The decision often starts with a spreadsheet and ends in legal review.

A CFO sees one quote with a low monthly admin fee and another with a higher bundled charge. An HR director sees promises around compliance, benefits, payroll, and support. A business owner sees risk. The difference between PEO and ASO isn’t just who runs payroll or answers employee questions. It changes who carries liability, whose tax ID sits underneath core filings, who owns the benefits structure, and where total cost lands once insurance and internal staffing are included.

That last point is where many evaluations go wrong. A low ASO fee can look cheaper until the company prices benefits, workers’ compensation, broker involvement, and the internal time needed to hold the whole model together. A higher PEO fee can look expensive until pooled health and workers’ comp pricing changes the math. For companies deciding under pressure, especially those with 10 to 2,000 employees, the core issue isn’t feature lists. It’s operating model.

Table of Contents

- PEO vs ASO The Strategic Choice Beyond Admin Support

- The Foundational Difference Co-Employment vs A La Carte Services

- Comparing PEO and ASO Service Delivery Models

- A Practical Guide to PEO and ASO Pricing and Total Cost

- Analyzing Risk Management and Employer Liability

- Best-Fit Scenarios When to Choose Each Model

- Your Decision and Transition Framework

PEO vs ASO The Strategic Choice Beyond Admin Support

A PEO or ASO selection shouldn’t sit only with payroll or procurement. It belongs in a conversation between finance, HR, operations, and legal.

A Professional Employer Organization changes the structure of employment administration and shares part of the employer burden. An Administrative Services Organization provides support services while the company keeps the full employer role. That difference affects tax handling, benefits purchasing power, workers’ compensation structure, internal HR headcount needs, and legal exposure.

For finance teams, the question is advantage. Does the company gain enough from pooled benefits, bundled administration, and shared responsibility to justify the model? For HR leaders, the question is bandwidth. Does the team need a co-employment partner that can absorb more process and compliance work, or does it only need execution support while keeping control in-house?

Too many buying processes reduce this to “PEO is full service, ASO is flexible.” That’s directionally true, but it misses the stakes. Ultimately, the choice is whether the business wants a partner inside the employment infrastructure or a vendor sitting alongside it. That single decision shapes the rest of the operating model, especially when leadership is comparing a PEO against a broker, payroll provider, or broader HR services provider.

Practical rule: If leadership is only comparing admin fees, the evaluation is incomplete. Liability, benefits structure, and internal staffing costs belong in the same model.

