Most advice on professional employer organization health insurance is too shallow. It treats the decision like a shopping exercise for lower premiums. That's lazy analysis, and it leads companies into bad contracts.

A PEO health plan is not just a benefits product. It's a co-employment arrangement that changes who handles payroll, benefits administration, parts of compliance, and parts of employment risk. If leadership only compares monthly premiums, leadership misses the true issue: total cost of employment management.

That matters even more for companies with lean HR teams, multi-state headcount, or uneven claims history. A cheaper plan can still be a worse deal if the contract locks the business into weak service, opaque fee increases, or a painful exit. On the other hand, a PEO can be the right move when it stabilizes administration and gives access to stronger benefits than the standalone market can realistically deliver.

For organizations with specialized workforce needs, benefit design also has to fit the employer type. Leaders comparing broader workforce strategies may find useful context in this roundup on employee benefit programs for nonprofits, especially where mission-driven employers face tight budgets and retention pressure.

A smarter evaluation starts with the full operating picture, not the sales deck. Companies weighing the trade-offs should first understand the pros and cons of using a PEO before comparing any specific health offering.

Table of Contents

- The Strategic Decision Beyond Cheaper Premiums

- How PEO Health Insurance Actually Works

- PEO vs ASO Broker and Direct Purchase Models

- Unpacking the True Cost of PEO Health Insurance

- Solving for Multi-State Compliance Complexity

- Negotiating Your Agreement and Avoiding Contract Pitfalls

- How to Benchmark and Make a Final Decision

The Strategic Decision Beyond Cheaper Premiums

The biggest mistake buyers make is assuming professional employer organization health insurance is mainly a way to cut benefit spend. Sometimes it does that. But the core purchase is broader: access to pooled benefits, outsourced administration, and a different operating model.

That distinction matters because premium savings can distract from harder questions. Who owns the employee experience? How quickly does the service team fix payroll mistakes? How painful is implementation? What happens at renewal if rates move and the contract gives the provider too much room to reprice? Those issues hit the P&L just as surely as premiums do.

A PEO relationship is often strongest when the company has one of three conditions: a small HR team, multi-state complexity, or a workforce profile that struggles in the small-group market. It is often weakest when the company wants deep plan customization, highly specific carrier relationships, or complete control over every benefits decision.

Bottom line: A CFO should treat a PEO quote like a combined procurement decision across benefits, HR operations, compliance support, and contract risk.

This is why cheap quotes alone shouldn't win. A lower medical rate paired with vague service language and rigid termination terms can create more pain than the savings justify. A disciplined buyer evaluates net economics, operational fit, and exit flexibility together.

