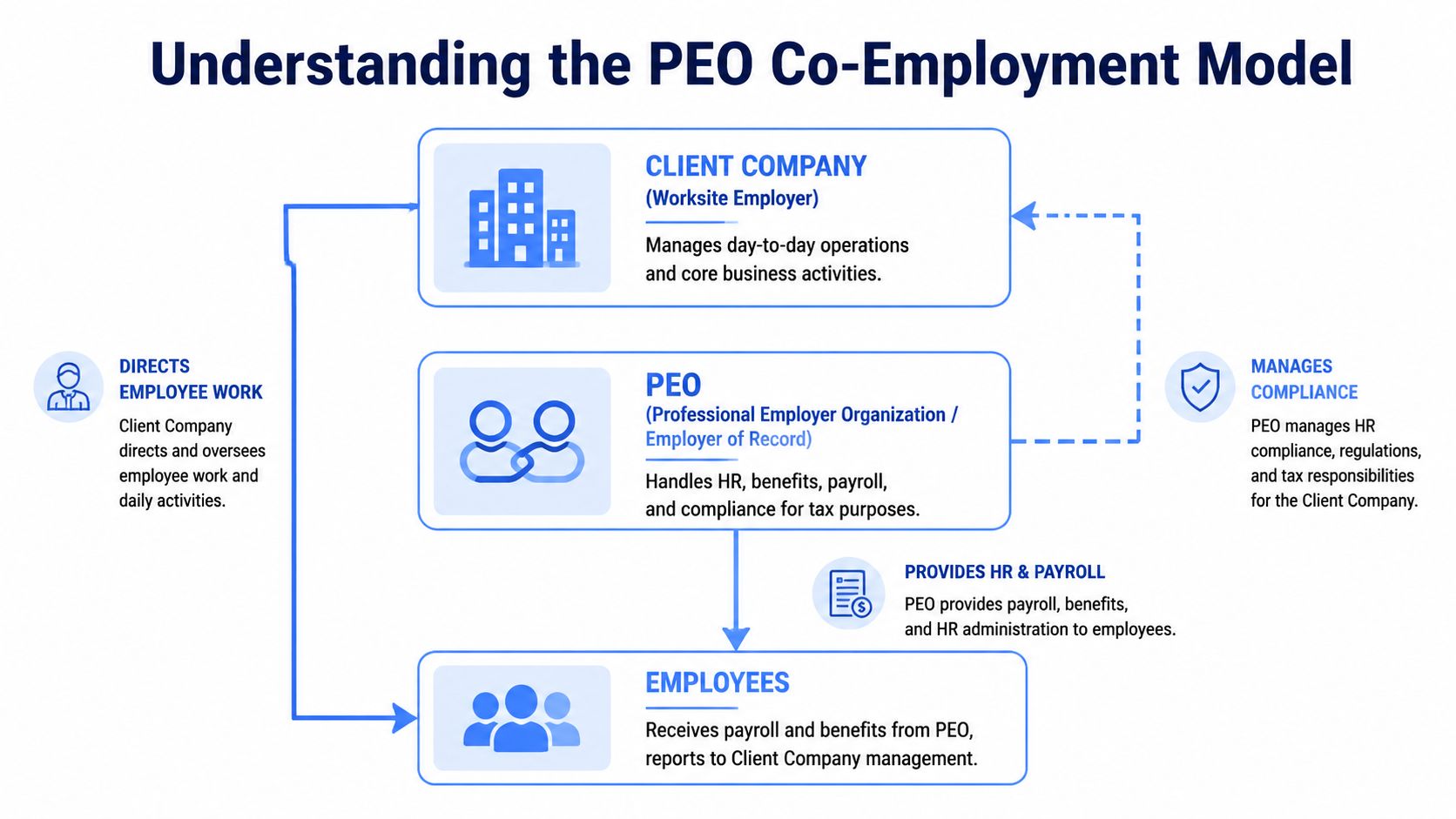

How PEO Payroll Works The Co-Employment Model

The core of what is PEO payroll is the co-employment model. In plain terms, two parties share employer responsibilities, but they do not share them equally or vaguely. Each side has a defined role.

