A Florida employer shopping for a PEO usually sees the same pattern. A national provider promises buying power, a regional firm promises white-glove service, and both send proposals that look polished but are hard to compare line by line. The admin fee looks simple until payroll tax handling, workers' comp structure, renewal terms, and service limits start showing up in the fine print.

That problem is sharper in Florida because the market is deep, crowded, and state-specific. Florida is one of the largest PEO markets in the country, which gives buyers real negotiating power, but it also creates a higher risk of choosing a provider whose contract structure, insurance setup, or compliance process doesn't fit the company's actual operating model.

The right way to evaluate PEOs in Florida isn't to ask which firm is “best.” It's to ask which model fits the company's headcount, hiring footprint, risk profile, and tolerance for service trade-offs. That's where most buying teams need a better framework.

Table of Contents

- Evaluating PEOs in Florida Beyond the Sales Pitch

- Understanding the Florida PEO Market Landscape

- Navigating Florida-Specific Regulatory and Compliance Hurdles

- Benchmarking PEO Costs and Benefits in Florida

- Comparing PEO Providers National vs Florida-Specialist

- A Practical Checklist for Vetting Florida PEOs

- Making Your Final PEO Decision in Florida

Evaluating PEOs in Florida Beyond the Sales Pitch

Most PEO proposals sound better than they are. Sales teams lead with benefits access, payroll efficiency, and compliance support. They spend less time on what happens at renewal, how service issues get escalated, who owns tax reporting workflows, or how quickly the client can exit if the relationship goes sideways.

That matters more in Florida because buyers have a lot of choice. Existing content often stops at provider lists or generic benefit summaries, but it doesn't translate Florida's market depth into buyer strategy, including whether employers should expect stronger competition on renewal, more room to negotiate, or a better fit among national and regional models, as noted in the NAPEO Florida client concentration summary.

A finance leader should treat PEO selection like a risk-transfer decision, not a convenience purchase. The wrong provider can create friction in payroll operations, leave administration, workers' comp claims handling, onboarding, and year-end reporting. The right provider can clean up fragmented HR processes and reduce internal administrative drag. Both may look similar in the demo.

| What to compare early | Why it matters in Florida | What buyers often miss |

|---|---|---|

| Licensing and compliance process | Florida has state-specific operational rules | Sales reps may gloss over who owns what |

| Cost structure | Admin fees rarely tell the whole story | Benefit and insurance mechanics drive real cost |

| Service model | Response quality varies widely | “Dedicated support” can mean very different things |

| Insurance structure | Partial arrangements can create gaps | Carve-outs need careful review |

| Renewal and exit terms | Market depth creates negotiation leverage | Many teams accept boilerplate too quickly |

Practical rule: If two PEO proposals look close on price, the tie-breaker usually isn't the admin fee. It's contract flexibility, insurance clarity, and who will actually solve problems after implementation.

A smarter buying process starts with sharper questions. Instead of asking for a standard quote, ask each provider to show fee assumptions, implementation responsibilities, workers' comp handling, service escalation contacts, and renewal protections in writing. A good starting point is a structured PEO contract negotiation guide that forces those items into the open before legal review begins.

