A Georgia CFO usually reaches the PEO decision at the same moment operations get messy. Payroll has become fragile. Benefits renewal is painful. Workers’ compensation questions keep bouncing between HR, finance, and the broker. Then three PEO proposals arrive, all promising lower admin burden, better benefits, and cleaner compliance.

The problem is that most proposals hide the key decision points. The brochure talks about service. The contract assigns liability. The pricing page shows a fee. The actual cost sits in workers’ comp structure, tax handling, benefit funding, renewal language, and termination terms.

For companies evaluating a Professional Employer Organization in Georgia, the right question isn’t which provider has the lowest headline price. It’s which provider can take on the right administrative burden without creating new risk in Georgia’s co-employment framework.

Table of Contents

- Beyond the Quote How to Truly Evaluate a Georgia PEO

- Aligning PEO Models with Georgia Compliance Rules

- Benchmarking PEO Costs and Benefits in Georgia

- Decoding Contract Red Flags in Georgia PEO Agreements

- Your PEO Negotiation and Implementation Timeline

- Making a Confident PEO Decision in Georgia

Beyond the Quote How to Truly Evaluate a Georgia PEO

Most Georgia buyers start in the wrong place. They compare the per-employee fee, skim the medical plan summary, and assume the rest of the offering is roughly interchangeable. It isn’t. A PEO quote only becomes useful after the buyer separates four things: legal structure, operating model, cost mechanics, and contract exposure.

That matters because a Georgia PEO relationship isn’t just outsourced HR. It’s a co-employment arrangement with tax, insurance, and liability consequences. If the provider is strong, the arrangement can simplify payroll tax reporting, workers’ compensation administration, unemployment filings, and benefits access. If the provider is weak, the buyer inherits confusion at exactly the points a finance team wants control.

A disciplined evaluation usually starts with a short scorecard:

- Legal fit: Does the agreement clearly state who handles payroll taxes, unemployment filings, workers’ compensation claims, and employee relations decisions?

- Financial fit: Is the quote transparent enough to model the actual employer cost, not just the admin fee?

- Service fit: Who answers payroll errors, onboarding issues, claim disputes, and renewal questions?

- Exit fit: Can the company unwind the relationship without disruption to tax accounts, benefits, or payroll continuity?

For staffing-heavy employers, law firms, and companies with mixed exempt and nonexempt populations, recruiting patterns often shape the right PEO structure. Practical hiring and retention context from attorney placement insights can be useful when a company is evaluating whether a PEO’s onboarding and HR support model matches the way it hires.

A buyer also needs a grounded understanding of what’s being purchased in the first place. This overview of PEO benefits meaning is a helpful primer for separating benefits access from the broader co-employment and compliance package.

Practical rule: Don’t advance any PEO to final review until finance, HR, and legal can each answer the same question the same way: what, exactly, is this provider taking off the company’s plate, and what remains with the employer?

