Most advice about a professional employer organization in Florida treats the decision like a commodity purchase. Compare a few admin fees, pick the lowest quote, and move on.

That approach fails in Florida. A cheap quote can become an expensive contract once workers' compensation structure, benefits pass-throughs, implementation charges, renewal language, and exit terms show up on the invoice. In a dense market, buyers have an advantage, but they also have more room to make the wrong comparison.

Florida deserves a CFO-level review, not a generic HR checklist. The state is a major PEO market, and that changes how employers should evaluate risk, price, and negotiating power. The right provider can simplify payroll, benefits, and compliance. The wrong one can lock a company into weak service, opaque fees, and avoidable workers' comp exposure.

Table of Contents

- Why Choosing a PEO in Florida Is Different

- The Florida Co-Employment Model Explained

- Calculating the True Cost of a Florida PEO

- PEO vs ASO vs In-House HR in Florida

- A Due Diligence Checklist for Vetting Florida PEOs

- Contract Red Flags and Negotiation Levers

- Your Action Plan for Choosing a Florida PEO

Why Choosing a PEO in Florida Is Different

Florida isn't just another state on a provider coverage map. It is one of the most concentrated PEO markets in the country. According to a NAPEO industry footprint report, Florida had 107 PEOs operating in the state, the highest count in the U.S.

That concentration changes the buying process in two ways. First, it gives employers negotiating power because multiple providers often want the same account. Second, it makes lazy evaluation dangerous because two proposals that look similar on the surface may allocate risk very differently underneath.

A Florida buyer rarely wins by asking only one question: “What's your per-employee fee?” The stronger question is, “What is the total financial and legal outcome if this agreement runs for multiple years?” That means reviewing fee mechanics, workers' comp treatment, service-team design, claims handling, benefits funding, and contract flexibility as one package.

Market density creates leverage and noise

In a thin market, employers may have to accept the standard offer. In Florida, that usually isn't the case. There are enough providers that a disciplined buyer can push for cleaner language, stronger service commitments, and better renewal protections.

But the same density creates noise. One PEO may be strong in hospitality, another in multi-location healthcare groups, another in professional services with low claims exposure. One may lean on a bundled quote that hides cost drivers. Another may break everything out clearly but appear more expensive at first glance.

Practical rule: In Florida, the cheapest-looking PEO proposal is often just the least transparent one.

This is a financial decision disguised as an HR decision

Many companies start the search because payroll is messy, benefits are expensive, or internal HR is stretched. Those are valid triggers. Still, the actual decision reaches far beyond HR administration.

A PEO agreement can affect workers' compensation economics, payroll tax handling, employee experience, benefits competitiveness, and the company's ability to exit cleanly if service deteriorates. That's why strong buyers treat PEO selection like any other vendor relationship with recurring spend and operational dependency.

For a more disciplined way to frame that exposure before provider outreach begins, use a structured state employment law risk review. It helps separate operational pain points from actual compliance and cost priorities.