Understanding the Florida PEO Market Landscape

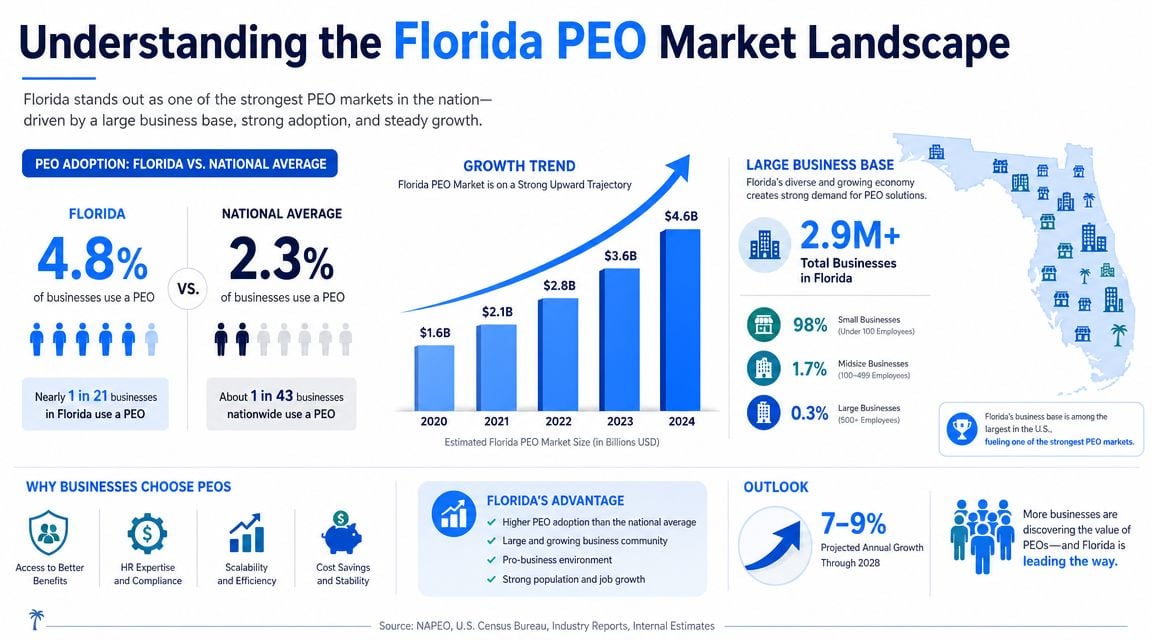

A CFO entering Florida often gets the same pitch from three different providers in the same week. The demos look polished, the admin fee spread looks narrow, and every rep claims strong local support. The key buying advantage comes from understanding how crowded this market is, why that gives buyers more negotiating room, and where Florida-specific cost differences show up.

According to the Florida Office of Program Policy Analysis and Government Accountability, the number of PEOs operating in the state rose from 677 in fiscal year 2016–17 to 760 as of March 2020, while average fiscal-year employment for covered workers rose from 537,930 in FY 2016–17 to 572,798 in FY 2018–19, and average fiscal-year wages increased from $39,636 to $42,995 during that period (Florida OPPAGA report). Florida is not a fringe PEO market. It is a large, mature provider field with enough volume to create meaningful differences in pricing discipline, service depth, and contract terms.

At the national level, NAPEO reported that at the end of 2022 there were 523 PEOs in the United States serving 4.5 million worksite employees, paying $308 billion in wages to more than 208,000 PEO clients. The same report states that PEO clients represented 17% of all businesses with 10–99 employees, worksite employees had grown at a 7.5% compounded annual rate since 2008, and Florida accounted for 25% of all PEO clients, ahead of Texas, California, and New York (NAPEO industry footprint report).

For a buyer, that market structure matters because Florida gives you more choice than many states, but also more variance. Some providers are disciplined operators with strong payroll controls and predictable implementation. Others win deals on rate and hand off the account to a thin service team after signature.

That is why the Florida decision should start with provider type, not logo recognition.

A national PEO may bring stronger HRIS tools, broader benefits buying power, and more standardized service processes. A Florida-focused firm may be better at state leave administration, workers' compensation class-code discussions, and practical issue resolution for multi-location operations inside the state. Neither model is automatically better. The better fit depends on your employee count, claims profile, hiring pace, and whether your finance team needs tighter reporting or more state-specific handholding. Teams reviewing professional employer organization options side by side usually get better results when they separate those models before pricing discussions start.

The size of the Florida provider field also changes how you should negotiate. In a crowded state market, providers often have room to adjust implementation fees, shorten initial terms, revise renewal notice windows, or add named service contacts. Sales reps rarely volunteer those concessions early. Buyers get better terms when they run a disciplined process and force competing providers to respond to the same scope, census assumptions, insurance setup, and support expectations.

One practical point gets missed often. Florida's labor profile is broad, with large service-sector populations, seasonal hiring patterns, and employers that can swing workers' compensation costs quickly based on class mix and claims experience. That means a PEO with an attractive admin fee can still be the more expensive option if its benefit structure, workers' comp arrangement, or payroll tax assumptions are less favorable for your workforce.