Aligning PEO Models with Georgia Compliance Rules

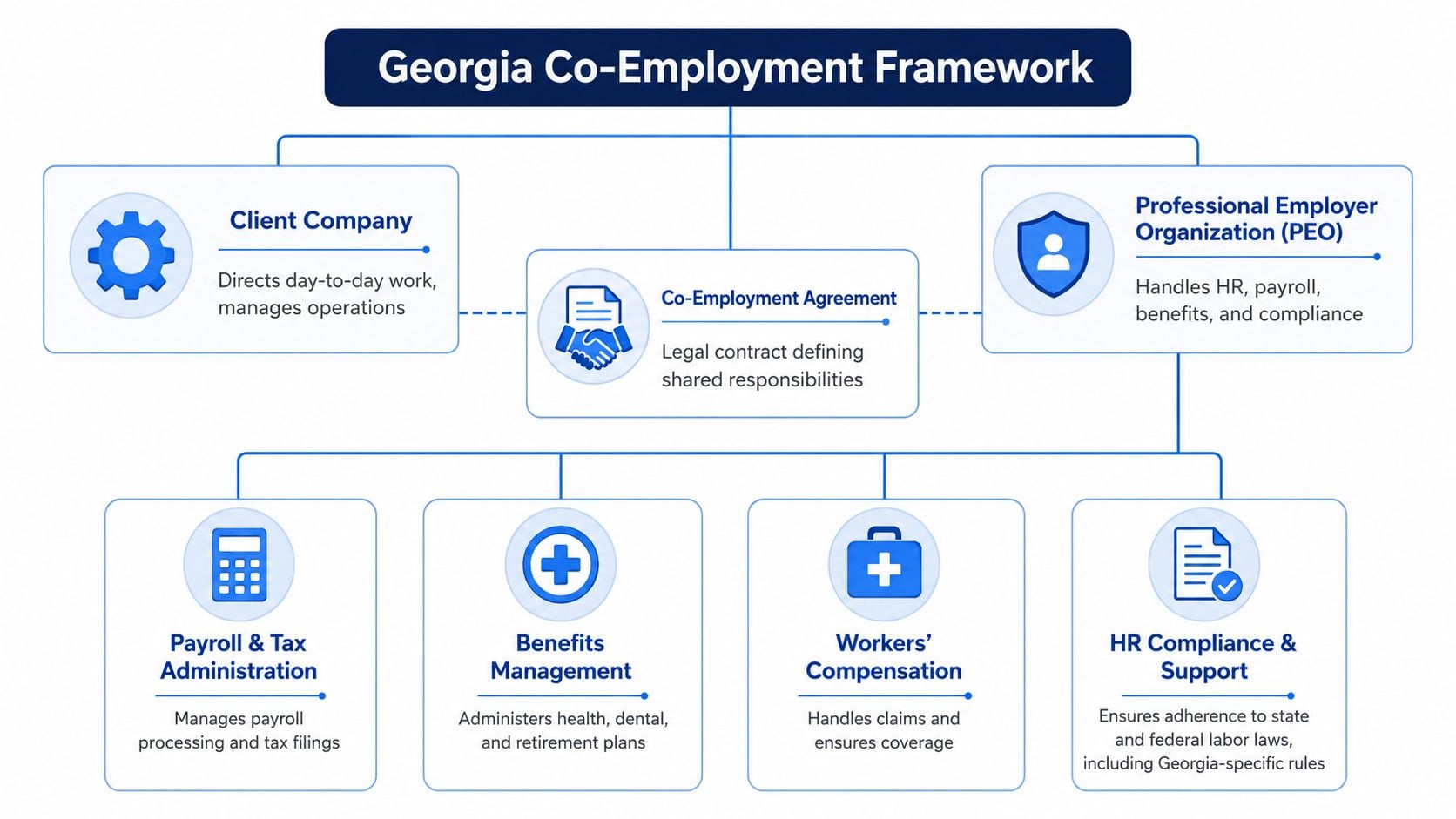

A Georgia CFO usually discovers the PEO risk after the kickoff call. Payroll has already been promised, benefits look competitive, and the sales team says the model is straightforward. Then legal asks a basic question. If a wage claim, tax filing error, or workers’ compensation dispute hits, whose name is on the notice and who fixes it?

That question matters more in Georgia than many first-time buyers expect. Georgia regulates employee leasing and co-employment through statute and administrative rule, and the practical result is simple. A PEO can take on major administrative and reporting functions, but the client company still keeps operational control and still carries exposure for bad management decisions, poor classification, and inconsistent supervisor practices. The Georgia Department of Labor’s Professional Employer Organization law and rules framework is the right place to start if you want the state’s view of how these relationships are structured.

What co-employment means in Georgia

The clean sales version is that the PEO becomes employer of record for certain administrative purposes while the client manages the business. The contract version is more important. You need to see which party handles payroll tax deposits, wage and hour recordkeeping, unemployment filings, workers’ compensation coverage, handbook maintenance, claim response, and termination documentation. If those duties are described vaguely, the ambiguity will show up later as cost, delay, or finger-pointing.