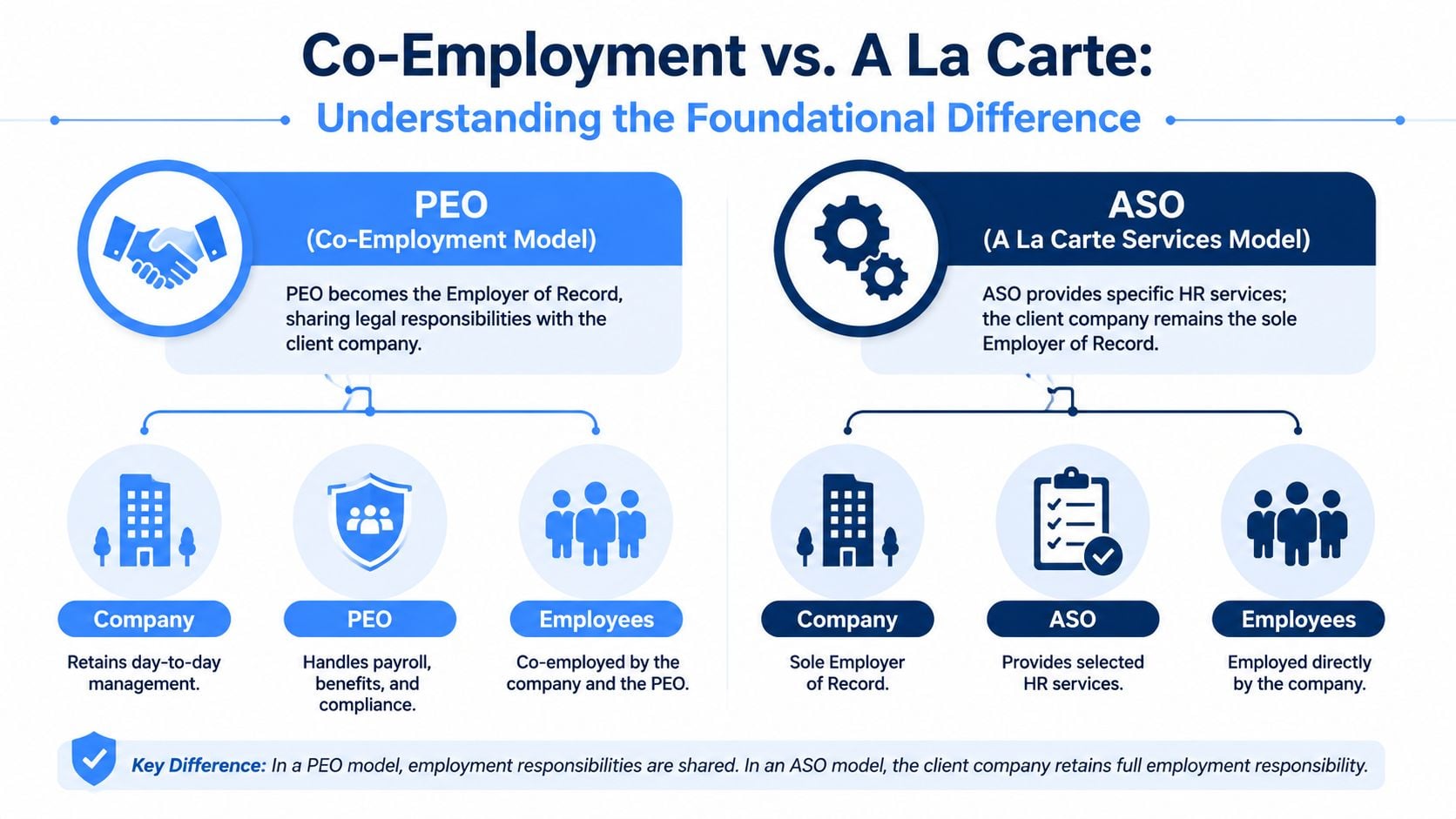

The Foundational Difference Co-Employment vs A La Carte Services

The core distinction is structural, not cosmetic.

According to FrankCrum’s explanation of PEO and ASO differences, the fundamental difference between a Professional Employer Organization (PEO) and an Administrative Services Organization (ASO) is the employment model: a PEO operates under a co-employment structure where it becomes the employer of record for tax and benefits purposes, while an ASO functions strictly as a third-party vendor without sharing employer liability.

Who holds the employer role

In a PEO arrangement, the PEO files payroll taxes under its own FEIN, sponsors a master health plan, holds the workers’ compensation policy, and assumes part of the legal liability tied to HR matters alongside the client company. The company still manages day-to-day work, performance, hiring decisions, and culture, but the employment infrastructure changes.

In an ASO arrangement, the company remains the sole employer of record. Payroll doesn’t run under the ASO’s FEIN. Benefits stay under the company’s own plan structure. Workers’ compensation remains the company’s policy. The ASO helps administer selected functions, but it doesn’t step into shared employer status.

That distinction matters even more in organizations with mixed labor models. Companies juggling contractors, seasonal labor, staffing partners, and direct employees often need a broader labor strategy before locking in an HR outsourcing structure. A useful reference point is this contingent workforce strategic framework, especially for teams deciding where co-employment should and shouldn’t exist.

A simple way to think about it

A PEO is like moving into a managed building where the operator controls the core systems. The company still runs its own office, but the building owner controls utilities, infrastructure, and building-wide policies.