State employment administration also affects fit. If your team expects the PEO to support Florida leave handling in a detailed, policy-driven way, ask how that work is done and what tools employees and managers will use. For example, the Redstone HR leave platform for Florida shows the kind of state-specific leave framework buyers should expect a provider to understand, whether that support is delivered internally or through a partner.

Florida rewards disciplined buyers. The market is big enough to give you negotiating advantage, but only if you compare providers by operating model, insurance structure, service ownership, and contract terms before you compare headline price.

Navigating Florida-Specific Regulatory and Compliance Hurdles

A PEO doesn't remove employer risk in Florida. It reallocates and manages pieces of it. That's why a Florida buyer needs to understand the state rules that sit underneath the sales presentation.

Licensure and operational standing matter

In Florida, a PEO must be actively licensed under Chapter 468 and registered with the Florida Department of Business and Professional Regulation. That sounds like a background detail, but it affects whether the provider is properly positioned to operate in the state's co-employment framework.

A buyer shouldn't assume the legal setup is fine because the provider is large or well known. The safer move is to verify current licensure and ask who inside the PEO owns state compliance monitoring, payroll tax administration, and notice handling if a regulatory issue arises.

The 30-day reemployment-tax election isn't a small administrative detail

Florida's Department of Revenue requires a newly licensed PEO to make a reemployment-tax election within 30 days of licensure, and that election determines how unemployment tax reporting is assigned and managed for co-employed workers (Florida Department of Revenue reemployment-tax election guidance).

For a CFO, the practical issue is control. If the PEO handles tax reporting one way and the client assumes it works another way, the disconnect usually shows up after implementation, not before signature. The right diligence question isn't “Do you handle unemployment tax?” It's “Walk through exactly how reporting responsibility is set up in Florida, what election applies, and what documentation the client receives.”

A Florida PEO transition should include a written tax workflow, not just a verbal assurance that payroll taxes are “handled.”

Leave, wage-hour, and handoff risk

Florida employers also need clarity on related compliance workflows that often sit adjacent to the PEO relationship. Leave administration is a common weak point because the PEO may support policy administration while the employer still owns day-to-day manager decisions and documentation discipline. For teams reviewing state leave requirements and policy interactions, the Redstone HR leave platform for Florida is a useful reference point during diligence.

The same applies to wage-hour practices. A PEO can provide guidance, payroll processing, and policy templates, but the employer still controls scheduling, break practices, classification decisions, and supervisor behavior. That's where companies should map the overlap between internal management and external support before the agreement is signed. A focused wage and hour compliance review helps define which responsibilities stay with the employer and which ones are contractually supported by the PEO.

Workers' comp structure can create hidden exposure

Florida buyers should ask direct questions about how workers' compensation is arranged, especially if the provider proposes any carve-out, split, or partial approach. If one workforce segment sits inside the PEO structure and another sits outside it, the company needs to understand exactly how coverage continuity is maintained across the whole employee base.

That issue becomes especially important in industries with rotating crews, multiple locations, or variable classifications. Construction, field services, hospitality, and healthcare operations should press for written clarity on employee mapping, reporting rules, and claims escalation.