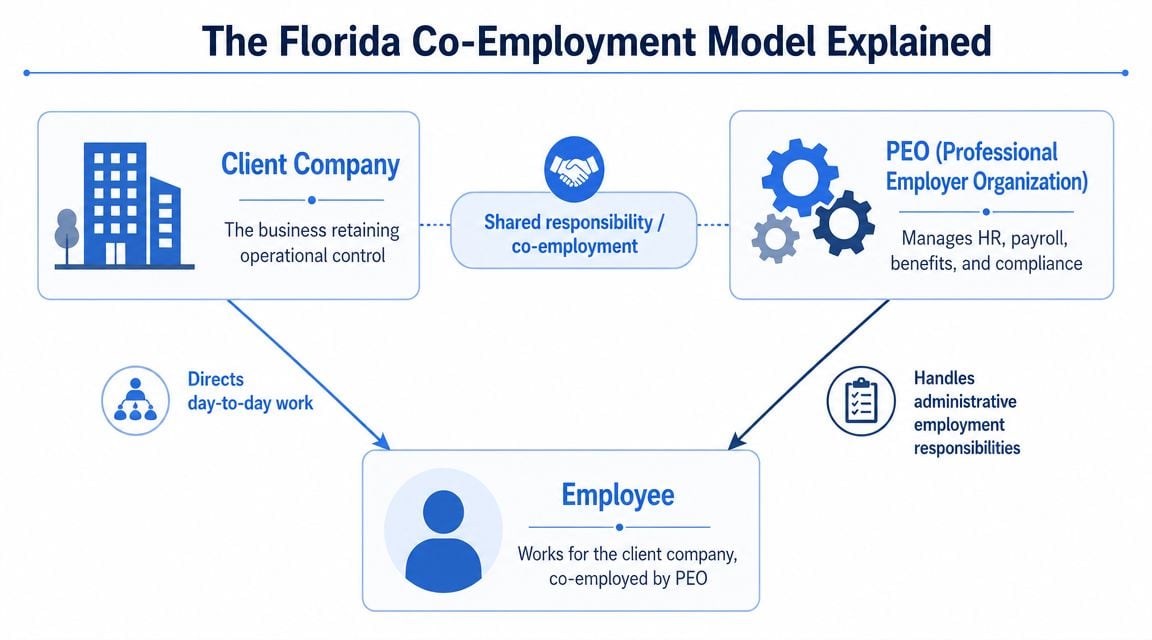

The Florida Co-Employment Model Explained

A PEO relationship in Florida works through co-employment. That term sounds more complicated than it is. The client company keeps control of the business and the workforce's day-to-day activity, while the PEO takes on defined administrative employment responsibilities.

A useful analogy is property ownership and property management. The owner still decides what happens to the asset. The manager handles the administrative work, documents, vendors, and routine processes. In a PEO model, the employer still runs operations, hires for business need, sets compensation strategy, and directs employees. The PEO handles payroll administration, benefits administration, HR support, and certain compliance functions.

The Florida oversight view matters here. The Florida Office of Program Policy Analysis and Government Accountability report described PEOs as businesses providing extensive HR services, including workers' compensation coverage, and noted that the size of Florida's PEO industry had increased.

Who controls what

The split of responsibility should be clear before contract signature. When it isn't, companies usually discover the confusion during a payroll error, a claim, or a termination dispute.

The client company typically controls:

- Daily supervision: Managers assign work, set schedules, and evaluate performance.

- Operational decisions: The business decides who to hire, promote, discipline, and terminate.

- Compensation philosophy: Pay ranges, bonus philosophy, and staffing levels remain business decisions.

- Workplace practices: Safety procedures, training enforcement, and site-level management still sit with the employer.

The PEO typically handles:

- Payroll processing: Wage calculation, deductions, and related reporting.

- Benefits administration: Enrollment support, carrier coordination, and plan administration.

- HR administration: Onboarding documents, handbook support, and routine employment documentation.

- Certain compliance functions: Tax filing support, employment administration, and workers' comp administration under the service model.

A clear primer on the structure helps when legal and finance teams need a common vocabulary. This overview of PEO co-employment explained is useful for that internal alignment.

Why workers comp matters so much in Florida

In many Florida evaluations, workers' comp is the hidden center of the entire deal. The PEO's master policy structure can change how risk is priced, how claims are administered, and how costs appear on the invoice.

That doesn't mean every employer should move workers' comp into a PEO arrangement. It means every employer should understand exactly what it is handing over. A company with poor claims history may view the PEO's arrangement as a relief valve. A company with a clean history and stable internal administration may find less advantage.

If the provider can't explain, in plain language, how workers' comp is handled from enrollment through claims management and exit, the buyer doesn't have enough information to sign.

The same applies to unemployment and payroll-related administration. Sometimes the outsourced structure is beneficial. Sometimes it's neutral. Sometimes it introduces trade-offs that sales teams understate. The practical point is simple: co-employment is not a marketing phrase. It is a real operating model with real allocation of responsibility.

Calculating the True Cost of a Florida PEO

A Florida PEO quote usually starts with a simple number. That's the trap.

The admin fee matters, but it's only one line in the full cost picture. A serious evaluation builds a total cost of ownership model that captures administrative fees, workers' compensation treatment, payroll tax handling, benefits costs, implementation expenses, service add-ons, and termination exposure. Without that model, the buyer is comparing marketing formats, not economics.

A Florida workers' compensation resource makes the point directly. It notes that PEOs may provide savings only if a company has unfavorable loss history, while also warning about additional and sometimes hidden fees, upfront charges, and claim-related costs. That's why a headline quote can't be trusted on its own.

