A finance leader usually starts a California PEO search with a simple question. Will this lower admin load and improve benefits?

That's the wrong opening question in California. The better one is whether the provider will help the company control compliance process risk without creating a false sense of protection.

For an employer with staff in California, a professional employer organization isn't just a payroll and benefits decision. It's a decision about workers' compensation structure, wage and hour execution, leave administration, documentation discipline, service responsiveness, and contract language that only matters once something goes wrong.

Table of Contents

- Why Choosing a PEO in California Is Different

- Understanding the Co-Employment Model in California

- Navigating the California Compliance Gauntlet

- How to Compare PEO Pricing and Benefits

- Evaluating Contract Risk and Service Models

- A Practical Checklist for California PEO Due Diligence

- Why Independent Benchmarking Improves Your PEO Decision

Why Choosing a PEO in California Is Different

A company in a lower-complexity state can often evaluate a PEO like an outsourced back office. Payroll gets processed, benefits get bundled, HR questions get routed, and the decision mostly turns on price and convenience.

California changes that math.

A California employer has to think about wage statements, meal and rest break administration, local paid sick leave overlays, workers' compensation structure, safety coordination, termination handling, and documentation that may later be reviewed in a claim, audit, or dispute. The PEO relationship can reduce friction in those processes, but it can also magnify risk if the provider's systems are generic or the contract leaves critical gaps.

California raises the stakes

The national market is large and mature. IBISWorld projects the U.S. Professional Employer Organizations industry at $254.8 billion in 2026 with 6,675 businesses operating in the sector. That scale gives California buyers options, but it also creates noise. Two providers can both call themselves full-service PEOs while offering very different service models, insurance structures, and contract terms.

That's why a California professional employer organization review has to start with exposure mapping, not with a demo.

A useful first screen is simple:

- Workforce profile: Does the company have hourly staff, multiple locations, field employees, or local ordinance exposure?

- Claims sensitivity: Would a workers' compensation dispute, payroll tax issue, or wage claim create a material operational distraction?

- Internal capacity: Can the company audit the provider's output, or will managers assume the PEO “has it covered”?

- Contract tolerance: Is leadership prepared to negotiate liability language, renewal terms, and service commitments?

Practical rule: In California, a PEO should be evaluated as a risk-management partner with an administrative engine attached, not as a software subscription with HR add-ons.

The buyers that make better decisions usually separate three questions. What risk is being shifted, what work is being standardized, and what liability stays with the employer anyway. That framework helps leadership avoid overbuying convenience and under-reviewing exposure.

For companies that want to map that exposure before comparing providers, a focused review of state law compliance exposure in PEO arrangements is often more useful than another generic vendor checklist.