An ASO is closer to hiring a facilities contractor for selected services. The company keeps the lease, the liability, and the vendor relationships. The contractor helps, but ownership doesn’t move.

That is why contract language matters so much. Under co-employment, the parties share certain responsibilities. Under an ASO, responsibility may be supported, but it isn’t transferred. For teams that need a detailed breakdown of this legal structure, a strong primer is PEO co-employment explained.

A company that misunderstands employer-of-record status usually misprices the deal, misreads the liability, or both.

Comparing PEO and ASO Service Delivery Models

Once the structure is clear, service delivery becomes easier to evaluate. The same labels, payroll, benefits admin, compliance support, can describe two very different operating realities.

A PEO typically delivers these services through its own employment and insurance framework. An ASO delivers them as administrative support around the company’s framework. That’s why two proposals can list similar services while placing responsibility in different places.

PEO vs. ASO Responsibility Matrix

| Function | PEO Model (Co-Employer) | ASO Model (Service Vendor) |

|---|---|---|

| Payroll tax filing | PEO files under its own FEIN as part of the co-employment model | Company remains responsible and payroll doesn’t run under the ASO’s FEIN |

| Employee benefits | PEO sponsors the master health plan and manages plan administration | Company owns the plan and the ASO helps administer what the company secures |

| Workers’ compensation | PEO holds the workers’ compensation policy | Company secures and retains responsibility for its own policy |

| HR compliance support | PEO provides compliance support within a shared-responsibility framework | ASO provides support, but employer responsibility stays with the company |

| Vendor and carrier management | PEO usually handles carrier relationships tied to its bundled model | Company, often with its broker or internal team, manages carrier relationships |

| Employee HR inquiries | PEO support team often handles benefits and payroll questions directly | ASO may assist administratively, but the employer remains the accountable party |

A company evaluating broader outsourcing structures can compare this model against other options in human resources outsourcing, especially when the debate includes payroll providers, brokers, and in-house expansion.

Where day-to-day friction shows up

The operational difference becomes obvious during renewals, claims, and compliance issues.

Under a PEO, the benefits renewal conversation usually runs through the PEO’s plan structure. Employees often contact the PEO’s service team for benefits and payroll support. Workers’ compensation administration sits within the PEO’s policy framework. This reduces the number of moving parts a small HR team needs to coordinate.

Under an ASO, the company still owns more decision points and more follow-up. The broker may negotiate benefits. Internal HR may handle carrier escalations. Finance may still track workers’ compensation audits and insurer communication. The ASO can make those processes easier, but it doesn’t remove the ownership burden.

For companies with experienced HR operations staff, that can be exactly the right design. For lean teams, it often creates hidden administrative load.

Operational checkpoint: Ask who owns the problem when an employee has a payroll tax issue, a benefits eligibility dispute, or a workers’ comp claim. The answer reveals more than the service list does.

A Practical Guide to PEO and ASO Pricing and Total Cost

Here, many comparisons fail.