Georgia’s rules also make the benefits side more specific than many buyers realize. Under O.C.G.A. Section 34-7-6 and the state’s administrative rules for employee leasing companies, covered workers may participate in the PEO’s benefit and insurance arrangements, including workers’ compensation and other group plans. That legal structure is what allows a client to enter a master program quickly. It does not guarantee that the program is competitively priced, well administered, or easy to exit.

That last point gets missed. A PEO can improve administration and broaden benefit access. It can also centralize risk in one provider. If the provider mishandles tax filings, carries a weak workers’ compensation program, or has poor claims follow-through, the client inherits the operational fallout even if the contract says the PEO is responsible.

Classification is a separate issue. A PEO can support documentation and process, but it does not rewrite the facts of how your workforce is used. For companies with 1099 contractors, mixed exempt and nonexempt roles, or location-based pay differences, these legal considerations for classifying employees should be reviewed before anyone assumes co-employment reduces that risk.

What to verify before comparing providers

Georgia buyers often waste time asking whether a PEO has a state license in the way an insurer or bank would. That is not the right test. Georgia instead imposes registration, reporting, and financial assurance requirements on covered providers through the state labor framework, including bonding and related filings described by the Georgia Department of Labor’s employee leasing guidance.

Request proof early, and request it in writing.

- Audited financial statements. Finance should review whether the provider has the balance sheet and controls to support payroll funding, tax remittance, and claim administration.

- Bonding or financial assurance documentation. Ask for the current bond evidence or other required filing support, not just a verbal assurance that the provider is compliant in Georgia.

- Workers’ compensation program details. Confirm whether coverage is fully insured or arranged another way, who the carrier is, how claims are reported, and whether your loss history affects renewal pricing.

- Tax filing mechanics. Get the exact workflow for payroll tax deposits, quarterly filings, W-2 processing, unemployment reporting, and notice handling.

- Responsibility matrix. Require a written schedule that shows who owns handbook updates, leave administration, garnishments, I-9 retention, onboarding errors, and employee complaint escalation.

This review is also where cost and compliance meet. A cheaper admin fee can still produce a worse outcome if the provider’s tax operations are thin or its workers’ compensation structure exposes your company to renewal surprises. Finance teams that need a baseline for outsourced HR economics can compare that model against broader HR outsourcing cost ranges and pricing structures, then isolate what is unique to the Georgia PEO arrangement.

Strong providers answer these requests directly. Weak providers redirect to software demos, service slogans, or generic SOC reports that do not answer the Georgia-specific questions. That is usually your signal that the contract needs harder scrutiny before the process goes any further.

Benchmarking PEO Costs and Benefits in Georgia

A CFO gets three Georgia PEO quotes by Friday. All three show lower HR overhead than the current model. All three promise better benefits. Only one will still look attractive after first-year reconciliations, workers’ compensation claims activity, and renewal pricing.

That is the benchmark that matters.

A usable Georgia PEO cost model starts with total employer spend, not the admin line item. The quote usually blends several moving parts into one presentation. To compare providers accurately, break the proposal back into payroll administration, benefits funding, workers’ compensation, tax handling, implementation costs, and any pass-through charges the sales sheet pushed into footnotes.

National market data from the National Association of Professional Employer Organizations shows that businesses using a PEO grow faster, experience lower employee turnover, and are less likely to fail than comparable firms. Those findings are summarized in NAPEO’s research on PEO business outcomes. Useful context, but it does not answer the Georgia buyer’s harder question: which provider structure produces stable cost and lower compliance exposure for this company?

Build the model around Georgia-specific cost risk

Georgia buyers should model at least five cost buckets.