A helpful way to think about it is this: the client company runs the business, and the PEO runs much of the employment infrastructure behind it. Employees still work for the client's managers. The PEO doesn't tell a sales rep which accounts to pursue or a plant supervisor how to schedule a shift. It handles the payroll, tax, benefits, and compliance machinery that sits underneath employment.

For a deeper legal and operational explanation, this guide to PEO co-employment is worth reviewing alongside any provider proposal.

What changes operationally

The client company still controls:

- Hiring and firing decisions: The business chooses who joins and who leaves.

- Compensation strategy: Pay rates, bonuses, commissions, and promotions remain with company leadership.

- Daily supervision: Managers direct work, set expectations, and handle performance.

- Business operations: Culture, staffing plans, and departmental decisions stay internal.

The PEO typically handles:

- Payroll processing: It calculates wages, deductions, and withholdings.

- Payroll tax filing: It files and remits taxes under the PEO structure used in the co-employment arrangement.

- Benefits administration: Enrollment, deductions, and plan administration sit with the PEO platform.

- Compliance support: The PEO supports employment-related compliance administration tied to payroll and HR processes.

That split matters because it lets a smaller employer use infrastructure that would otherwise require a larger in-house team.

Why the tax structure matters

Under the co-employment model, the PEO processes payroll and files taxes under its own EIN. According to ADP's explanation of PEO tax reporting, IRS data shows certified PEOs achieve 99.9% accuracy in federal tax compliance compared to 92% for non-PEO employers. That same source notes this structure can help shield clients from multi-state nexus complexity, where non-compliance fines average $15,000 per incident.

The model offers benefits beyond mere convenience. The tax filing mechanism can reduce error exposure, especially for companies hiring across multiple states or dealing with frequent payroll changes.

Practical rule: If the business operates in several states, ask exactly who files what, under which EIN, and who carries the remediation burden when an agency issue appears.

A strong buyer also asks what happens when a payroll input error starts with the client. Some PEOs take broad responsibility for processing accuracy but narrow responsibility for bad source data. That distinction should be clear before signing.

PEO Payroll vs ASO and In-House Payroll

The wrong comparison is PEO versus payroll software. The right comparison is PEO versus ASO versus in-house payroll operations. Those are the three models most midsize employers are choosing between.

Where the models actually differ

The biggest dividing line is liability structure. A PEO uses co-employment. An ASO delivers administrative support without changing the employer structure in the same way. In-house payroll keeps everything under the employer's own internal stack and internal accountability.

| Feature | PEO (Co-Employment) | ASO (Administrative Services) | In-House Payroll |

|---|---|---|---|

| Employment structure | Co-employment model | Administrative support model | Employer handles all functions directly |

| Tax filing approach | PEO structure handles payroll tax administration | Employer remains responsible through its own structure | Employer files and manages internally |

| Benefits access | Often bundled with broader HR and benefits administration | Usually more limited and employer-directed | Employer sources and administers directly |

| Compliance support | Broader support tied to payroll and HR administration | Support without the same liability structure | Entirely internal or spread across advisors |

| Operational control | Client retains day-to-day control | Client retains day-to-day control | Full internal control |

| Admin burden on internal team | Lower | Moderate | Highest |

| Best fit | Employers needing infrastructure and risk support | Employers wanting admin help without co-employment | Employers with strong HR, payroll, and compliance depth |

A company that wants a broader payroll and HR operating model may prefer a PEO. A company with a mature HR team but limited admin capacity may prefer an ASO. A company with specialized internal capabilities may keep payroll in-house.

For readers comparing process options beyond the PEO decision, this guide to streamlining business payroll gives a useful operational view of where outsourcing can reduce workload and where it can create handoff issues.

Which model fits which company

A practical shorthand works well here.

Choose a PEO when the business wants shared infrastructure, stronger administrative support, and a tighter compliance wrapper around payroll and HR.

Choose an ASO when leadership wants help with administration but isn't ready for a co-employment arrangement. More detail on that distinction is in this comparison of PEO vs. ASO.