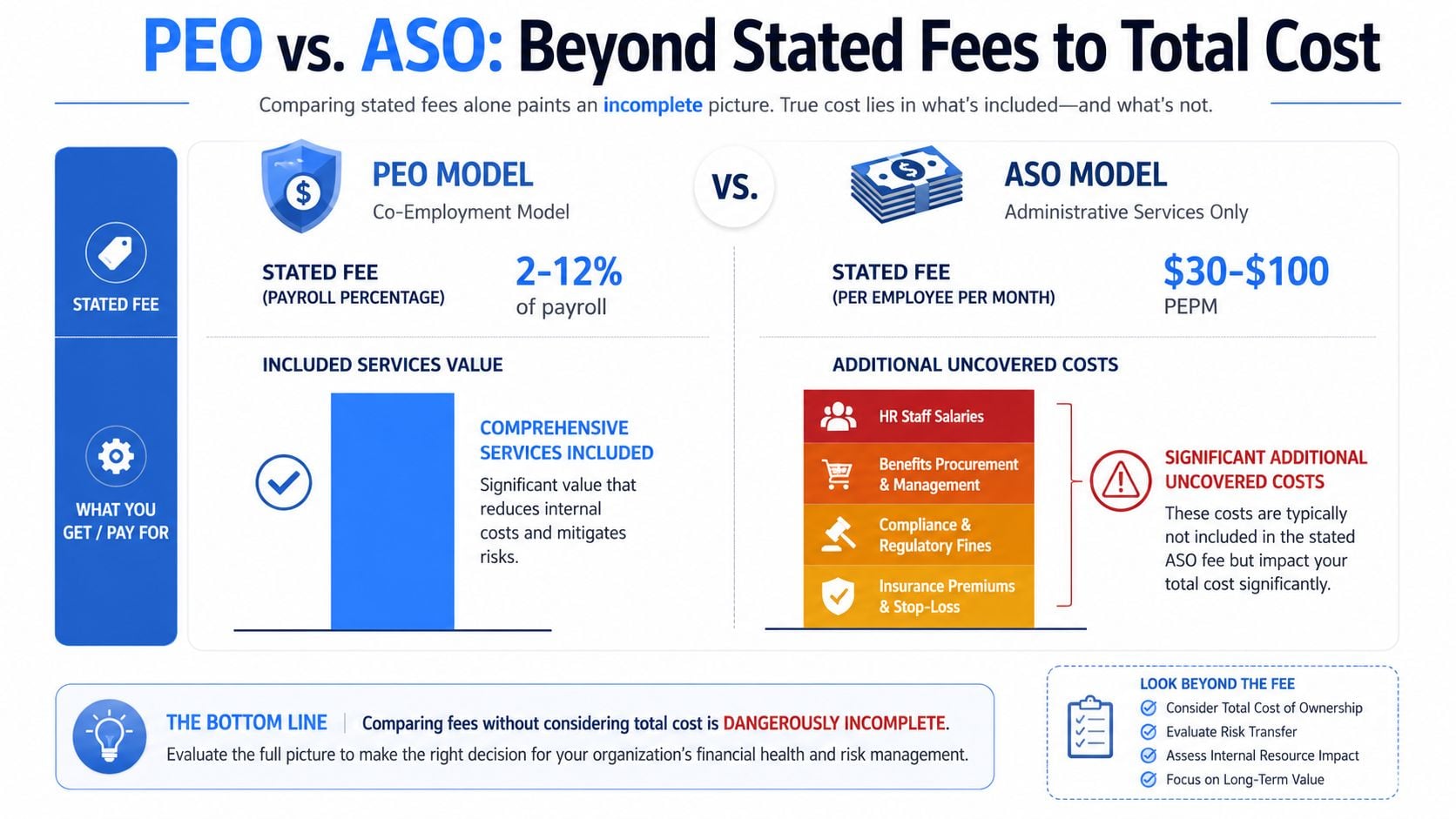

A company sees an ASO quote with a lower monthly fee and assumes it has found the cheaper option. That conclusion is often premature because the ASO fee covers administration, not the full employment cost stack. The company still buys benefits separately, manages workers’ compensation separately, and often carries more internal HR cost.

Headline fees are only the first line item

According to G&A Partners’ breakdown of ASO vs. PEO pricing, PEOs typically charge 2–12% of total payroll or a flat per-employee-per-month fee bundling benefits, workers’ comp, payroll, and compliance, while ASOs charge $30–$100 PEPM separately from benefits and workers’ comp fees. The same source notes that PEOs often deliver lower aggregate costs for employers under 200 employees due to pooled benefits advantage, whereas ASOs become more cost-effective for employers above 500 employees who can secure competitive benefits independently.

That range matters, but it still isn’t enough on its own. The proper analysis has to compare total cost of ownership, not only service fees.