Administrative pricing

Convert percentage-based fees and per-employee-per-month fees into the same annual number. Then test the math against expected headcount changes. A quote that looks cheap at current staffing can become expensive if the vendor uses minimum billing thresholds or reprices after growth stalls.Benefits funding

Rebuild employer cost using your expected enrollment mix, not the provider’s default assumptions. The gap is often material. A rich benefits menu does not help if the medical contribution strategy drives employer cost above your current trend line.Workers’ compensation structure

In Georgia, this deserves a separate review, not a line-item glance. Ask whether the PEO places your employees into a master policy, how claims affect renewal pricing, how audits are handled, and whether your loss experience still influences what you pay. A low service fee can hide an expensive workers’ comp arrangement.Payroll tax and unemployment handling

Confirm how state unemployment insurance is managed and how notices are handled if Georgia issues a rate change, audit question, or wage reporting discrepancy. The process matters because mistakes here create direct cost, management distraction, and sometimes penalties.Implementation and exception charges

Include setup fees, historical data conversion, off-cycle payrolls, year-end correction work, garnishment administration, and custom reporting. These charges rarely decide the sale. They often decide whether the first-year budget holds.

A finance team that wants a broader baseline outside the PEO model can compare the quote against these HR outsourcing cost ranges and pricing structures. That helps isolate what the co-employment arrangement is adding, and what it is merely repackaging.

Sample all-in comparison worksheet

Use a worksheet simple enough to audit. If the model is too abstract, the bad assumptions stay hidden.

| Cost Component | Example PEO Quote | Your Calculation |

|---|---|---|

| Administrative fee | Quoted as percentage of payroll or PEPM | Convert to annual total using current headcount and payroll |

| Medical benefits | Employer contribution assumptions included | Rebuild using actual enrollment expectations |

| Dental and vision | Bundled or separate | Confirm whether voluntary plans still carry admin costs |

| Retirement administration | Included or separate | Identify any recordkeeping or plan admin charges |

| Workers’ compensation | Quoted under PEO master policy | Compare structure, claims handling, and audit assumptions to current program |

| Payroll processing | Included | Confirm off-cycle payroll, corrections, and year-end work |

| Implementation | One-time fee or waived | Add to first-year cost if not contractually waived |

| Miscellaneous pass-throughs | Vaguely described | Require a written schedule of every billable item |

One example. A 50-employee Georgia company with hourly operations, modest turnover, and a mixed claims history can get trapped by the wrong comparison method. Provider A may win on admin fee. Provider B may still be cheaper after you correct the benefits enrollment assumptions, add implementation charges, and stress-test the workers’ compensation pricing methodology for renewal risk.

That is common in Georgia’s mid-market segment, where the spread between quotes often comes less from service efficiency and more from how aggressively the provider underwrites assumptions in year one.

Benefits should be measured in operating terms

The benefit side of the analysis should be tied to operating outcomes, not brochure language.

A stronger medical plan can improve retention in hard-to-staff roles. Better HR process coverage can reduce supervisor time spent on leave questions, onboarding errors, and payroll cleanup. Faster recruiting support can matter if open positions are driving overtime or production delays. Those gains are real only if the provider has a service model that can execute, and only if the contract does not let pricing drift upward before those gains appear.

Companies that are also tightening recruiting and applicant screening workflows should compare that operating spend with broader Investment in hiring workflows. I have seen finance teams approve a PEO based on projected HR savings, then give back part of the savings because hiring process inefficiency remained untouched.

Cost items Georgia buyers miss

The recurring misses are predictable.

- State unemployment treatment. If the proposal is vague on SUI administration, notice handling, or rate change workflow, assume more diligence is needed before you trust the budget.

- Workers’ comp renewal mechanics. Buyers often ask about current pricing and skip the formula that governs year-two cost.

- Pass-through billing language. “Additional services as incurred” is not a pricing term. It is an invitation to ask for a schedule.

- Benefit equivalency claims. “Comparable coverage” needs to be tested against deductibles, employer contribution levels, and participation assumptions.

- Mid-year census changes. Acquisitions, layoffs, and seasonal swings can change pricing faster than the proposal implies.