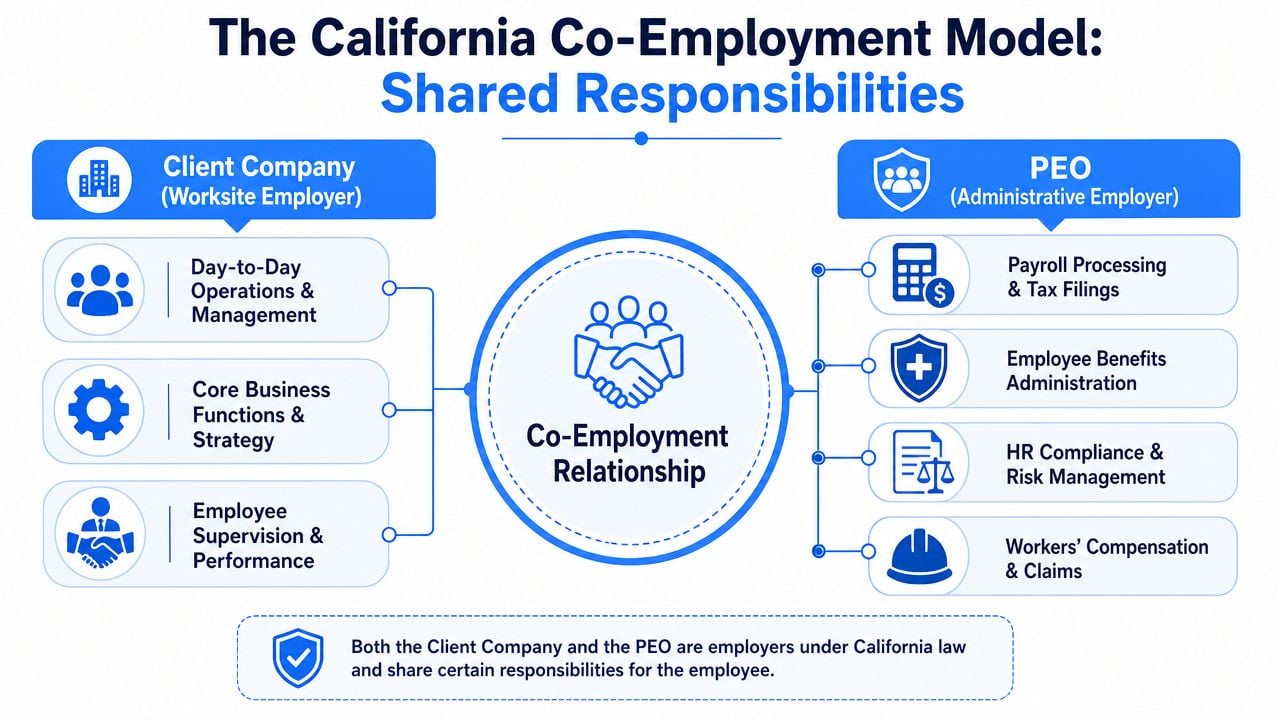

Understanding the Co-Employment Model in California

Most PEO sales conversations make co-employment sound cleaner than it is. In practice, it works well when both sides respect the line between administrative responsibility and operational control.

In California, that line matters because the employer can't outsource day-to-day management discipline and then expect the PEO to absorb every downstream issue.

Who handles what

Operationally, a California PEO can centralize payroll, tax withholding, benefits administration, and HR compliance support, while the client retains day-to-day management and employment decisions. Deel's California PEO guide describes the model as one where the PEO typically manages payroll taxes, workers' compensation coverage, and HR guidance, while the business keeps control of hiring, firing, and operations.

That's the clean version. The actual version looks more like this:

| Responsibility area | Client company | PEO |

|---|---|---|

| Hiring decisions | Owns | Supports process if contracted |

| Supervision and scheduling | Owns | Doesn't run operations |

| Payroll processing | Supplies accurate inputs | Processes payroll and filings |

| Benefits administration | Chooses within offered structure | Administers enrollment and service |

| HR policy guidance | Applies policy in the workplace | Advises on policy framework |

| Workers' comp administration | Manages workplace realities | Coordinates coverage and claims process |

A CFO should read that table with one question in mind. Where can bad inputs from the company still create a compliance problem even if the PEO executes the back-end workflow correctly?

Where companies get confused

The confusion usually shows up in three places.

- Timekeeping and premium pay: The PEO can process payroll, but it can't fix inaccurate punches, missed attestations, or manager practices that create off-the-clock risk.

- Leave administration: The provider may track leave categories and documentation steps, but supervisors still create problems when they say the wrong thing or apply rules inconsistently.

- Terminations: The PEO may provide guidance, final pay workflow support, and documentation templates, but the employer still controls the underlying decision and how it is carried out.

A good co-employment model reduces process burden. It does not replace management judgment or local execution discipline.

That distinction is why the best-fit provider for one California employer can be the wrong one for another. A founder-led company with a lean office staff may need stronger administrative lift. A larger business with an internal HR team may care more about claims coordination, technology integration, and escalation quality.

Buyers who want a sharper breakdown of those lines should review how PEO co-employment works in practice. It's often the fastest way to identify where the company expects transfer of responsibility, but the contract only provides support.