What belongs in the cost model

A finance-ready model should include at least these categories:

- Administrative charges: The recurring PEO service fee and any separate charges for payroll runs, off-cycle payrolls, year-end processing, onboarding, background checks, or HR projects.

- Benefits costs: Employer medical, dental, vision, life, disability, and retirement-related costs, plus any required contribution rules or plan participation constraints.

- Workers' compensation: Whether pricing is embedded, passed through, estimated, adjusted later, or influenced by claims treatment under the PEO's structure.

- Taxes and filings: How payroll taxes are administered and whether any service-related tax handling fees appear separately.

- Implementation costs: Data migration, onboarding support, system setup, employee meetings, handbook work, and carrier transitions.

- Exit costs: Notice periods, runout support, COBRA coordination, data extraction, and final invoice reconciliation.

Many teams benefit from a benchmarking framework built specifically for how much a PEO costs, because provider invoices rarely use the same structure.

Where buyers get misled

A low admin fee often distracts from a more expensive total arrangement. Common examples include:

- Bundled ambiguity: The quote says “all-in HR support,” but benefits administration or claims support carries separate charges.

- Estimated workers' comp treatment: The proposal implies savings without showing how claims, classifications, audits, or adjustments affect actual cost.

- Implementation minimization: The contract leaves enough room for onboarding work to become a paid project after signature.

- Renewal drift: The initial quote looks competitive, but the contract gives the provider wide flexibility to raise pricing later.

A disciplined buyer should ask for the proposal to be rebuilt into the company's own spreadsheet format. Don't accept each provider's template as the basis for comparison.

Buyer warning: If one proposal can't be normalized line by line against another, it isn't ready for executive review.

A practical review usually works best when HR, finance, and operations each own one part of the model. HR validates service scope and benefits fit. Finance rebuilds the invoice and tests assumptions. Operations confirms how the provider will handle locations, supervisors, and employee communication.

One more point matters in Florida. Savings claims around workers' comp are often true only for the right employer profile. A company with adverse claims history, difficult classifications, or weak internal processes may gain more from the PEO arrangement than a company already buying well in the open market. That's why the right question isn't “Do PEOs save money?” It's “Under this company's profile, with this payroll mix and this risk history, does this PEO lower total cost after all fees?”

PEO vs ASO vs In-House HR in Florida

Not every Florida employer needs a PEO. Some need an ASO. Others are better off keeping payroll, HR, and compliance management in-house with specialist vendors around the edges.

The problem is that these models are often compared too loosely. Buyers hear “full-service,” “outsourced HR,” or “compliance support” and assume the offerings are close substitutes. They aren't. The biggest dividing line is whether the company wants administrative help only, or administrative help plus a meaningful degree of risk transfer and infrastructure.

The real dividing line is risk transfer

A PEO typically provides services inside a co-employment arrangement. An ASO provides outsourced administration without the same employment structure. In-house HR keeps the company in direct control of systems, vendors, and compliance workflow.

For many Florida companies, the practical question is less about preference and more about exposure. If workers' comp complexity, payroll administration burden, and multi-site HR support are the main pain points, a PEO may fit. If the company wants to keep more direct control and outsource selected tasks, an ASO may be cleaner. If leadership already has capable HR, payroll, legal, and broker relationships, in-house can remain the better option.

| Factor | Professional Employer Organization (PEO) | Administrative Services Organization (ASO) | In-House HR |

|---|---|---|---|

| Workers' comp liability and cost | Often tied to the PEO structure and administration | Employer typically retains direct responsibility | Employer retains direct responsibility |

| Access to health benefits options | Often bundled with PEO-sponsored offerings or negotiated programs | Usually coordinated without the same co-employment structure | Employer manages broker and carrier relationships directly |

| State compliance administration | Broader outsourced support for payroll and HR administration | Support is narrower and depends heavily on scope | Internal team owns workflow, timing, and controls |

| Cost structure | Bundled service model that can mask cost drivers if not unpacked | Usually more modular | Internal headcount plus vendor stack and advisory costs |

| Best fit | Employers seeking support plus operating relief | Employers wanting support without full PEO structure | Employers with stronger internal capability and control needs |

Some industries feel this distinction more sharply. Construction, hospitality, healthcare support, field services, and multi-location retail often care more about workers' comp administration and employee-volume swings than low-risk office environments do. In those settings, the structural difference between PEO and ASO matters more than the sales presentation.