The right question is simple: what will the company spend over 12 months if hiring, claims, employee elections, and exception processing behave like a normal year in Georgia, not like a sales spreadsheet?

Decoding Contract Red Flags in Georgia PEO Agreements

The sales process encourages buyers to trust the relationship. The contract reveals whether that trust is deserved. In Georgia, that distinction carries real weight because 76,443 employees in the state’s PEO industry are exposed to co-employer liability under Code Section 34-9-11 if the PEO fails its obligations, according to this Georgia legislative reference.

That number should change how a CFO reads the agreement. The buyer isn’t reviewing a routine vendor contract. The buyer is reviewing a co-employment contract that allocates payroll, insurance, tax, and operational risk.

The contract matters more than the demo

A polished implementation team and attractive benefits menu don’t matter much if the agreement lets the provider reprice freely, renew automatically, or shift responsibility back to the client after an error. Many Georgia buyers still assume the biggest risk sits in transition. Often, the bigger risk sits in year two.

A market with fewer provider options also raises the stakes. IBISWorld projects 207 active PEO businesses in Georgia in 2026 and identifies a $3.9 billion state market, while noting a structural decline in vendor availability between 2021 and 2026 in this Georgia PEO industry profile. In a contracting market, weaker contract language becomes more dangerous because the ability to switch diminishes.

The practical takeaway is simple. If a provider knows moving away will be disruptive, the renewal clause becomes a pricing tool.