Navigating the California Compliance Gauntlet

A weak PEO can make California risk look organized right up until a claim, audit, or plaintiff letter tests the process. That's why compliance review has to go beyond “Do you support California?”

The useful question is narrower. How does the provider handle the pressure points that create real employer exposure?

Workers' compensation is not a handoff

California's own guidance is clear on a point many buyers miss. The state warns employers to verify that the PEO's workers' compensation carrier has a California Department of Insurance certificate of authority, and it states that using a PEO does not release the employer from liability for ensuring employees are covered by a valid workers' compensation policy.

That has immediate due diligence consequences.

- Verify the carrier: Don't accept a sales summary. Ask for the carrier structure and confirmation that the insurer is authorized in California.

- Review the policy framework: Ask how employee classifications, additions, and removals are handled.

- Check cancellation procedures: If the relationship ends badly, the company needs clarity on how coverage transitions.

A buyer that treats workers' comp as “the PEO's problem” is taking the wrong posture from day one.

Wage and hour failures usually start in operations

Most California wage and hour problems aren't caused by a payroll engine. They start with scheduling, time entry, break practice, shift changes, manager behavior, or bad approvals.

A competent PEO helps by standardizing inputs, enforcing payroll calendars, flagging missing data, and giving the employer a framework for compliant administration. A weak one merely processes what it receives.

When payroll corrections are frequent, supervisors approve time retroactively, or off-cycle payments happen too often, finance and HR should work together. The issue isn't just administrative inefficiency; it signals process instability.

For companies reviewing these workflows, a focused guide to wage and hour compliance responsibilities can help separate system issues from management issues.

Leave administration is a consistency test

California leave administration breaks down when different managers improvise. One supervisor allows an informal accommodation. Another demands paperwork immediately. A third delays escalation to HR.

A strong PEO creates a repeatable intake and documentation process. That doesn't eliminate every risk, but it reduces the chance that the company handles similar situations in inconsistent ways.

PAGA risk changes the standard

California's litigation environment forces employers to think in systems, not isolated incidents. A single policy gap matters less than a repeated practice spread across locations or managers.

That's why CFOs should care about process design, audit trails, and escalation paths. The right provider helps the company build repeatable controls around payroll, leave, timekeeping, onboarding, and separation. Businesses that need a broader legal framework for ensuring business legal compliance should also review outside counsel guidance alongside the PEO contract. The provider can support compliance execution, but it doesn't replace legal review.

How to Compare PEO Pricing and Benefits

PEO pricing discussions often become messy because buyers compare proposals that aren't built on the same assumptions. One quote may bundle workers' comp administration differently. Another may place more cost inside the benefits package. A third may look cheap until implementation fees, add-on HR support, or renewal language surface later.

A clean comparison starts by forcing every provider into the same financial worksheet.