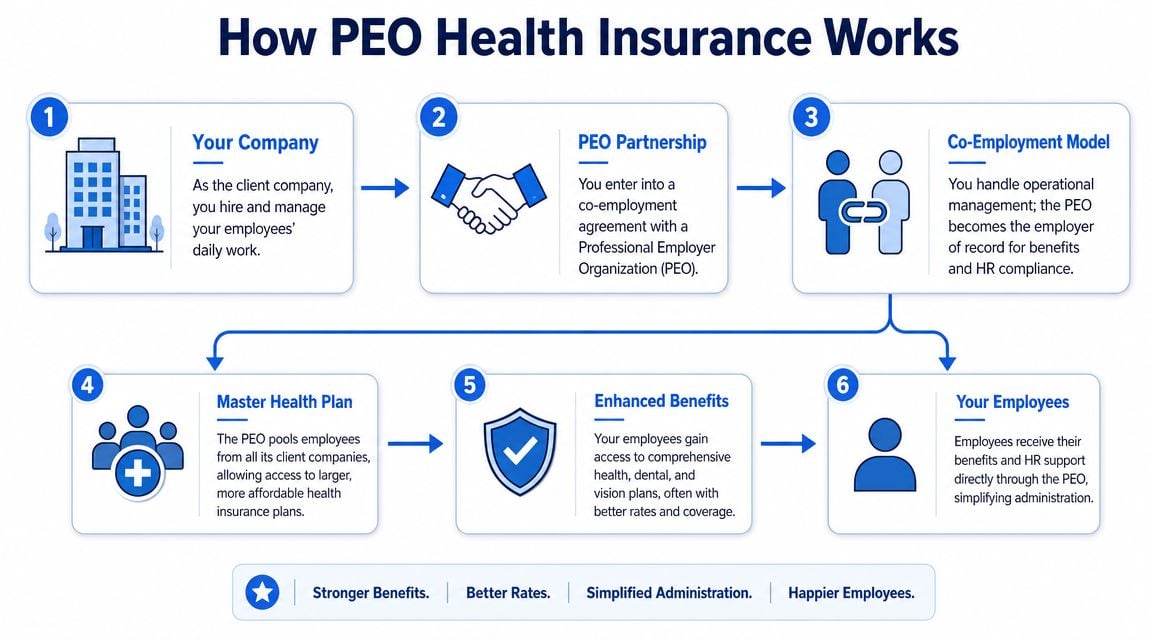

How PEO Health Insurance Actually Works

A simple way to think about professional employer organization health insurance is this: a smaller employer joins a larger buying structure instead of standing alone in the market.

The co-employment structure

In a PEO model, the client company still directs day-to-day work. The company hires, manages, evaluates, and, when necessary, terminates employees. The PEO steps in on the administrative side as the employer of record for payroll and benefits purposes under the co-employment agreement.

That structure is the legal engine behind the insurance offering. Instead of each client trying to buy coverage as an isolated employer, the PEO aggregates many client workforces into a larger population. That larger pool is what gives the model its advantage.

A buyer that needs the basics spelled out cleanly should review a plain-language overview of what PEO insurance is. It helps clarify why the insurance piece can't be separated from the service model.

Why the master plan changes the buying power

The practical effect is straightforward. A small or midsize employer may gain access to large-group purchasing power through the PEO arrangement. Industry research from NAPEO says businesses that hire a PEO grow twice as fast, have 12% lower employee turnover, and are 50% less likely to go out of business than similar firms that don't use one, which helps explain why the bundled benefits model became so attractive in the first place (NAPEO industry research).

The plan itself is commonly offered through a master policy or large-group style arrangement. That means the employer is no longer shopping exactly the way a standalone small group shops. The PEO collects the employer contribution and employee deductions through payroll administration, manages enrollment workflows, and supports ongoing benefits operations.

A 50-person company doesn't suddenly become a large corporation. But inside the PEO structure, it may buy health coverage more like one.

That's the core appeal. The company keeps operational control of the workforce while the PEO handles much of the benefits administration under a broader risk pool.

There's also a legal history behind this model. A New York State Insurance Department opinion from 2005 confirmed that certain PEO-related health coverage structures were permitted, which reflected growing regulatory recognition of the arrangement described in the same NAPEO background above.