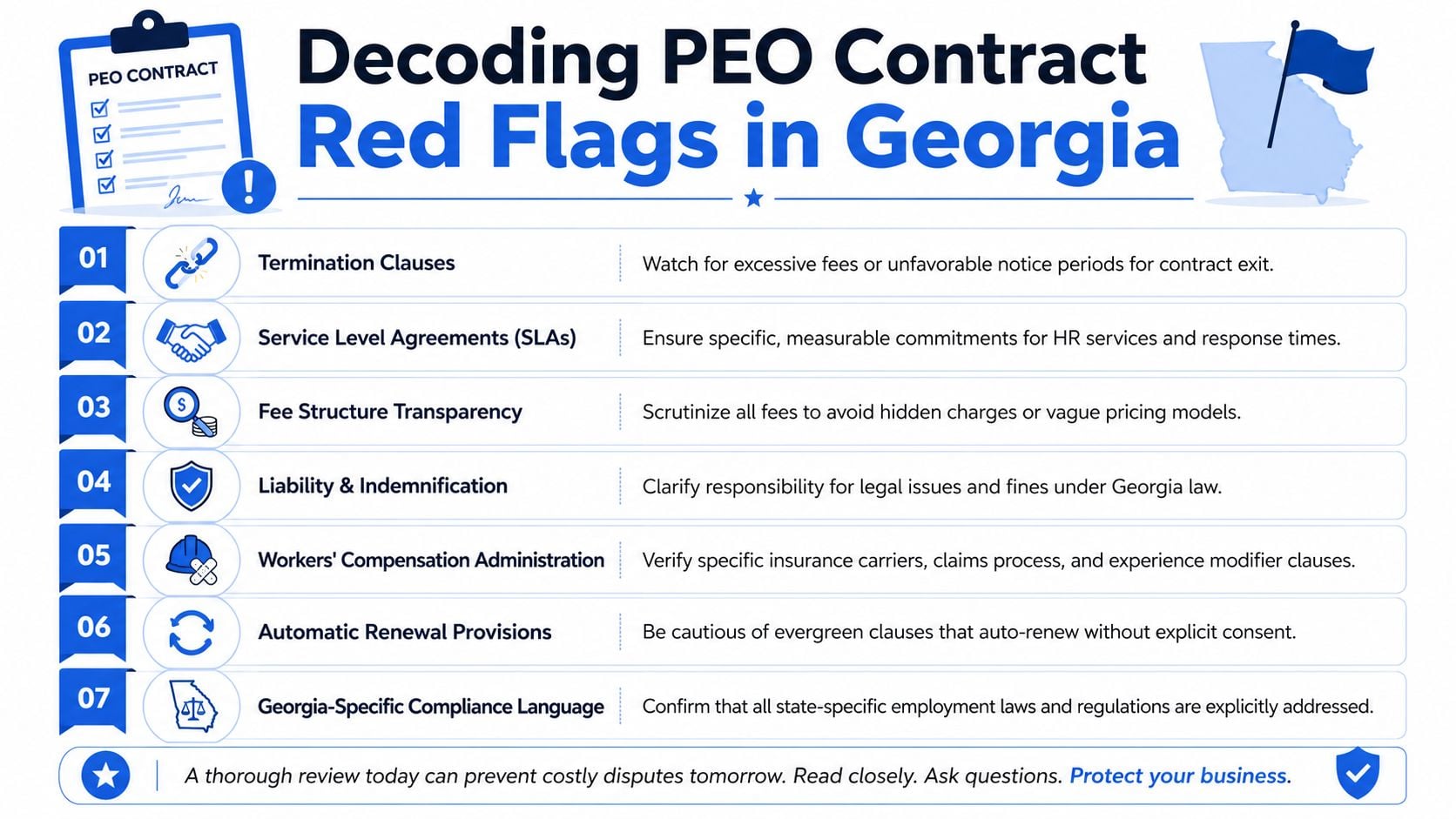

Clauses worth pushing back on

The highest-risk clauses usually appear in plain language, not legal jargon.

Termination language that favors the provider

Watch for long notice periods, vague transition obligations, and open-ended fees tied to implementation recovery, claims runoff, or administrative closeout.Broad pass-through authority

If the contract allows the PEO to pass through benefit or insurance increases without meaningful limits or notice, the buyer’s budget control is weak.Thin service commitments

“Reasonable efforts” is not a service standard. If payroll turnaround, issue response, and dedicated support aren’t defined, enforcement is hard.One-sided indemnification

The agreement should say who pays if payroll taxes are mishandled, if filings are late, or if insurance administration fails. Ambiguity helps the drafter, not the client.Automatic renewal terms

Evergreen language often gets ignored during selection and regretted at renewal.Weak workers’ compensation provisions

Georgia buyers should confirm carrier structure, claims administration responsibility, audit handling, and any language tied to experience modifier outcomes.

A more detailed checklist of PEO contract negotiation red flags is useful during legal review, especially when multiple providers use different pricing structures that make direct comparison harder.

Review the contract as if the relationship has already gone wrong. That’s when the language starts to read clearly.

One more point deserves attention. Some contracts are drafted as if all co-employment risk can be operationally solved. It can’t. Contract language should separate what the PEO controls from what the employer controls. If the agreement blurs that line, disputes become expensive fast.

Your PEO Negotiation and Implementation Timeline

The best negotiation advantage appears after the shortlist is down to two or three viable providers and before the winning provider thinks the decision is final. That’s the point where buyers can improve economics, tighten contract language, and set implementation controls without reopening the entire process.

A useful governance standard already exists. The National Association of Professional Employer Organizations provides a 10-step guideline that requires buyers to verify service competence and confirm that the agreement clearly defines each party’s responsibilities and liabilities, as summarized by the Georgia SBDC discussion of the NAPEO framework.

Days 0 through 30 selection and negotiation

The first month should stay narrow and documented. Buyers who keep too many providers alive for too long usually lose negotiating momentum.

A clean sequence works better:

Days 0 to 15

Final diligence. Confirm financial documents, tax handling, workers’ compensation structure, support model, and contract exceptions.Days 15 to 30

Negotiate the agreement, not just the fee sheet. Buyers should ask for rate stability, implementation concessions, service language, and renewal protections in writing.

The most useful asks in Georgia tend to be practical rather than theatrical:

- Ask for fee clarity: Require a complete billing schedule that lists every standard and nonstandard charge.