A useful internal exercise is to rank priorities in this order: risk transfer, benefits strategy, administrative relief, control, and flexibility to exit. Once leadership agrees on that ranking, the right model is usually easier to spot.

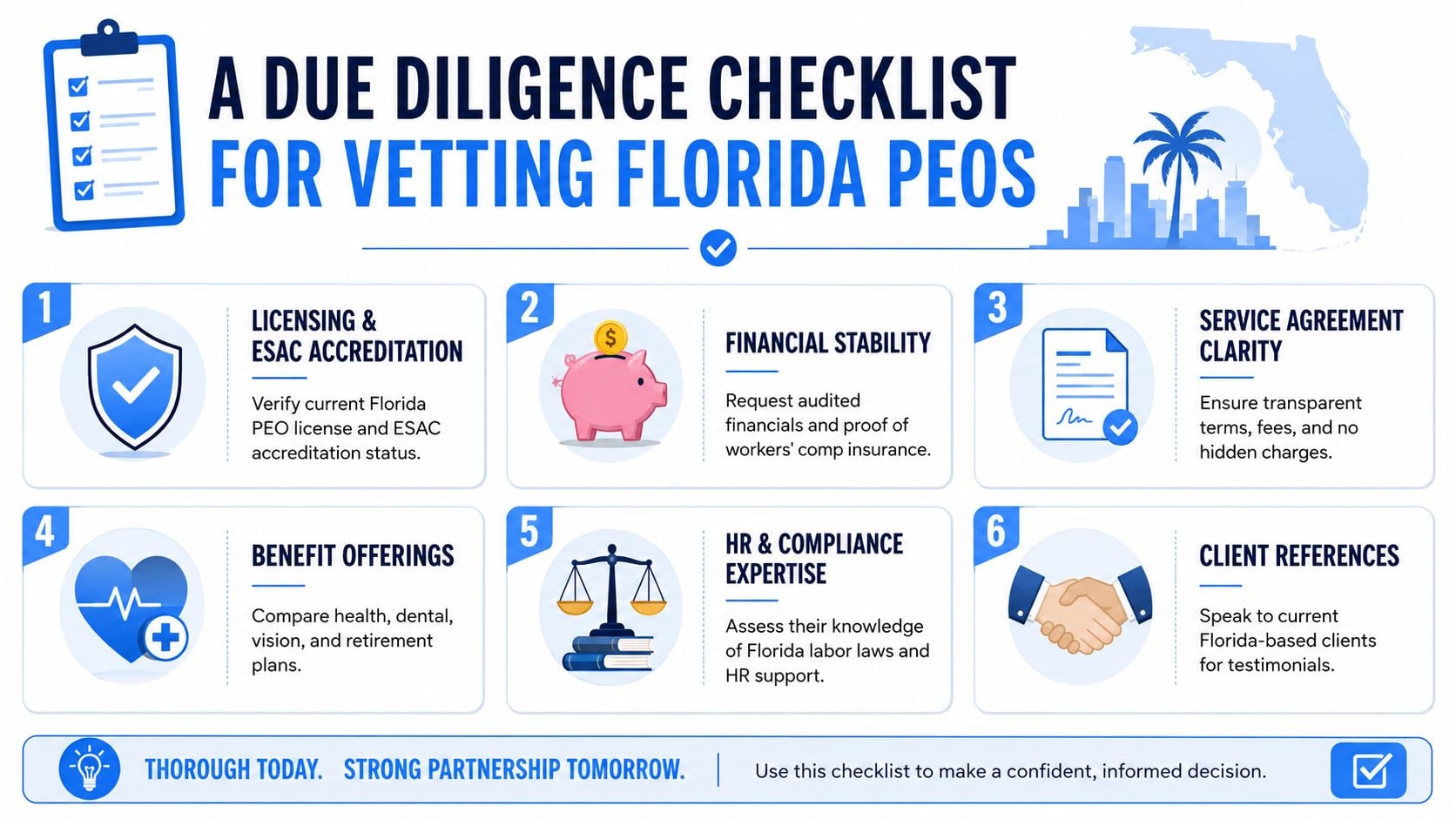

A Due Diligence Checklist for Vetting Florida PEOs

Florida's PEO market is crowded enough that “good on the demo” means almost nothing. StaffMarket's Florida directory says its database includes 120 different PEOs operating in the state, which is why buyers need a structured filter before provider meetings turn into noise. That market snapshot appears in StaffMarket's Florida PEO directory.