Benchmarking PEO Costs and Benefits in Florida

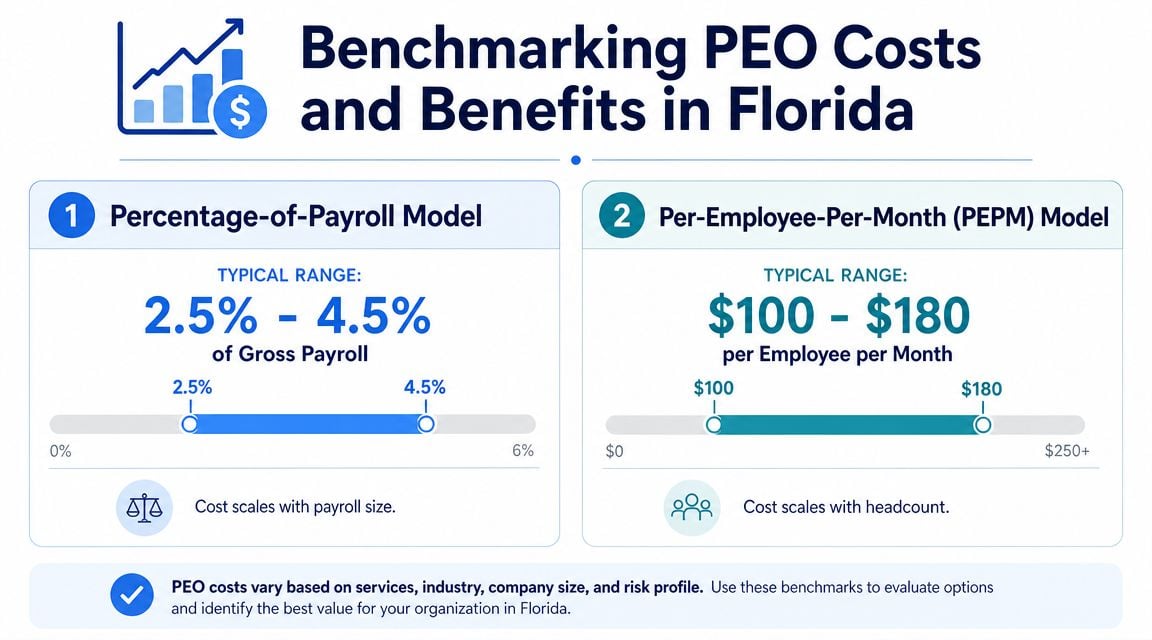

Most Florida PEO proposals are framed to make the admin fee look like the main decision variable. It rarely is. A lower fee can still produce a worse total outcome if the health plan is weak, the workers' comp structure is clunky, or the renewal language shifts too much cost back to the client.

The first benchmark should separate pricing model from total cost. Florida buyers generally see two broad charging methods:

- Percentage of payroll. The fee rises with payroll, which can be simple but may become expensive for higher-paid workforces.

- Per employee per month. The fee is easier to forecast, but buyers still need to check what services are excluded or billed separately.

The infographic above shows typical market-style ranges for those structures. Those figures can be useful for orientation, but they aren't enough to make a decision on their own. The actual analysis comes from building an all-in comparison.

What belongs in the all-in model

A CFO should compare proposals using the same categories for every provider:

- Administrative fee. Separate the stated PEO fee from bundled payroll or HR tech charges.

- Medical and ancillary benefits. Review both employer cost and employee contribution impact.

- Workers' compensation. Understand whether the PEO includes coverage, brokers it, or manages it through a master arrangement.

- Payroll tax administration. Confirm who files what, how amendments are handled, and who pays penalties if the provider makes an error.

- Implementation cost. Some providers absorb setup tasks. Others charge for migration, onboarding, or custom integration support.

- Renewal economics. Check rate caps, repricing triggers, and termination timing.

A proposal that looks cheap on page one can become expensive if it has weak controls on renewal or if benefits pricing isn't competitive for the workforce profile.

A practical Florida scenario

Take a mid-sized Florida employer with a mix of office and hourly staff. One provider offers a lower visible admin charge but uses a more rigid service bundle and gives limited flexibility on workers' comp handling. Another comes in with a higher visible fee but stronger benefits alignment, cleaner payroll tax process ownership, and clearer renewal protection.

On paper, the first quote may look cheaper. In practice, the second may be easier to defend because the company can budget it more predictably and avoid unpleasant surprises during the first renewal cycle.

That's why finance teams should model at least two views. One should show expected base-year cost. The other should test how the agreement behaves under hiring growth, wage changes, and benefit elections. A static comparison misses too much.

Workers' comp can change the economics fast

In Florida, workers' comp deserves its own workstream during PEO diligence. Industry classification, claims handling, and audit practices can materially change the value of the relationship. Buyers that need a grounded refresher on state-specific issues should review these essential workers' compensation details before finalizing the model.

Watch for this: a provider that simplifies the quote by burying workers' comp assumptions in general pricing language usually needs more scrutiny, not less.

The same goes for cost benchmarking tools. A structured PEO cost comparison framework helps buyers normalize dissimilar proposals so the decision isn't driven by whichever salesperson packaged the spreadsheet more neatly.