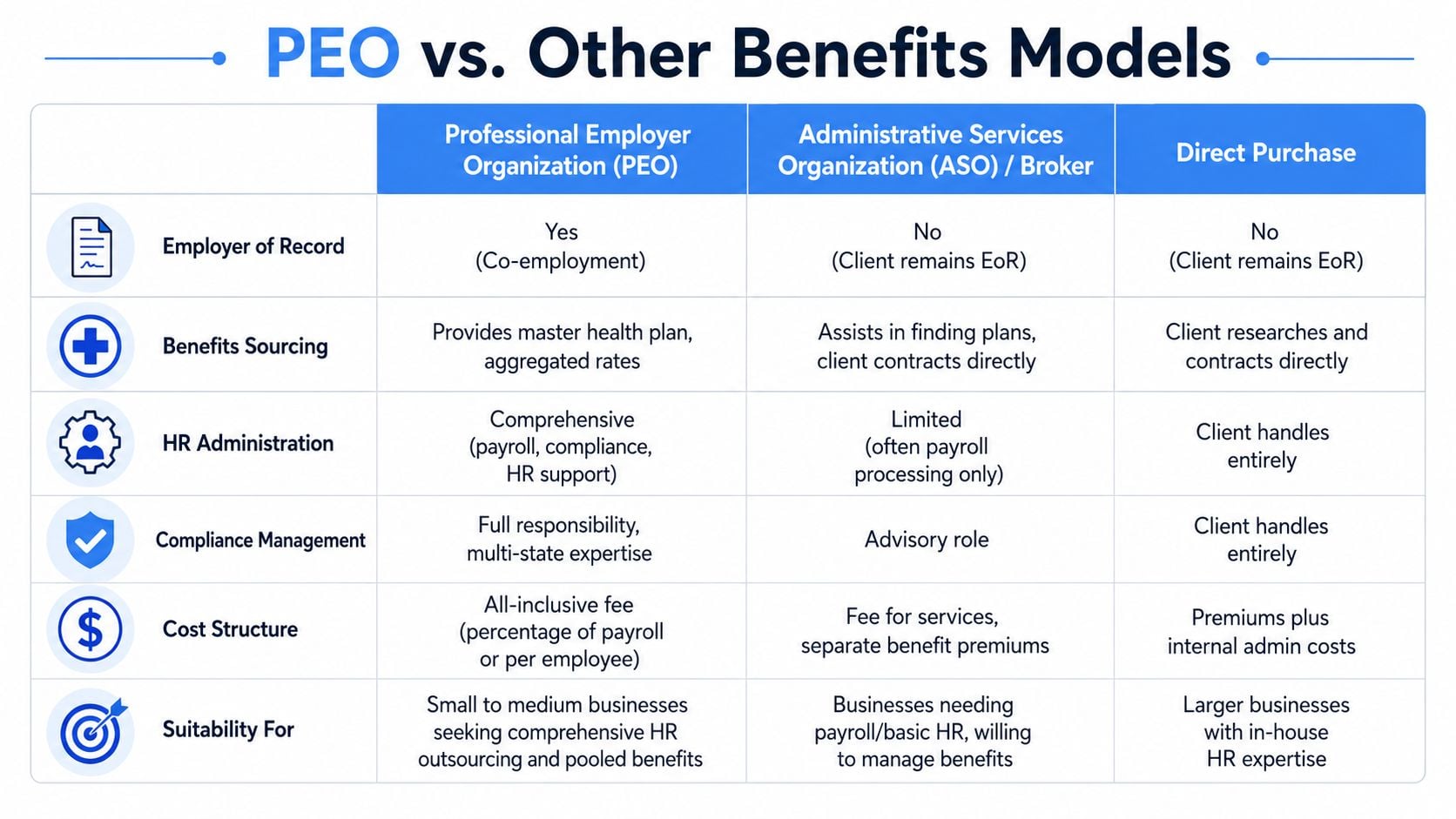

PEO vs ASO Broker and Direct Purchase Models

A PEO is only one path. Buyers should compare it against an ASO, a traditional broker-led setup, and direct carrier purchase before making any call.

Who carries what

The cleanest distinction is legal and operational. In a PEO, the relationship involves co-employment. In an ASO or broker model, the client remains the employer of record and the benefits contract typically sits more directly with the employer. In a direct purchase model, the employer owns even more of the work.

The comparison gets easier in a simple framework:

| Model | Risk and liability posture | Cost structure | Admin burden | Control level |

|---|---|---|---|---|

| PEO | Shared operational structure through co-employment | Bundled fees, often per employee or percentage of payroll | Lower day-to-day burden | Less control over plan design |

| ASO or broker | Employer retains more direct responsibility | Service fees and separate premiums | Moderate burden | More control |

| Direct purchase | Employer carries the most direct responsibility | Premiums plus internal labor cost | Highest burden | Highest control |

Leaders evaluating these structures side by side should also review a focused PEO legal structure vs ASO comparison because the health plan question is really a legal structure question first.

Where control gets tighter or looser

A PEO often wins on convenience. Payroll, onboarding support, benefits administration, and portions of compliance are centralized. That's valuable when HR is stretched thin or when leadership is tired of managing disconnected vendors.

But convenience has a cost. A company may have fewer carrier options, fewer plan design choices, and less control over timing. If a leadership team wants a very specific network, carve-out strategy, or custom contribution philosophy, the PEO menu may feel tight.

By contrast, a broker or ASO model usually preserves more decision-making control. The employer can often shape plan design more precisely and maintain direct carrier relationships. The trade-off is simple. Internal HR and finance staff have to carry more process weight.

A direct purchase model makes sense for companies that already have the people, systems, and discipline to manage enrollment, eligibility, vendor oversight, and ongoing issue resolution internally. For many mid-market companies, that sounds appealing until open enrollment, ACA administration, leave coordination, and payroll corrections start stacking up.

The right model depends less on ideology and more on operating capacity. If the business can't reliably administer a complex benefits program, “control” becomes a liability.