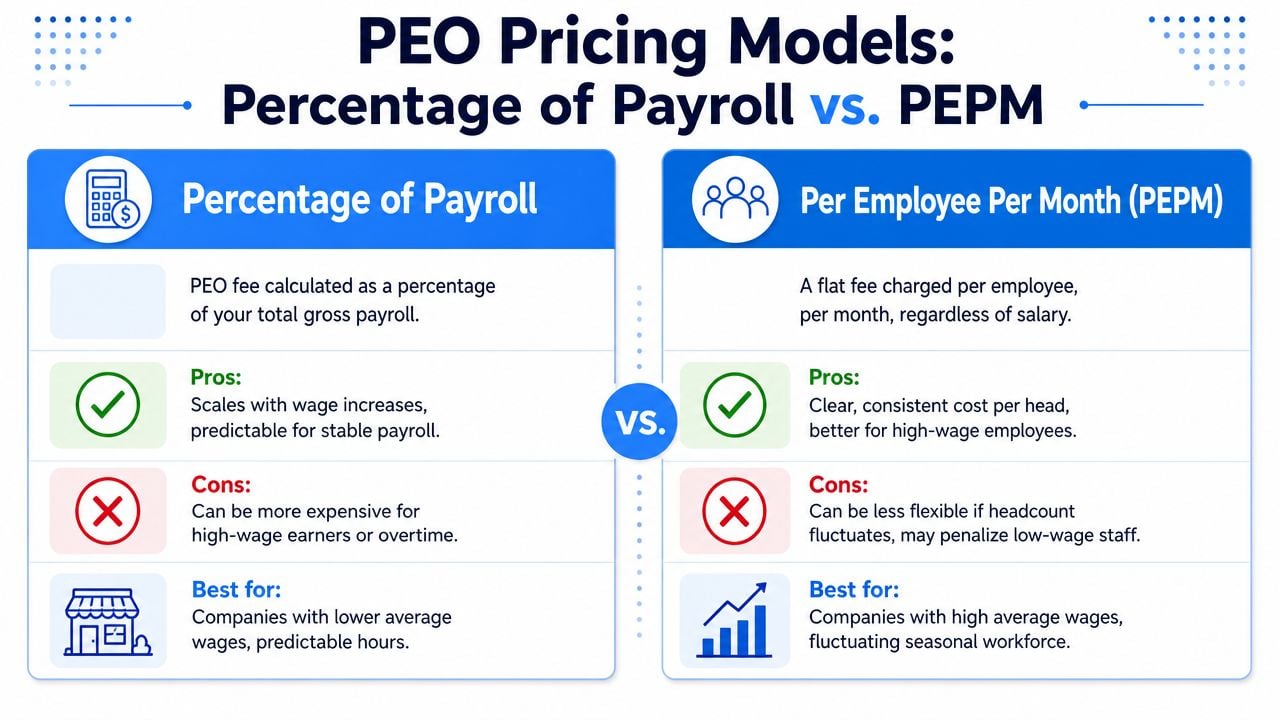

Two pricing models that behave differently

Most proposals land in one of two buckets.

| Pricing model | How it works | Usually fits better when |

|---|---|---|

| Percentage of payroll | Fee rises as payroll rises | Payroll is stable and average wages are lower |

| Per employee per month | Flat fee per headcount | Wages vary widely or headcount planning is more predictable |

The key difference is what drives cost drift.

A percentage-of-payroll model can become more expensive when overtime rises, higher-paid employees are added, or compensation grows. A per-employee-per-month model creates cleaner budgeting per head, but can feel inefficient for low-hour or low-wage populations if service needs are light.

Buying advice: Ask every provider to restate the proposal in the other pricing format. That single step exposes whether the quote is genuinely competitive or just framed attractively.

What to compare beyond the admin fee

The admin charge matters, but a California professional employer organization decision usually swings on total employment cost, not the visible fee line.

A disciplined comparison should include:

- Medical plan access: Compare carrier networks, employee contribution strategy, plan design flexibility, and whether the plans fit the workforce's geography.

- Payroll and tax scope: Confirm what is included in processing, tax filings, amendments, off-cycle runs, and support.

- Workers' comp administration: Clarify what service is included for claims coordination, audits, and reporting.

- Technology stack: Review HRIS usability, manager workflows, onboarding, timekeeping integration, and reporting.

- Service delivery: Identify whether the account will have named specialists or a pooled support queue.

Benefits should be tested like a finance decision

Benefits comparisons go wrong when buyers focus only on premium labels and ignore usability. A richer-looking health plan isn't better if the employee network fit is poor or the enrollment support is weak.

Finance should ask HR to score benefits in two ways. First, how competitive the package is for hiring and retention. Second, how predictable the employer contribution strategy will be over time.

The insurance side also deserves plain-language review. A practical starting point is understanding how PEO insurance structures typically work and where coverage administration intersects with the service agreement. That usually reveals hidden assumptions in proposals that looked similar on first pass.

Evaluating Contract Risk and Service Models

A polished demo can hide a bad contract. In California, that's dangerous because the legal and operational consequences rarely show up during implementation. They show up during renewal, termination, a claim, or a dispute over who was supposed to handle what.

The strongest buyers spend as much time on contract mechanics as they do on benefits and technology.