Comparing PEO Providers National vs Florida-Specialist

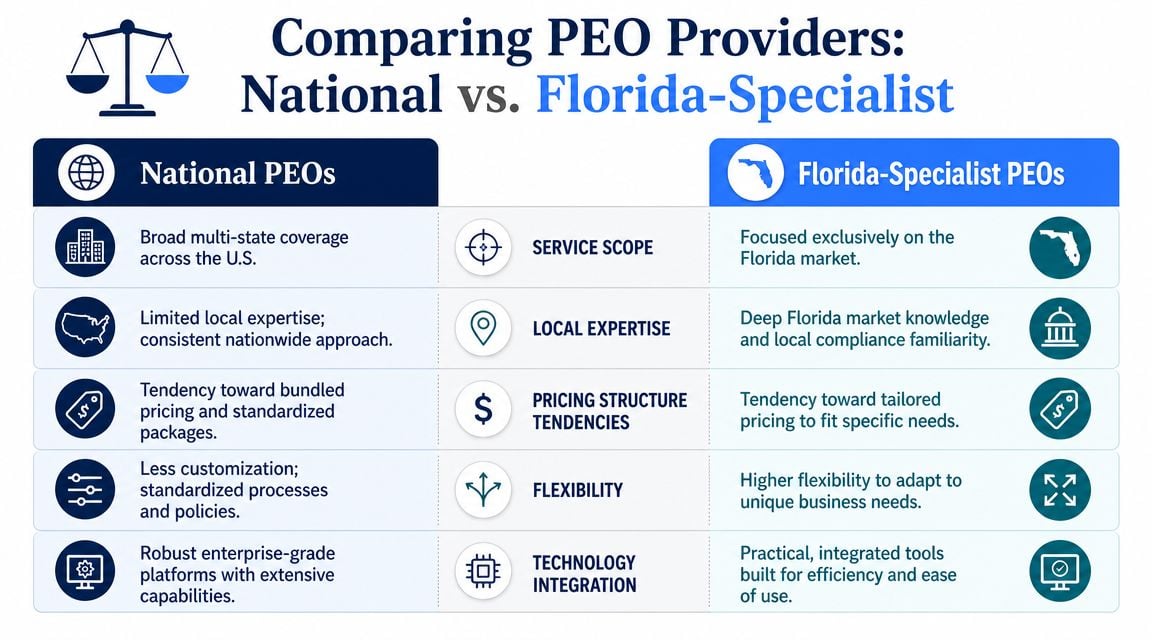

A CFO entering Florida usually sees two polished stories. The national firm sells scale, systems, and multi-state readiness. The Florida specialist sells access, speed, and local judgment. Both can be right. The mistake is treating this as a brand comparison instead of a contract and operating model decision.

| Decision Criterion | National PEOs (e.g., ADP TotalSource, Insperity) | Florida-Specialist PEOs (e.g., Regional Providers) |

|---|---|---|

| Service model | More standardized processes, often broader teams | More localized relationships, often more direct access |

| Benefits approach | Strong scale and packaged offerings | May offer more hands-on tailoring within a narrower structure |

| Technology platform | Usually more developed proprietary systems | May rely on simpler stacks or selected third-party tools |

| Compliance support | Better fit for multi-state complexity | Better fit for Florida-specific operating detail |

| Pricing and flexibility | Can be rigid on terms, strong on standardization | Can be more negotiable, but not always broader in scope |

What changes in the service model

National PEOs usually win on repeatability. Payroll, onboarding, benefits administration, reporting, and ticket handling are built around standard workflows. That matters if the company expects to hire outside Florida soon or wants fewer exceptions in HR operations.

The trade-off shows up after implementation. A dedicated service team can still mean separate contacts for payroll, benefits, leave, and risk, with handoffs between them. For some finance leaders, that structure is fine because it scales. For others, it creates friction because no single person owns the issue from start to finish.

Florida-specialist PEOs often compete on direct access and faster judgment calls. That can be valuable for employers dealing with field-based teams, variable schedules, claims questions, or payroll practices that do not fit a standard playbook. In a Florida-heavy operation, speed and accountability can matter more than a polished portal.

