A benefits renewal file is sitting open on the CFO’s desktop. HR has three browser tabs full of carrier summaries, one spreadsheet comparing deductibles, and a queue of employee questions about networks, payroll deductions, and whether this year’s plan still covers the same doctors. The broker says the market is tough. Finance wants predictability. Leadership wants better benefits without taking on more overhead.

That’s the moment when many companies start searching for PEO benefits meaning. Not because they want a new acronym, but because the current process isn’t working. They’re tired of buying benefits one plan year at a time, with too little bargaining power and too much administrative drag.

A PEO can solve real problems. It can also create new ones if the buyer only listens to the savings pitch and skips the legal structure, fee mechanics, and renewal language. The difference between a strong PEO decision and a costly mistake usually comes down to contract terms, plan structure, and whether the buyer understands what’s being purchased.

Table of Contents

- Beyond the Annual Renewal Nightmare

- What PEO Benefits Actually Mean

- The Engine Behind PEO Benefits How Co-Employment Works

- A Look at a PEO Benefits Package

- Analyzing the Financial and Compliance Impact

- How to Evaluate a PEO and Negotiate Your Agreement

- Hidden Risks and Common Contract Pitfalls

Beyond the Annual Renewal Nightmare

Most companies don’t start with a philosophical interest in outsourced HR. They start with a renewal problem.

A company with 50 employees or 150 employees often runs into the same wall. The medical renewal comes in high, plan options shrink, employee contributions become harder to justify, and HR spends weeks translating carrier language into something managers and employees can use. Then payroll changes have to be loaded, open enrollment questions pile up, and COBRA, ACA, and deduction accuracy still sit with the employer.

That cycle creates two separate costs. One is obvious and shows up in premiums, fees, and payroll deductions. The other is operational. HR leaders get pulled away from hiring, employee relations, and policy work. Finance leaders lose forecasting confidence because the total cost isn’t just the premium. It’s also the labor spent administering the plan and fixing errors.

Practical rule: If the renewal conversation is focused only on premium rates, the company is probably missing half the cost.

A PEO becomes noteworthy, not merely as a generic HR outsourcing vendor, but rather as a distinct way to buy and operate benefits. The shift matters. A traditional approach usually means the company shops for insurance as a standalone employer. A PEO approach means the company may enter a larger benefits infrastructure with different underwriting dynamics, different compliance support, and different contract obligations.

That distinction is why the phrase PEO benefits meaning matters more than it sounds. For buyers evaluating their first PEO, the key question isn’t “what benefits are included?” It’s “what operating model sits underneath the benefits, who carries which responsibilities, and where can the economics break down?”

What PEO Benefits Actually Mean

The plain-English meaning is this. PEO benefits are not just a menu of insurance products. They are access to a shared benefits platform built on pooled purchasing power.

The easiest way to think about it is a wholesale buying club for employers. A standalone company with a modest employee count usually buys benefits with limited negotiating power. A PEO groups employees from many client companies into a larger pool, and that larger footprint can provide access to plan designs, carrier arrangements, and administrative support that smaller employers often can’t get on their own.

According to Paychex’s explanation of what a PEO is, PEOs provide enterprise-level benefits typically unavailable to small businesses, including health, dental, vision, and life insurance; 401(k) retirement plans; employee assistance programs, and disability insurance, by leveraging collective buying power across hundreds of client companies.

Access is the real benefit

That’s the first mental shift. The benefit isn’t only the insurance card. The benefit is access to infrastructure.

That infrastructure may include:

- Larger-group purchasing advantage: Better negotiating position than a standalone small employer typically has.

- Bundled administration: Benefits administration tied more closely to payroll, onboarding, deductions, and compliance workflows.

- Broader plan ecosystem: Medical, ancillary lines, retirement support, and employee support programs housed in one service model.

For HR directors, that can mean fewer disconnected vendors. For CFOs, it can mean a cleaner view of total employment cost. For business owners, it can mean a more competitive offering in recruiting conversations.

A buyer trying to benchmark whether the offer is strong should compare the PEO package against the current market, not just against the current pain point. A structured employee benefits benchmarking process is what separates a good-looking sales deck from a defensible decision.