Choose in-house when the company already has the payroll, HR, legal, and benefits depth to manage complexity directly, and when leadership prefers total internal control over standardized outside processes.

The best model is rarely the one with the lowest visible fee. It's the one that matches the company's operating complexity and tolerance for internal administrative burden.

The Strategic Benefits and Hidden Risks

The surface-level benefits of PEO payroll are easy to list. Less admin. Better infrastructure. Broader HR support. Those are real, but they're not the strategic reason many companies sign.

The deeper reason is advantage. A PEO can give a growing employer a more mature operating backbone than it has built internally. That can matter when the company is entering new states, tightening controls, formalizing HR, or trying to offer benefits that feel more competitive than its standalone size would normally allow.

Where the upside is real

The first strategic benefit is risk containment. When payroll, benefits administration, and employment compliance are fragmented across a broker, payroll platform, spreadsheet process, and a lean HR team, errors tend to show up in the seams. A PEO can centralize those responsibilities.

The second is execution speed. Companies that are scaling often need process consistency more than they need theoretical flexibility. A PEO can impose standard workflows for onboarding, payroll runs, benefits deductions, and reporting.

The third is talent competitiveness. Access to a broader benefits structure can change recruiting conversations, especially for a company that's large enough to feel complexity but not large enough to negotiate like a national employer on its own.

A related discipline that gets overlooked is recordkeeping. When payroll, approvals, and compliance questions are spread across systems, disputes get harder to reconstruct. Teams that want cleaner documentation should understand the basics of an audit trail in finance and compliance workflows, because that principle applies directly to payroll approvals, corrections, and employee record history.

Where buyers get burned

Contract language is where many PEO relationships go sideways. According to BambooHR's overview of PEOs, agreements often include auto-renewal clauses with 30 to 90 day notice periods and early termination penalties up to 25% of annual fees. That same source notes a 2025 NAPEO survey found 62% of PEO users reported dissatisfaction with their exit terms.

That should change how buyers read the contract. The risk isn't only overpaying on the monthly fee. The risk is getting locked into a service model that no longer fits and then paying to leave it.

Common failure points include:

- Service mismatch: The buyer expects strategic support but gets a ticket-based service desk.

- Escalating cost: The proposal looks manageable, then fees and bundled costs rise in renewal.

- Difficult offboarding: Data transfer, timing, payroll cutover, and notice terms become a project of their own.

- Cultural friction: Employees feel like HR support has moved outside the company, even when leaders want a high-touch internal culture.

A good PEO can lower administrative strain. A poorly matched PEO can replace internal complexity with vendor complexity.

Decoding PEO Pricing and Total Cost of Ownership

Cheap PEO pricing often turns out to be expensive finance. The proposal may show one admin fee, but the budget impact sits across payroll taxes, benefits, workers' compensation, implementation, and contract structure.

The two pricing models

According to Business.com's breakdown of PEO payroll pricing, PEOs commonly use two fee structures:

- Percentage of gross payroll: Typically 2% to 12%

- Per employee per month: Typically $50 to $150 PEPM

The same source gives a practical benchmark for a 100-employee company with $5 million in payroll. At 3% to 5%, annual fees can reach $150,000 to $250,000 under the percentage model.

That difference matters in forecasting. A percentage model rises with merit increases, commission growth, overtime, and bonus cycles. A PEPM model usually gives cleaner budgeting, but it can become less favorable if headcount grows faster than payroll or if the provider adds separate charges outside the monthly rate.

I tell finance teams to model both pricing methods under their actual operating plan, not under a flat-headcount assumption. A company planning 8% wage growth will feel percentage pricing differently than a company holding wages steady but hiring 20 more employees.

What belongs in the TCO model

A serious total cost model should capture more than the quoted fee. At minimum, it should include:

- Base administrative fees

- Implementation and onboarding costs

- Employer benefit contributions under the PEO's plans

- Workers' compensation structure and class-code assumptions

- Payroll tax administration scope

- Year-end processing and off-cycle payroll fees

- Renewal increases and minimum annual commitments

- Offboarding, data migration, and transition costs

Implementation is an easy place to miss real dollars. As noted earlier from the same Business.com source, setup fees can range from $5,000 to $20,000. On a smaller deal, that can erase much of the first-year savings story.