A shortlist should be earned, not assumed. The buyer's job is to eliminate providers that can't support the company's risk profile, service expectations, or contract requirements.

What to verify before the finalist round

A real diligence file should include more than a proposal and a demo deck. At minimum, buyers should review:

- Licensing status: Verify the PEO's Florida licensing status directly through the appropriate state records before any finalist selection.

- Financial backing: Ask for audited financials or equivalent evidence of financial stability, especially if the provider emphasizes workers' comp strength.

- Service model: Confirm whether support is centralized, pod-based, or assigned to named contacts. Then ask what happens when a payroll lead or HR contact leaves.

- Industry fit: Request client references from businesses with similar workforce patterns, not just similar headcount.

- Geographic support: Test whether the provider can support employees across Florida locations with consistent onboarding, handbook administration, and escalation handling.

- Contract exhibits: Review all fee schedules, service descriptions, workers' comp language, and termination provisions before verbal selection.

For teams that want a tighter process, this PEO due diligence checklist helps standardize provider review across finance, HR, and legal.

Questions that expose weak providers

Weak providers usually fail on specifics. Strong ones answer clearly and document the answer.

Ask questions like these:

- How are claims escalated? The provider should identify who owns first response, documentation, and follow-up.

- Who handles implementation? A sales rep's promise doesn't matter if onboarding is handed to a different team with different standards.

- What fees sit outside the proposal? Push for a written list of non-recurring, contingent, and event-based charges.

- How do you support policy and compliance issues in Florida? The answer should be concrete, and legal boundaries should be clear.

When employment practices, privacy issues, or state-specific policy questions become sensitive, outside counsel review is worth the cost. For businesses that need Florida-focused legal context around employment and compliance obligations, Coto & Waddington's legal expertise is a useful reference point during diligence.

A strong PEO doesn't resist diligence. It expects it.