Where negotiation power usually shifts

The size of the Florida PEO market gives buyers more room than sales reps suggest, especially if they run a real process with competing proposals. National firms tend to hold the line on master service terms but may give ground on implementation support, reporting setup, or service credits. Florida-focused firms are often more open to contract edits, renewal controls, and named service commitments because local relationships are part of the sale.

That difference matters in procurement.

If a national provider is the better operating fit, ask for specifics that reduce execution risk: implementation milestones, escalation contacts, response-time standards, and clearer repricing language at renewal. If a Florida specialist is the better fit, test whether the flexibility is institutional or just tied to one experienced account manager. A custom promise is only worth something if the provider can deliver it after staffing changes.

A disciplined buyer should also press both sides on what happens when the business outgrows the original model. That is where many first-year quotes stop being useful. A practical PEO due diligence checklist for contract and service review helps finance and HR compare those terms on the same basis.

Which model fits which employer

A multi-state employer or a company expecting near-term expansion usually gets more value from a national platform. The reason is less about prestige and more about operating consistency. Once hiring spreads across several states, fragmented processes become expensive.

A Florida-based employer with concentrated in-state headcount may get more from a specialist if that provider shows real strength in claims handling, payroll execution, and local support coverage. This is common in industries where workforce issues are operational, not just administrative.

There is also a middle case. A company with one Florida headquarters and an uncertain expansion timeline should compare switching risk, not just first-year price. I usually advise CFOs to ask a blunt question: if the company doubles headcount or adds three new states, does this PEO still fit, or does it become a migration project?

PEO Metrics is often part of that process as an independent comparison resource. The useful part is not the branding. It is the side-by-side review of pricing structure, contract terms, service model, and fit, which makes it easier to see whether a national provider is charging for capabilities the company will use, or whether a Florida specialist is offering attractive flexibility without enough operating depth.

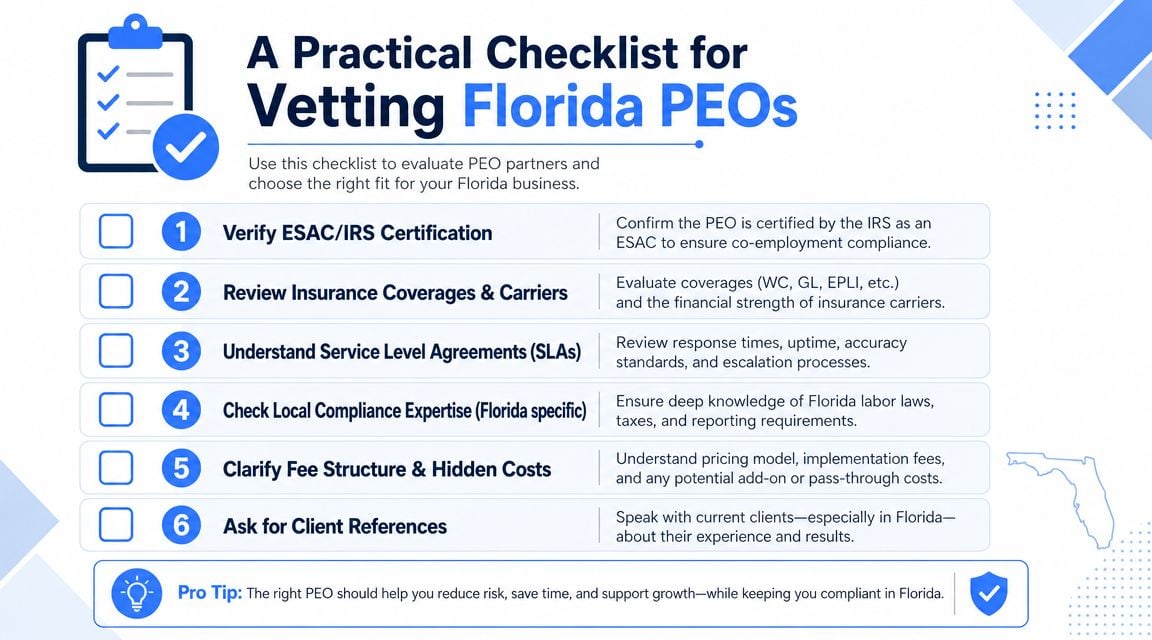

A Practical Checklist for Vetting Florida PEOs

A Florida PEO agreement should be read like an operating contract, not a marketing document. Most problems show up after go-live, but the warning signs are usually visible in the proposal, service agreement, insurance language, and implementation plan.