Here is the finance mistake I see most often. Buyers compare a PEO quote to the salary of one internal payroll or HR hire and call it done. That ignores benefits markup, workers' compensation treatment, payroll platform costs, broker fees, internal time spent on audits and employee issues, and the cost of getting out if the relationship fails.

A better approach is to build a 12-month view and a contract-term view. For example, a provider that looks cheaper in year one can cost more by year three if the admin fee scales with payroll growth, medical renewal rates come in above your current trend, and the agreement limits your exit options. A disciplined PEO total cost of ownership analysis makes those trade-offs visible before signature.

Experienced buyers also separate controllable cost from pass-through cost. If a PEO lowers admin burden but moves the company into a richer benefits package with higher employer contributions, the service may still be worth buying. It just is not a payroll savings decision. It is a workforce strategy decision.

The evaluation discipline is similar to finance outsourcing vendor selection. The lowest visible fee rarely reflects the full operating cost, governance burden, or switching risk.

If finance cannot rebuild the proposal into a monthly run rate, a renewal scenario, and an exit-cost scenario, the company is not evaluating PEO payroll. It is reacting to a sales quote.

How to Evaluate and Select the Right PEO Partner

Most companies spend more time selecting accounting software than selecting a PEO, even though a PEO can shape payroll operations, benefits administration, and HR processes for years. That's backwards.

A serious evaluation process should test fit across service design, pricing structure, contract terms, technology, and industry alignment. That last point matters more than many buyers expect. According to the U.S. Chamber of Commerce comparison of PEOs and payroll services, tech firms may pay 3% to 6%, while construction firms can average 8% to 12% because of workers' compensation risk, and generic PEOs can be 15% to 25% more expensive for specialized industries than a specialist provider.

Questions that expose fit

The right questions are usually more revealing than the demo.

- Who will service the account? Ask whether support is pooled, dedicated, or segmented by payroll, benefits, and HR.

- How does the provider handle industry-specific issues? A construction employer, healthcare group, or professional services firm won't have the same needs.

- What does implementation look like in practice? Ask for the sequence, responsibilities, and cutover ownership.

- How are issues escalated? Payroll errors matter most when time is short. The escalation path should be specific.

- What reporting is standard and what costs extra? Finance teams should know which outputs are native and which require manual work.

For teams building a broader vendor diligence process, this overview of finance outsourcing vendor selection is useful because many of the same evaluation disciplines apply: scope clarity, accountability, transition planning, and contract review.

Contract terms worth pushing on

The contract deserves the same scrutiny as the pricing sheet. Sometimes more.

A buyer should push on:

Renewal mechanics

Auto-renewal language should be visible, not buried. Notice windows should be practical for a finance and HR planning cycle.Termination language

Early exit terms, data transfer obligations, and transition support should be reviewed before signature, not after a service problem.Fee change protections

If pricing can move, the mechanism should be clear. Broad discretionary adjustments create avoidable budgeting risk.Service scope definitions

“HR support” can mean anything from template access to hands-on employee relations guidance. The contract should say which.Industry fit

A generic provider may still be the right answer, but only if the economics and service model hold up against a specialist alternative.

A structured buying process helps prevent “good enough” decisions that become expensive later. Companies that want a clearer framework can use this guide on how to choose a PEO to pressure-test providers on the issues that usually matter after launch, not just before signing.

The takeaway is simple. Don't buy a PEO because the demo is smooth or the admin fee looks competitive. Buy one only if the operating model, contract structure, and economics still make sense after they're put into a real finance and HR review.

PEO decisions are easier when someone independent can compare pricing, benefits, contract terms, service models, and industry fit side by side. PEO Metrics helps companies evaluate, compare, and negotiate PEO options with a clearer view of total cost and contract risk, so buyers can make a confident decision before they sign.