What doesn’t count as a real improvement

A polished portal isn’t enough. A longer benefits list isn’t enough either.

If the PEO package adds benefits employees don’t value, narrows provider networks in the company’s main geographies, or shifts too much of the total cost into opaque administrative charges, the employer hasn’t improved the program. It has just moved complexity.

The strongest PEO arrangements improve purchasing position and operating discipline at the same time. If only one of those improves, the deal needs a closer look.

That’s why the phrase PEO benefits meaning should be read strategically. It means buying into a model, not just enrolling in a plan lineup.

The Engine Behind PEO Benefits How Co-Employment Works

The mechanics matter, as they determine whether many buyers either get comfortable or back away.

In a PEO arrangement, the legal structure is commonly called co-employment. That term sounds heavier than it is, but it has real consequences for tax handling, compliance, and benefits administration. In this model, the PEO takes on an employer role for administrative purposes while the client company keeps operational control of the workforce.

Take Command Health’s overview of PEO pros and cons states that in a PEO co-employment arrangement, the PEO becomes the employer of record for tax and compliance purposes, issuing W-2s with its name as the employer while the client company retains control over daily operations, hiring, and termination decisions.

Who controls what

That split is the core of the arrangement.

The client company still decides:

- Who gets hired

- Who gets promoted

- Who gets terminated

- How work is performed

- What compensation philosophy and workforce strategy look like

The PEO typically handles or supports:

- Payroll processing and tax administration

- Benefits enrollment and administration

- Certain compliance workflows

- Workers’ compensation administration

- HR systems and service support

Buyers need precision. “Shared responsibility” sounds fine in a sales call, but it isn’t enough in a contract. The Client Service Agreement should spell out who handles notice requirements, tax filings, claim administration, payroll timing, and benefit eligibility corrections.

A useful way to ground this is to compare the model with two alternatives that often show up in the same evaluation cycle.

PEO vs ASO vs Traditional Broker

| Attribute | PEO (Co-Employment) | ASO (Administrative Services Only) | Traditional Insurance Broker |

|---|---|---|---|

| Legal structure | Co-employment model | No co-employment | No co-employment |

| Employer of record for tax and compliance purposes | PEO | Client company | Client company |

| W-2 issuer | PEO | Client company | Client company |

| Control over daily operations | Client company | Client company | Client company |

| Benefits access model | Shared platform and pooled buying structure | Administrative support only, depending on setup | Carrier placement and renewal support |

| HR scope | Broad HR, payroll, benefits, compliance support | Varies by provider and contract | Primarily benefits advisory |

| Liability allocation | Shared and contract-driven | Mostly retained by client | Mostly retained by client |

| Cost structure | Administrative fee plus benefit costs | Service fee plus separate plan costs | Commission or fee arrangement, plus carrier premiums |

| Best fit | Employers seeking integrated benefits and HR administration | Employers wanting admin support without co-employment | Employers wanting market shopping without broader outsourcing |

An ASO can work well for employers that want support but don’t want co-employment. A broker can work well for employers with internal HR depth and enough scale to negotiate competitively on their own. A PEO tends to fit best when the company wants integrated administration and broader purchasing power, and is comfortable with the legal structure.

A more detailed step-by-step guide to how a PEO works is useful during diligence because it helps legal, HR, and finance review the same model from different angles.

Buyers get into trouble when they compare a PEO only to their current broker. The better comparison is operational. Which model gives the company the best combination of control, cost visibility, and compliance support?

A Look at a PEO Benefits Package

A PEO package usually looks bigger than what a smaller standalone employer is used to seeing. The key question is whether the package is better in substance or just broader on paper.

For a growth-stage company with around 75 employees, the appeal often starts with medical coverage. The company may move from a narrow set of local options to a more extensive selection with stronger network access and cleaner administration. But often, the most significant improvement manifests in the areas related to medical, beyond just the medical plan itself.

What employees usually see

Employees usually notice the visible parts first:

- Medical, dental, and vision options: Sometimes with stronger networks or more plan design choice than the employer previously offered.

- Life and disability insurance: Often easier to implement in a PEO environment than through a fragmented setup.

- 401(k) administration: A more institutional process, usually bundled into broader HR administration.