A second benchmark supports the same pattern. The U.S. Chamber comparison of PEOs and ASOs notes that PEOs typically charge between 3% and 12% of total payroll or a PEPM fee, while for employers with fewer than 200 employees, PEOs often produce a lower total cost because pooled-plan pricing for health benefits and workers’ compensation usually beats what a small employer can secure alone. It also notes that for employers with more than 500 employees, ASOs typically win on total cost because larger companies can negotiate better standalone insurance rates and don’t need the pooled benefits advantage.

Where the crossover point usually appears

The crossover point sits where pooled buying power stops outweighing the bundled fee.

For a smaller employer, the PEO can be cheaper overall even when its admin charge looks higher on paper. That’s because the business may gain access to master health plan pricing and workers’ compensation economics that it can’t reproduce on its own. This is especially relevant in the sub-200-employee range.

For a larger employer, the equation often flips. Once the company has enough scale, its own broker relationships, benefits strategy, and internal HR team can make an ASO more efficient. At that point, paying for co-employment and bundled infrastructure may add cost without enough corresponding advantage.

The nuance is important. A headline comparison that says “ASO is cheaper” is often incomplete for smaller employers. The Tabulera discussion of the ASO vs. PEO crossover point highlights this directly, noting that many comparisons miss the total cost of ownership crossover point for SMBs under 200 employees, where PEO pooled plans often outperform ASO separately bought plans despite higher headline fees.

How finance teams should model it

A sound evaluation needs a side-by-side model with at least these inputs:

- PEO service structure: Is pricing based on payroll percentage or a PEPM fee, and what exactly is bundled?

- ASO fee scope: Which services are included, and which remain outside the contract?

- Benefits cost ownership: Under the ASO model, what will the company pay for medical, dental, vision, and ancillary coverage outside the admin fee?

- Workers’ compensation structure: Who holds the policy, who manages claims, and how will audit exposure be handled?

- Internal staffing cost: Which tasks still require HR, payroll, finance, broker, or legal time under each model?

A useful real-world benchmark from the same G&A source is a 60-person professional services firm. That example notes the firm typically achieves a lower total cost through a PEO bundle, while the economics change somewhere in the 200 to 500 employee range as in-house capability improves. That doesn’t mean every company will land in the same place. It means the company should test where its own break point sits rather than assume the admin fee tells the story.

For teams pricing a switch, this kind of exercise belongs next to a broader HR outsourcing cost analysis, not inside a narrow vendor quote review.

Finance view: The wrong comparison is PEO fee versus ASO fee. The right comparison is total employment administration cost under each model, including benefits, workers’ comp, internal labor, and risk transfer.

Analyzing Risk Management and Employer Liability

Cost gets attention first. Liability usually becomes the deciding factor later.

The structure of a PEO means the PEO assumes some liability and shares employment-related responsibilities. The structure of an ASO doesn’t. The U.S. Chamber’s review of PEO and ASO trade-offs states that PEOs assume some liability and share employment-related responsibilities, while ASOs do not assume liability for HR matters depending on the service agreement terms, making PEOs more expensive but offering broader risk-sharing and HR support that reduces the need for internal HR staff.

What risk sharing actually means

In a PEO relationship, shared responsibility usually shows up in payroll tax administration, benefits plan sponsorship, workers’ compensation coverage, and HR compliance support tied to the co-employment structure. That doesn’t eliminate employer risk. The company still controls hiring, supervision, employee conduct, and day-to-day workplace decisions.

In an ASO model, the company keeps the exposure. If a compliance process fails, if a filing issue arises, or if a policy decision creates legal trouble, the ASO may advise or support, but it doesn’t become a co-liable party in the same way. The vendor relationship is narrower by design.

What goes wrong in weak evaluations

Three mistakes show up repeatedly.

- Misreading shared liability as full protection: A PEO isn’t a shield against every employment claim. The company still owns major management decisions.