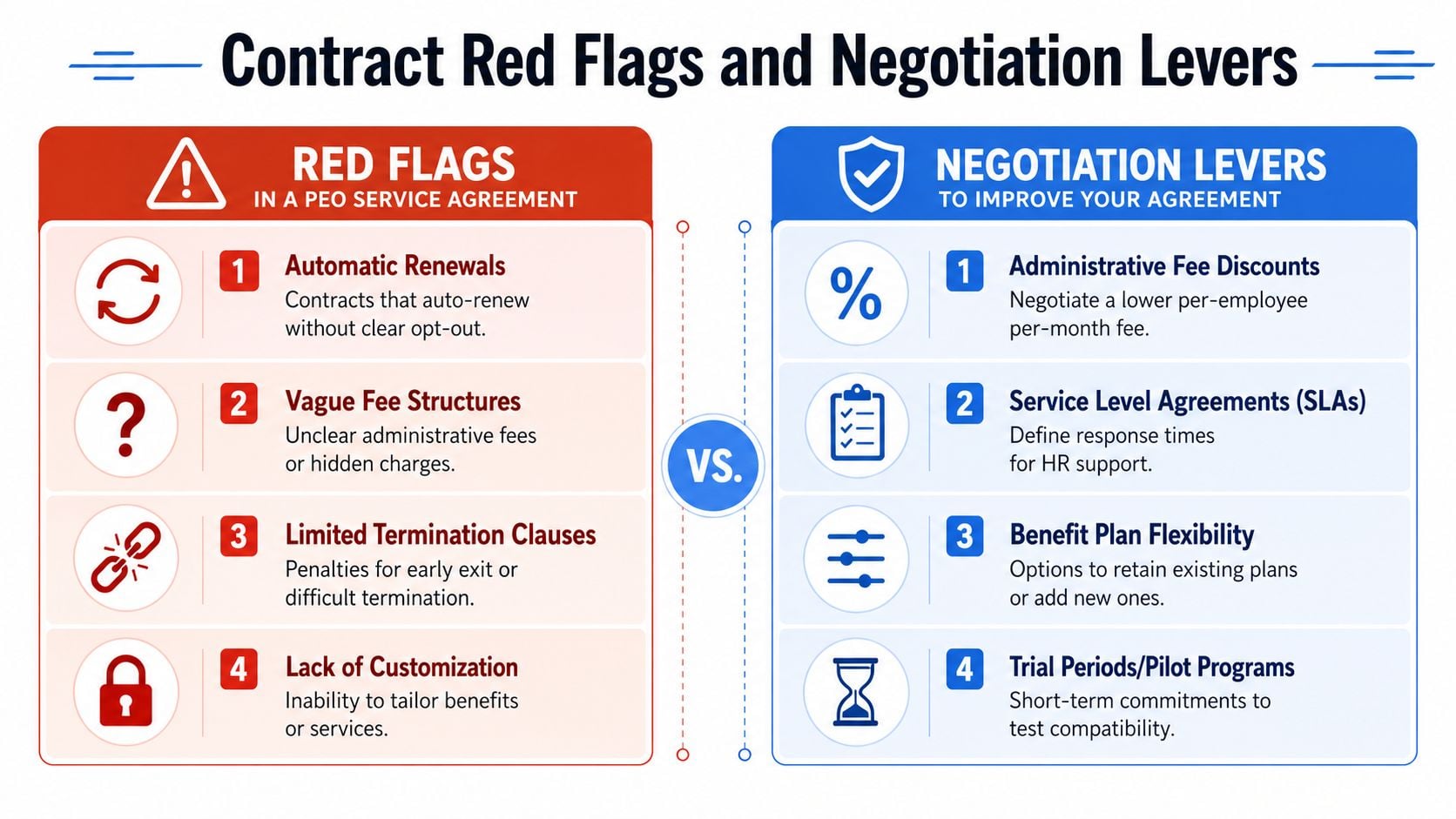

Contract Red Flags and Negotiation Levers

Most PEO agreements are written to reduce ambiguity for the provider, not for the client. That doesn't mean the contract is unfair by definition. It means buyers should assume the paper starts out provider-friendly and negotiate from there.

Many executives spend most of their time comparing proposals and too little time marking up the agreement. That reverses the actual risk. Proposal language sells the relationship. Contract language controls it.

Clauses that deserve a hard review

These issues deserve direct attention before signature:

- Automatic renewal language: If the contract renews unless terminated in a narrow notice window, the provider has a timing advantage.

- Vague fee definitions: If the agreement references schedules that can change, or uses broad wording around pass-through costs, the invoice can expand later.

- Weak termination rights: Long notice periods, penalties, or operational barriers make it hard to leave a poor-fit provider.

- Unclear liability language: If compliance support is marketed heavily but responsibility language stays broad and client-facing, expectations are misaligned.

- Soft service commitments: “Commercially reasonable efforts” isn't the same as measurable response standards.

A disciplined legal review benefits from the same habits used in broader vendor governance. These effective contract management practices are relevant because PEO agreements behave like complex operating contracts, not simple subscription terms.

Negotiation points that actually move the deal

Not everything is negotiable, but more is movable in Florida than many buyers assume. The competitive market gives employers room to push if they do it before final selection.

Strong pressure points include:

Renewal protection

Ask for clearer renewal notice rules, limits on fee increases, or a rate commitment period on the core administrative fee.Termination flexibility

Push for cleaner exit mechanics, shorter notice requirements where possible, and explicit runout support obligations.Fee transparency

Require a complete fee schedule attached to the agreement. If a charge can appear later, it should be named now.Service standards

Add response expectations for payroll issues, employee escalations, onboarding support, and claims-related questions.Implementation accountability

Name the implementation responsibilities, timeline assumptions, data ownership terms, and transition support in writing.

A practical guide to PEO contract negotiation can help buyers separate market-standard language from provider-friendly overreach.

Contracts rarely fail because of the clause everyone noticed. They fail because of the sentence nobody translated into operational reality.

One useful tactic is to negotiate from a side-by-side redline summary rather than a generic comment list. Put each requested revision into one of three buckets: pricing protection, operational clarity, and exit risk. That forces the provider to respond to business impact, not just legal wording.