A buyer shouldn't ask which model is best in the abstract. The right question is which model fits the company's internal bandwidth, compliance exposure, and tolerance for administrative drag.

Unpacking the True Cost of PEO Health Insurance

The headline promise is familiar: lower benefits costs. That may be true, but buyers who stop there are doing half the job.

A common benchmark is that employers often see 15% to 30% lower benefit costs with a PEO, although net savings depend on the administrative fee and plan design. The same industry source says businesses using PEO services report an average 27% ROI when broader compliance and efficiency gains are included (Native Teams guide to PEO health insurance).

Fee structure matters more than most buyers expect

Most PEOs price the service bundle in one of two ways:

- Per employee per month fees. These are usually easier to budget and easier to compare across vendors.

- Percentage of payroll fees. These can look fine at first and become expensive for high-wage workforces.

That distinction changes the economics materially. A software company with relatively high compensation may dislike percentage-of-payroll pricing because the admin fee rises with wages, not with administrative workload. A labor-heavy employer with lower average wages may land in a different place.

There's another layer. Premium savings and admin savings are rarely distributed evenly across departments. Finance may see one line item improve while HR absorbs implementation strain, payroll has to adjust processes, and managers field employee questions about provider networks and ID cards.

A practical way to model net savings

The right model uses the company's own census, current employer contribution levels, and the proposed PEO fee structure. It should test three scenarios instead of one:

- Best case where the premium reduction holds and service fees stay stable.

- Expected case where the admin fee offsets part of the insurance savings.

- Stress case where renewal pricing tightens and transition costs show up.

A serious buyer should ask for a line-by-line comparison with these inputs:

- Medical and ancillary premiums

- Administrative fee methodology

- Implementation charges

- Payroll and tax administration inclusions

- Any separate benefit technology charges

- Exit-related costs if the arrangement ends

Practical rule: Gross savings are interesting. Net savings decide the deal.

The U.S. Chamber notes that PEO health plans often cost less than open-market plans because pooled buying power and risk pooling can lower premiums while reducing administrative burden, but the economics still depend on age mix, geography, and claims factors in the broader arrangement. That's why no CFO should approve a switch without a full side-by-side net-cost model, not a teaser quote.

A disciplined review also checks whether the proposal buries fees outside the base admin charge. If the answer to “What's excluded?” is vague, the quote isn't finished.

A deeper review of PEO benefit markup transparency can help buyers pressure-test whether a proposal is transparent or just packaged to look simple.

Solving for Multi-State Compliance Complexity

Multi-state employers usually don't move to a PEO because the concept sounds elegant. They move because fragmented administration starts creating avoidable risk.

Why dispersed headcount breaks simple benefit administration

A company with employees in California, New York, and Colorado doesn't just have three offices. It has three compliance environments, different leave expectations, different payroll rules, and often different practical issues around benefits administration.

When that company tries to manage everything in-house with a payroll vendor, a broker, and a small HR team, work falls through the cracks. Eligibility changes lag. COBRA events get messy. State-specific leave administration becomes inconsistent. Employees receive uneven answers depending on who picks up the phone.

A PEO can earn its fee through its structure. The structure centralizes payroll, benefits administration, and a large share of recurring compliance process inside one operating platform.

Where centralized administration earns its keep

The insurance angle matters here too. PEO-style pooled or blended-rate plans can smooth premium volatility by moving away from the age-rated small-group pricing that penalizes many employers. The U.S. Chamber notes that this is especially relevant in states with different small-group thresholds because those rules affect access to large-group-style rating mechanics (U.S. Chamber overview of PEO health insurance).

That's one reason the model can be particularly useful for distributed teams. It doesn't solve every state issue, but it can reduce the chaos of managing benefits and related HR administration through disconnected vendors.

For employers with remote staff in highly specific jurisdictions, it also helps to review state-level risk guides outside the PEO discussion itself. For example, companies with headcount in Hawaii should understand local compliance pressure points such as those covered in this breakdown on Addressing Hawaii labor law risks.

A multi-state employer shouldn't ask whether administration is annoying. It should ask whether inconsistent administration is creating legal and employee-relations exposure.

The companies that benefit most here are the ones already feeling strain. Not in theory. In ticket backlogs, delayed responses, scattered leave tracking, and recurring payroll corrections.