- Push on renewals: Ask for defined notice periods and limits on discretionary repricing.

- Address implementation costs: If the provider wants the business, setup fees are often negotiable.

- Write service commitments into the agreement: Verbal promises from sales rarely survive handoff.

A structured operating checklist can help HR and finance stay aligned during this phase. This PEO integration timeline framework is a useful reference for sequencing legal review, data collection, onboarding, and payroll readiness.

Days 30 through 90 implementation and controls

Implementation is where weak providers expose themselves. Not because the platform fails, but because handoffs do. Payroll ownership gets muddled. Employee census data is inconsistent. Open enrollment deadlines collide with payroll conversion.

A disciplined onboarding plan should assign one internal owner for each workstream:

| Workstream | Internal Owner | Key Question |

|---|---|---|

| Payroll migration | Finance or payroll lead | Who validates employee-level data before first run? |

| Benefits enrollment | HR lead | Are plan elections and employer contributions confirmed in writing? |

| Workers’ compensation | Risk, finance, or operations | Who owns claim reporting and policy communication? |

| Tax and filings | Finance | What evidence confirms filings are being made correctly? |

| Manager training | HR or operations | Do supervisors understand what stays in-house? |

The final month should focus on confirmation, not optimism. Run payroll parallel checks where possible. Review employee deductions before the first live payroll. Confirm benefit effective dates. Make sure internal managers know the PEO isn’t taking over day-to-day supervision, performance management, or discipline decisions.

A successful launch happens when employees barely notice the transition and finance can still trace every number.

The strongest implementations feel quiet. The weak ones generate clarifying emails for weeks because no one documented ownership during negotiation.

Making a Confident PEO Decision in Georgia

A Georgia CFO usually gets serious about a PEO after a costly surprise. Payroll tax notices hit the wrong address. A workers’ compensation claim drifts for weeks because no one is sure who owns escalation. Renewal pricing shows up late, after budgets are already set. The decision gets better once the review shifts from demo quality to risk allocation.

Georgia adds a layer many buyers miss. The state does not run a licensing regime for PEOs the way some states do, but professional employer organizations operating here still sit inside a real compliance framework. Georgia law addresses employee leasing and co-employment arrangements, which is why I tell buyers to verify how the provider is structured, what entity is on the contract, and whether the provider can document its financial standing and tax process without delay. The Georgia Department of Revenue and the Georgia Code are better reference points than a sales deck for that review.

Use a final decision filter that finance can defend after signature:

- Entity and compliance check: Is the contracting entity the same one handling payroll, tax filings, and insurance administration in Georgia?

- Responsibility split: Does the agreement clearly state what the PEO handles, what stays with the employer, and where shared responsibility can still create exposure?

- Cost visibility: Can finance trace admin fees, benefit charges, workers’ compensation costs, payroll tax treatment, and renewal triggers without relying on verbal explanations?

- Georgia workers’ compensation process: Who controls carrier placement, claim reporting, return-to-work coordination, and audit response?

- Termination mechanics: What happens to benefits, payroll timing, tax accounts, and claim administration during exit?

- Service model fit: Will your assigned team solve issues fast enough for your headcount, locations, and operating tempo?

One hard truth matters here. A provider that is vague before signature usually stays vague once live.

Buyers who want an outside comparison before committing should review independent professional employer organization reviews and vendor comparisons and then test those claims against the actual service agreement, not the proposal summary.

The best decision in Georgia is rarely the cheapest quote or the broadest benefits package. It is the provider whose contract, operating model, and compliance posture hold up when a tax notice arrives, a claim goes sideways, or your company needs to exit cleanly on a fixed timeline.

PEO decisions are easier when finance, HR, and leadership can compare providers side by side on pricing, benefits, contract terms, and risk. PEO Metrics helps companies evaluate, benchmark, and negotiate PEO options with an independent view of what works, what costs more than it appears, and which contract terms are worth pushing before signing.