Liability language matters more than the sales pitch

A California Lawyers Association webinar notes that the Appeals Board has clarified a PEO can be considered an employer in a workers' compensation case, and even if it is not treated as the employer under the traditional test, it may still face contractual liability for insurance coverage in arbitration. That issue matters because liability allocation depends not only on the operating relationship, but also on the agreement the parties signed. The webinar summary is available through the California Lawyers Association event page on PEOs in workers' compensation cases.

That should change how buyers read the agreement. If the contract is vague, the company may learn what the provider meant only after a problem emerges.

Three contract terms that deserve red-flag treatment

First, review termination language carefully. Notice periods, automatic renewals, and conversion mechanics can trap a company in a poor fit longer than expected. The issue isn't just legal inconvenience. It's the operational risk of being unable to exit cleanly when service quality slips.

Second, look for broad disclaimers around compliance support. Many providers promise guidance, but the agreement limits responsibility heavily. That may be reasonable, but leadership should know when “support” means recommendations only, not accountability for execution.

Third, check fee adjustment terms. Renewal language that allows open-ended increases or vague pass-through charges creates budget uncertainty. For a CFO, that turns a supposedly stable outsourcing arrangement into an unpredictable expense line.

Service model risk is operational risk

Two PEOs can have similar pricing and radically different service outcomes.

A dedicated service team usually supports more continuity in payroll issue resolution, leave questions, and escalation handling. A pooled service center may still work well, but only if response standards are strong and the company's internal HR team can manage more of the complexity directly.

Ask practical questions, not marketing questions:

- Who handles urgent payroll issues on processing day?

- Who helps when a termination must be coordinated quickly?

- Who owns open items after implementation?

- How are California-specific escalations routed?

Contract review should answer one operational question. When something breaks, who does what by when, and what happens if they don't?

That's the standard. Not whether the proposal feels complete.

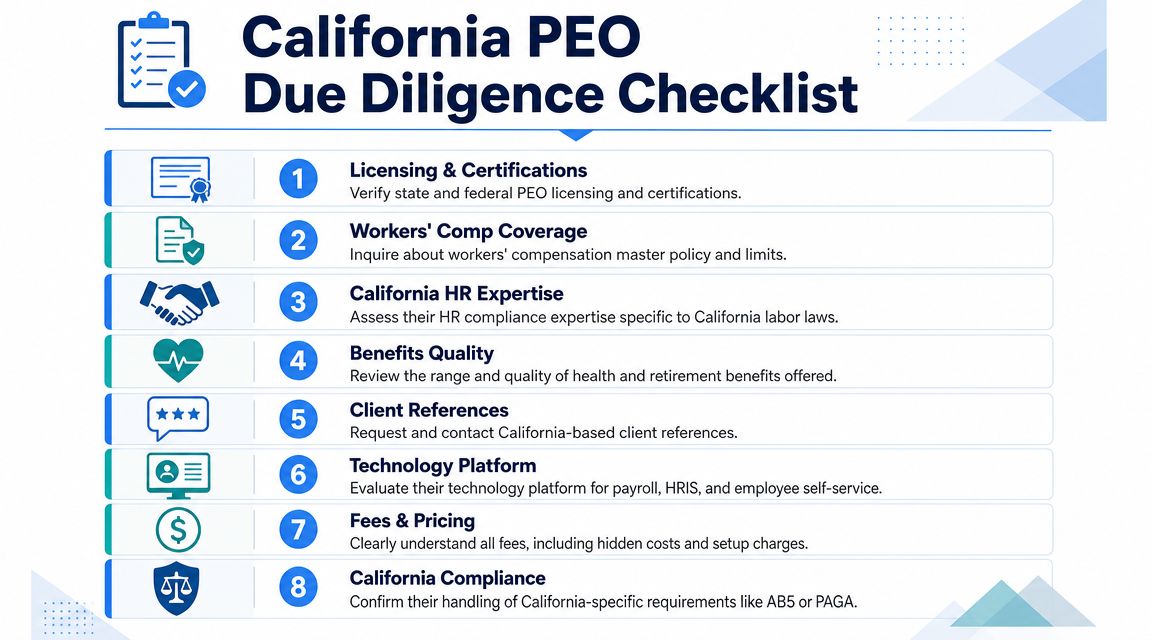

A Practical Checklist for California PEO Due Diligence

Most discovery calls are too polite. Buyers ask broad questions, vendors give broad answers, and everyone leaves with the impression that the provider can “support California.”