Contract clauses that deserve redlines

Some terms should trigger immediate follow-up from finance, HR, and legal.

- Termination language. Check the notice period, early termination fee, and any implementation cost clawback. A short, clean exit right is worth more than a polished launch presentation.

- Renewal mechanics. Look for automatic renewals, vague repricing language, and one-sided fee adjustment rights. If the provider can reset economics too broadly, the first-year quote doesn't mean much.

- Tax liability allocation. The agreement should state what happens if the PEO makes a payroll tax filing error. “We handle payroll taxes” is not the same as accepting responsibility for penalties caused by the provider.

- Service scope. Ask what is excluded. Recruiting, leave case management, handbook updates, integrations, and custom reporting are common gray areas.

- Implementation ownership. Clarify who migrates employee data, who validates deductions, and who signs off on first payroll accuracy.

A useful negotiation move is to tie broad provider discretion back to objective process. If the contract allows fee changes, ask for notice timing, documentation standards, and a defined client right to review or terminate before the change takes effect.

Insurance and tax questions to ask before signing

Workers' comp and related insurance terms deserve unusually close review in Florida. The National Association of Insurance Commissioners notes that PEO insurance must cover the client's full workforce unless other insurance provides complete “catch-all” protection, which means partial arrangements can create dangerous coverage gaps (NAIC PEO coverage guidance).

That leads to several practical questions:

- Which employees are covered under the PEO's arrangement? Titles aren't enough. The provider should identify the full covered population.

- Are any classes, locations, or subsidiaries carved out? If yes, the client needs written proof that the outside coverage fully closes the gap.

- Who controls claims administration and reporting? Delays and handoff confusion get expensive fast.

- How are payroll audits and classification disputes handled? The contract should describe process, not just intent.

Don't accept “we've never had an issue” as an answer to an insurance structure question. Ask for the policy logic, the carrier structure, and the written client responsibility map.

A short diligence list that actually works

A practical Florida review usually includes these checks before signature:

- Verify licensure and standing. Confirm the provider's Florida operating status and ask who monitors it internally.

- Request the service map. Get names or roles for payroll, HR, benefits, claims, and escalation contacts.

- Review sample invoices. Buyers should see how fees, taxes, benefit deductions, and insurance charges appear in practice.

- Stress-test the renewal. Ask what changed for similar clients at renewal and how notice is delivered.

- Read all insurance exhibits. Don't stop at the summary page.

- Run references by business type. A healthcare employer should talk to healthcare clients. A contractor should talk to contractors.

Teams that want a more disciplined diligence process often work from a formal PEO due diligence checklist so legal, HR, and finance review the same risks instead of running separate conversations.

Making Your Final PEO Decision in Florida

The final decision usually gets easier when the leadership team stops asking which proposal looks best and starts asking which operating model creates the fewest future problems.

A short decision screen works well:

- What is the main problem to solve right now? If the core issue is fragmented HR administration, several PEO models may work. If the issue is complex hiring across multiple states, the shortlist should narrow quickly.

- How Florida-centric is the workforce likely to remain? A company staying concentrated in Florida may value local operating fit more than broad national standardization.

- How much service variability can the team tolerate? Some employers want direct, relationship-heavy support. Others prefer a process-driven platform even if it feels less personal.

- Which proposal is most defensible on total cost, not headline fee? That means reviewing benefits, workers' comp, payroll tax workflows, implementation burden, and renewal protections together.

- How easy is it to leave if the relationship underperforms? Exit rights matter more than most buyers think.

The strongest choice is usually the provider whose contract, service design, and compliance handling still look solid after the sales pitch has been stripped away. In Florida, that discipline matters because there are plenty of providers, but not all of them fit the same risk profile.

A good PEO decision should survive three tests. The finance team can budget it. HR can operate it. Leadership can live with the contract if things change.

PEO buyers that want an independent second look can use PEO Metrics to compare providers, benchmark pricing and benefits, and review contract terms before choosing a Florida PEO or renegotiating an existing agreement.