- Employee support features: EAP access, enrollment tools, and cleaner self-service workflows.

Those visible improvements matter because they influence recruiting and retention. They also reduce the volume of hand-built admin work HR has to do during enrollment and qualifying event changes.

What leadership should look for behind the menu

The overlooked part of PEO benefits meaning is that ancillary benefits can become viable because the platform removes setup friction.

The U.S. Chamber’s guide to Professional Employer Organizations notes that PEOs enrich the overall employee experience by introducing advanced features like Flexible Spending Accounts, Health Savings Accounts, commuter benefits, and employee assistance programs, which are often omitted in traditional small business setups due to high setup costs.

That matters in practice. A company may have wanted to offer FSAs, HSAs, or commuter benefits for years, but delayed because payroll coordination, vendor setup, and enrollment management made the rollout too burdensome.

Before accepting the package as “better,” leadership should compare:

- Provider network fit: Are the main employee geographies covered well?

- Plan design quality: Are deductibles, copays, and out-of-pocket structures aligned with workforce needs?

- Retirement plan usability: Is the plan easy to administer and understand?

- Ancillary adoption value: Are offered extras likely to be used, or are they just brochure filler?

A disciplined PEO medical plan comparison framework helps keep the review grounded in actual employee impact instead of feature count.

Analyzing the Financial and Compliance Impact

At this juncture, many evaluations either become rigorous or drift into sales language.

A PEO can produce a strong financial outcome, but only when the employer measures the full picture. Premium savings alone don’t answer the question. The employer also needs to model the administrative fee, payroll implications, workers’ compensation handling, unemployment tax dynamics, implementation costs, and the internal labor that may no longer be required.

According to Thatch’s summary of PEO insurance economics, businesses utilizing PEO services achieve an average return on investment of 27%, translating to a net gain of $546 for every $2,000 invested in PEO services, as reported by the National Association of Professional Employer Organizations.

That benchmark is useful, but it shouldn’t end the analysis. It should start it.

How to model the real cost

The practical way to evaluate a PEO is to build a side-by-side total cost view.

Include these categories:

- PEO administrative fee: Usually structured as a per-employee-per-month charge or a percentage of payroll. The contract should define the exact method.

- Benefit spend: Medical, dental, vision, life, disability, retirement administration, and any employer contributions.

- Workers’ compensation and unemployment effects: These can materially affect the economics depending on the employer’s current setup.

- Internal labor savings: HR and payroll time that can be redirected or reduced.

- Implementation and exit costs: Setup fees, data conversion work, and any termination charges.

A strong model also asks what happens at renewal. A PEO can negotiate well on the front end and still become expensive if the admin fee escalates without a cap or if pass-through costs are defined loosely.

For retirement-plan-heavy organizations, especially nonprofits with lean back-office teams, there’s a useful adjacent read on how to optimize nonprofit retirement benefits without reducing value. The same discipline applies here. The right question isn’t “is this bundled?” It’s “what does this bundle cost over time, and what work does it eliminate?”

Where compliance value shows up

Compliance support is often undercounted because it doesn’t always show up as a line-item savings number in the proposal.

A PEO arrangement can reduce friction around:

- ACA-related administration

- Benefits eligibility tracking

- Payroll tax handling

- Workers’ compensation administration

- Open enrollment execution

- COBRA and employee notice workflows

Those tasks already cost the employer money. If they stay manual, the company pays in staff time and error risk. If they sit with fragmented vendors, the company pays in coordination failures.

The best financial review treats compliance support as part of total operating cost, not as a free add-on. A more rigorous PEO financial governance review helps finance teams test whether projected savings are real, durable, and contractually protected.

A PEO proposal is financially attractive only when the buyer can explain where the savings come from, what fee terms could offset them, and who owns the downside if assumptions don’t hold.