- Ignoring workers’ compensation structure: Who holds the policy affects claims handling, audits, and administrative burden.

- Skipping contract-level review: Service agreements decide where advice ends and responsibility begins. The label “ASO” or “PEO” isn’t enough.

Shared liability has value, but only when leadership understands exactly what is shared and what remains with the employer.

For HR and finance leaders, the practical question is simple. Does the company want to keep full employer responsibility and build the internal processes to support it, or does it want a partner with more skin in the game?

Best-Fit Scenarios When to Choose Each Model

The best answer depends less on ideology and more on company profile.

A startup with a lean team has different needs than a multi-state employer with an established HR department. A manufacturer with heavier workers’ compensation exposure is solving a different problem than a software company with mature benefits buying power. Such differences make the difference between PEO and ASO operational rather than theoretical.

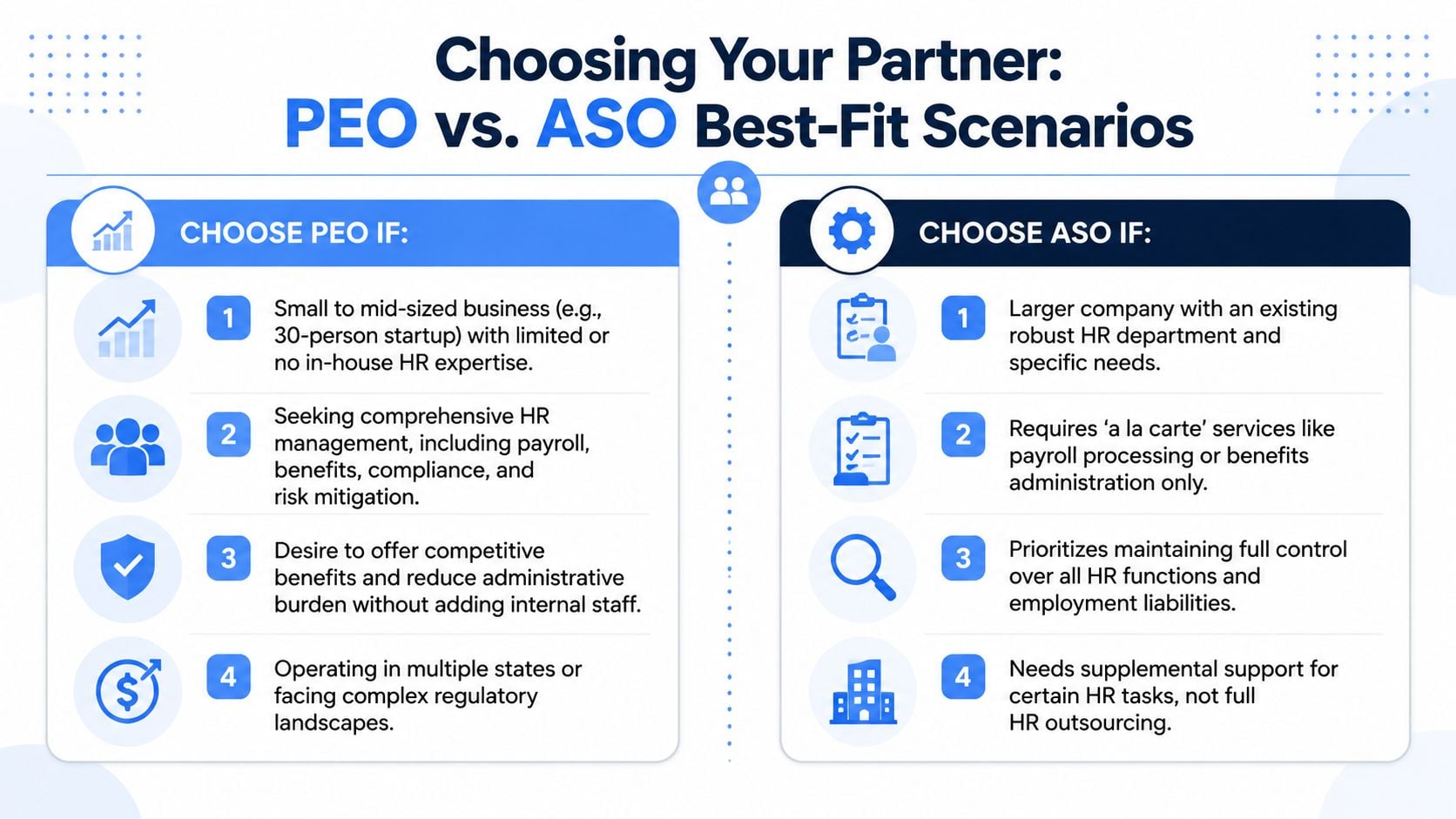

When a PEO usually fits better

A PEO is often the better fit when the business needs infrastructure, not just support.

- Smaller employer with limited HR capacity: A company under 200 employees is often where the bundled model has the strongest financial argument because pooled plans can outperform separately purchased coverage for smaller groups, as noted in Tabulera’s review of the sub-200 crossover point.

- Multi-state growth with lean administration: A growing employer that doesn’t want to build a larger internal HR and compliance function may get more value from the PEO structure.

- Benefits competitiveness matters: When recruiting depends on offering stronger benefits than the company can source on its own, pooled access can change the conversation quickly.

A practical example is a 30-person startup with no dedicated HR leader. That company usually needs payroll, benefits, compliance support, onboarding process, handbook support, and workers’ compensation administration in one package. Managing all of that through separate vendors creates more coordination cost than many founders expect.

A 250-employee manufacturer can also lean PEO if internal bandwidth is thin and risk management needs are rising. The model isn’t only for very small employers.

When an ASO usually fits better

An ASO tends to fit companies that already have the core structure and want help running it.