A better approach is to use a script that forces specificity.

Compliance questions

- Workers' comp structure: Which carrier is used, how is California coverage maintained, and what happens if the relationship terminates mid-policy period?

- Local ordinance handling: How does the platform track location-based rules for wages, leave, and policy administration?

- Escalation process: If a wage complaint, leave dispute, or agency notice appears, who takes point and what is the response workflow?

- Documentation discipline: What records are retained, where are they stored, and how does the client access them during a dispute?

Pricing and benefits questions

- Fee transparency: What charges sit outside the quoted admin fee?

- Renewal mechanics: Which costs can change at renewal, and which can be locked?

- Plan fit: Which medical options are strongest for the company's employee footprint and recruiting profile?

- Implementation costs: What work is included in onboarding versus billed separately?

Contract and service questions

- Termination terms: How much notice is required, and what support is provided for offboarding?

- Liability language: Where does the agreement assign responsibility for payroll errors, tax issues, and compliance support gaps?

- Named contacts: Will the company have dedicated payroll, HR, and benefits contacts?

- Service standards: What happens when the provider misses a payroll deadline or fails to resolve an open issue?

The right answer is rarely the shortest one. If a provider can't walk through process detail, the company should assume the detail gets improvised later.

For teams that want to formalize this review, a structured PEO due diligence checklist for buyers can make side-by-side comparison easier and cut down on subjective scoring.

Why Independent Benchmarking Improves Your PEO Decision

PEO buying is an opaque market. Pricing isn't public. Contract language varies. Service models are described in marketing language that often sounds interchangeable. That creates an information gap, and the employer usually absorbs the cost of that gap.

Independent benchmarking closes it.

NAPEO states that 14% of employers with 20 to 499 employees use a PEO, that the industry supports 4.5+ million jobs, and that roughly 230,000 businesses use PEO services. That level of adoption means buyers aren't entering an experimental model. They're entering a negotiated market where providers know far more than first-time or infrequent buyers do.

Why benchmarking changes leverage

Without a market reference point, a company can't easily answer basic negotiation questions.

Is the proposed fee structure competitive for this workforce profile? Are the renewal terms standard or aggressive? Is the service model aligned with price? Is the provider shifting unusual risk into the client agreement?

Those are benchmarking questions, not sales questions.

A company can gather that intelligence internally if it has enough time and enough exposure to multiple provider structures. Most don't. That's why some employers use brokers, some rely on counsel for contract review, and some use an independent advisory process such as PEO Metrics to compare pricing, benefits, service model, and contract terms side by side before signing.

Better decisions come from outside context

The biggest mistake in a California PEO search is assuming the decision is complete once a provider looks credible and the price seems acceptable. That's not due diligence. That's selection under uncertainty.

A stronger process validates three things:

- Market fairness: The company isn't overpaying for the service model offered.

- Contract balance: Renewal, exit, and liability terms are understood before signature.

- Operational fit: The provider's California execution model matches the company's actual risk profile.

A PEO can lower administrative strain. Only a well-benchmarked deal lowers decision risk.

That's the practical takeaway for CFOs, HR directors, and owners. In California, the right professional employer organization isn't just the one that can process payroll and offer benefits. It's the one whose pricing, service design, and contract structure hold up under scrutiny before the first problem lands on the company's desk.

PEO Metrics helps companies compare, select, and negotiate PEO options with an independent view of pricing, benefits, contract terms, service models, and fit. For California employers weighing a new PEO, a switch, or a renewal, PEO Metrics can provide a side-by-side benchmark so the final decision is based on market context instead of vendor positioning.