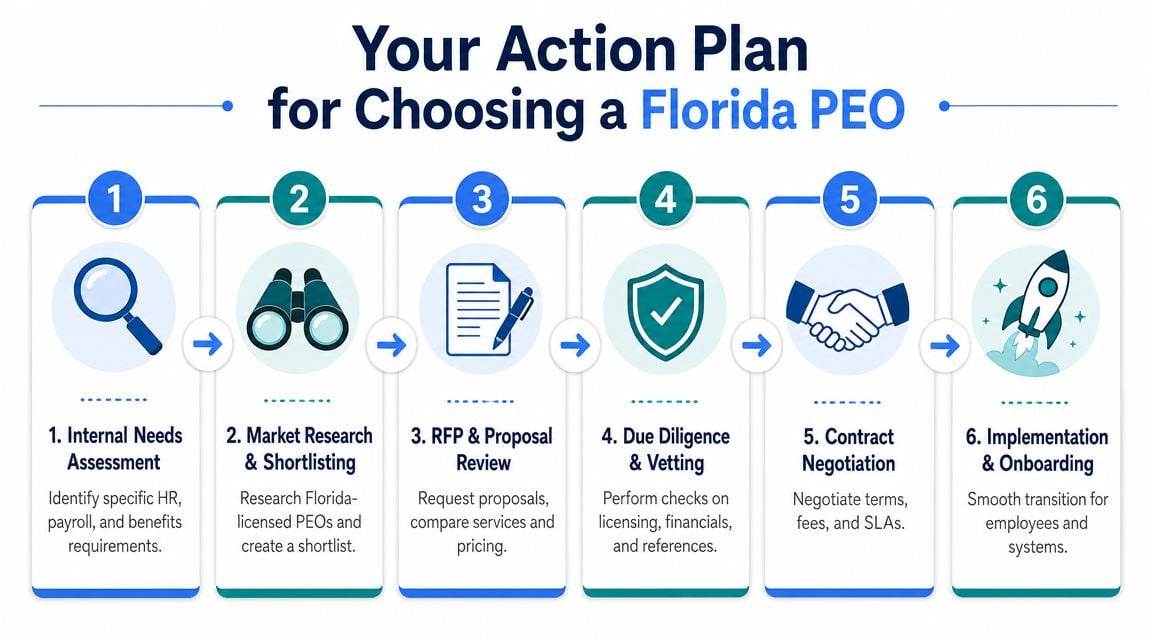

Your Action Plan for Choosing a Florida PEO

Most Florida employers don't need more information. They need a decision process that keeps sales momentum from outrunning internal analysis.

The strongest process is sequential. It starts with internal priorities, moves into cost modeling and market screening, and ends with negotiated contract terms that match the company's actual risk tolerance.

A practical sequence for finance and HR leaders

Step 1: Define the business case

List the actual reasons for evaluating a PEO. Is the trigger workers' comp pressure, weak benefits, payroll complexity, compliance strain, or lack of internal HR depth? If leadership can't rank the top priorities, every provider will sound plausible.

Step 2: Build the comparison model

Create one spreadsheet template that every provider must fit. Include admin fees, benefits costs, implementation items, non-recurring charges, and contract-driven risks. If the quote doesn't fit the template, the provider hasn't given enough clarity.

Step 3: Run a disciplined market scan

Screen Florida providers for licensing, service model, industry relevance, and multi-location fit. Don't send an RFP to everyone. Narrow the field to credible options first.

Step 4: Pressure-test benefits and insurance assumptions

If benefits are a major reason for considering a PEO, compare the PEO path against standalone options too. For employers evaluating the broader Florida small-group market alongside PEO proposals, Pounds Health small business insurance is a practical resource for understanding the separate insurance side of the decision.

Step 5: Benchmark proposals on one page

Force an apples-to-apples summary for executives. One page should show cost structure, workers' comp approach, service design, major contract risks, and notable trade-offs. If the summary is longer than that, the recommendation isn't clear enough.

Step 6: Negotiate before announcing a winner

Your negotiating advantage diminishes once the provider knows the deal is theirs. Finalist stage is the time to negotiate renewal protection, fee clarity, implementation commitments, and exit terms.

The final deliverable should be simple: a documented recommendation that explains which provider fits the company best, what risks remain, and what contract changes are required before signature.

A good professional employer organization in Florida can absolutely improve operations. But the winning decision usually comes from process discipline, not provider marketing.

PEO buyers don't need another sales pitch. They need a clean comparison of pricing, benefits, contract terms, service quality, and risk. PEO Metrics helps companies evaluate, benchmark, and negotiate PEO options with a side-by-side analysis built for finance and HR decision-makers.