- Larger workforce with purchasing power: Employers above 500 employees often have enough scale to negotiate their own competitive insurance arrangements.

- Established HR and finance teams: If the business already has strong process owners, an ASO can support execution without changing employer structure.

- Need for direct control: Some companies want to remain the sole employer of record for policy, legal, or operational reasons.

A 700-employee tech company with an experienced HR team, broker relationships, and a stable benefits strategy is a classic ASO candidate. The company may want payroll administration, HRIS support, and selected compliance help, but it may not need a co-employment model.

Decision shortcut: If the company is buying capability, a PEO often fits. If it’s buying capacity, an ASO often fits.

Your Decision and Transition Framework

A strong decision process starts with internal data, not vendor demos.

Leadership should gather current benefits costs, workers’ compensation structure, payroll process ownership, HR staffing load, open compliance issues, and any upcoming renewal or implementation deadlines. Then it should ask each provider the same set of questions so the comparison stays apples to apples.

Questions that belong in every review

- Fee definition: What is included in the quoted fee, and what sits outside it?

- Liability language: Which employment-related responsibilities are shared, and which remain fully with the company?

- Benefits and policy ownership: Who sponsors the plan, who holds the workers’ compensation policy, and what changes on exit?

- Implementation timing: What is the data migration process, who owns cleanup, and how long should payroll, benefits, and employee records transition take?

- Exit terms: What notice is required, what happens at renewal, and what obligations survive termination?

A transition review should also include payroll history, census accuracy, benefits enrollment files, state registrations, and employee communications. Teams handling a provider change often underestimate the operational work involved, which is why data migration best practices should be part of the planning process early, not after contract signature.

The actionable takeaway is straightforward. Price the full model, review the liability terms line by line, and decide whether the company needs a co-employment partner or a service vendor.

PEO decisions get expensive when buyers rely on vendor framing instead of side-by-side analysis. PEO Metrics helps companies compare PEO options, benchmark pricing and benefits, flag contract risks, and negotiate stronger terms before they sign or renew.