Negotiating Your Agreement and Avoiding Contract Pitfalls

A PEO agreement deserves the same scrutiny as a credit facility or a major software contract. Too many buyers skim the legal terms because the sales process centers on service and savings. That's a mistake.

Questions that expose weak proposals

A strong buying team asks direct questions early, before legal review starts:

- What exactly is included in the admin fee? Payroll processing, benefits administration, compliance help, HR support, and tax handling should be spelled out.

- Which health plans are available in each employee geography? A national logo means little if network access is weak where employees live.

- Who is the service team? Buyers should ask whether support comes from a named team, a call-center queue, or a pooled service model.

- How are renewals handled? The provider should explain timing, methodology, and how much visibility the client gets before effective dates.

- What does implementation require from internal HR and finance? A good implementation plan is operational, not just promotional.

Some questions should be asked twice, once in sales and once in contracting. If the answer changes, the buyer has learned something important.

Contract terms worth pushing hard on

Not every term is negotiable, but many are. Buyers often leave concessions on the table because they don't ask.

The most useful pressure points usually include:

- Implementation fee relief. If the provider wants the business, it can often soften upfront charges.

- Renewal protections. Even if a hard cap isn't available, buyers can ask for clearer methodology, earlier notice, or limits on fee escalators.

- Service level commitments. Response times, escalation paths, and assigned contacts should be documented.

- Data return language. Data ownership and export obligations should be explicit before signing, not debated during exit.

- Termination flexibility. Notice periods and offboarding obligations should be workable.

Buyers don't need a “friendly” contract. They need a readable one with measurable obligations.

Red flags that deserve legal review

Three problem areas show up repeatedly.

First, automatic fee increases buried in renewal language. If the admin fee can rise annually under broad wording, the first-year savings story may not survive.

Second, termination clauses that make exit expensive or operationally painful. Long notice periods, implementation clawbacks, or vague transition support language can trap a client in a deteriorating relationship.

Third, ambiguous responsibility language. If the contract uses broad wording around compliance support without clearly describing scope, the buyer may assume more protection than the document provides.

A disciplined review should also test whether the service agreement matches the proposal deck. If the deck promises dedicated support, the contract should reflect the service model or at least reference the support structure in a meaningful way.

Legal counsel should review the agreement, but HR and finance should mark it up first. They know where the operational pain will surface. Lawyers can tighten language. Internal operators identify where the language is likely to fail in real use.

How to Benchmark and Make a Final Decision

By the time proposals are on the table, many organizations have too much information and not enough structure. The fix is simple. Build a scorecard and force every option through the same lens.

Build a scorecard before the final meeting

The scorecard should compare the top PEO options against the current setup or against a non-PEO alternative. It should include both hard and soft criteria.

A practical framework includes:

| Decision area | What to evaluate |

|---|---|

| Total net cost | Premiums, admin fees, implementation, likely renewal posture |

| Benefits fit | Network access, plan richness, employee disruption risk |

| Service model | Named contacts, escalation path, issue ownership |

| Compliance support | Multi-state handling, reporting support, administrative reliability |

| Contract quality | Fee clarity, exit terms, renewal language, data ownership |

| Technology | Payroll and benefits usability for employees and admins |

The weighting should reflect the company's actual pain points. A distributed employer with recurring leave and payroll issues may weight service and compliance more heavily. A stable single-state employer with a strong internal team may weight control and contract flexibility more heavily.

For teams that need an external reference point, this guide to employee benefits benchmarking is useful because it pushes the conversation beyond premium comparisons.

What a defensible recommendation looks like

The final recommendation should fit on one page. If it can't, the decision still isn't clear.

That document should answer five questions:

- Which option has the best net operating fit?

- Where is the employee disruption risk lowest?

- Which contract creates the least downside at renewal or exit?

- Which provider can support the company's geography and workforce mix?

- What would make leadership regret the decision a year from now?

The winning option isn't the one with the flashiest spreadsheet. It's the one that still looks sensible after service risk, contract risk, and implementation burden are added back in.

A company doesn't need a perfect PEO. It needs one that fits the business better than the alternatives and doesn't hide the actual costs in the fine print.

Companies evaluating or renegotiating a PEO don't need more sales language. They need a clean view of pricing, benefits, contract terms, and trade-offs across real options. PEO Metrics helps HR and finance teams compare providers side by side, spot hidden contract risk, and negotiate stronger terms before signing.