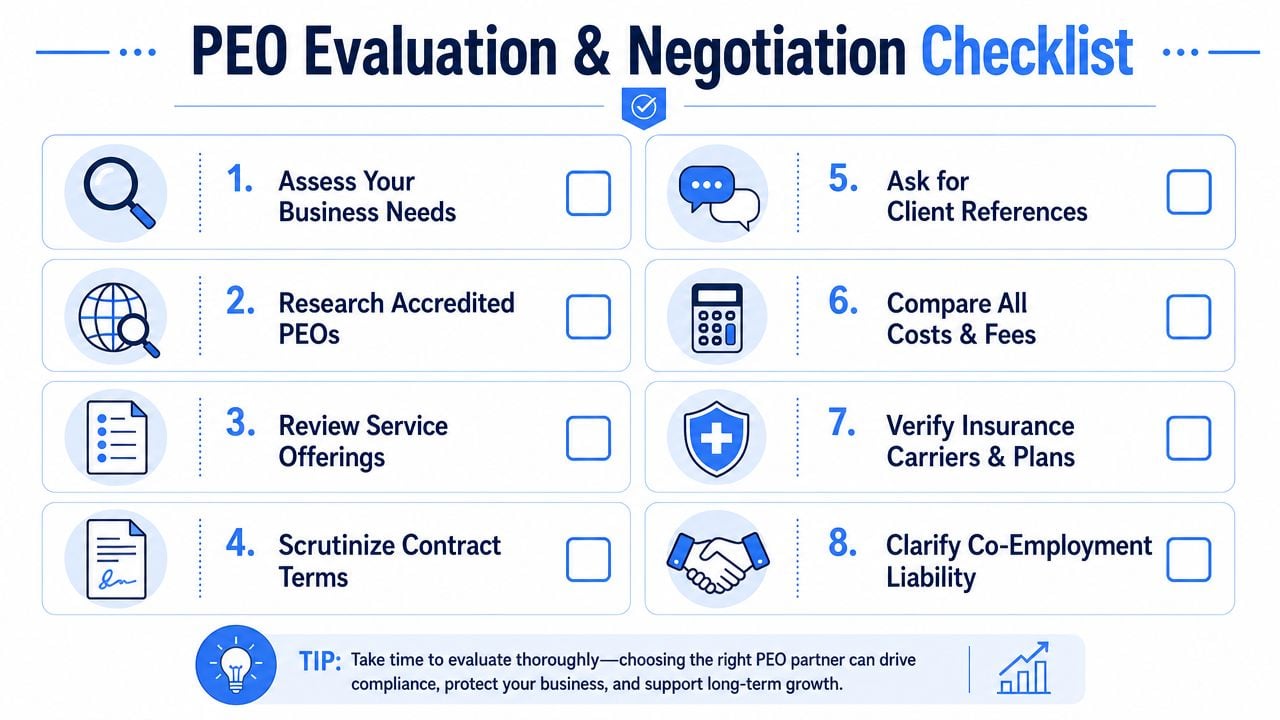

How to Evaluate a PEO and Negotiate Your Agreement

A serious PEO review starts after the demo, not during it.

Most providers can present a solid portal, a broad service menu, and a confident implementation story. The real work is testing the mechanics behind those claims. That means asking for documents, not just decks. It also means involving finance, HR, payroll, legal, and operations early enough that contract language doesn’t get approved by default.

Questions that expose the real offer

These questions tend to surface the trade-offs quickly:

- Ask for renewal mechanics in writing. How are benefit renewals communicated, and what discretion does the provider have to pass through cost changes?

- Request the service model details. Is support handled by a dedicated team or a general service queue?

- Review technology fit early. How will payroll, HRIS, timekeeping, and benefits elections connect with the company’s existing workflows?

- Check carrier and network flexibility. Are employees in all operating states likely to have workable provider access?

- Request implementation accountability. Who owns data migration, deduction setup, and employee communications if errors appear during launch?

A provider that answers these clearly is usually easier to work with after go-live. A provider that keeps responses high-level during diligence usually stays high-level after signature.

Contract terms worth negotiating

The Client Service Agreement deserves line-by-line review. Several terms are commonly negotiable, especially before implementation begins.

Focus on these points:

- Administrative fee increase caps: If the fee can rise at renewal, the cap should be explicit.

- Implementation fee treatment: Ask whether setup charges can be waived, reduced, or credited.

- Termination rights: Clarify notice periods, post-termination responsibilities, and any transition charges.

- Pass-through cost language: Narrow broad definitions that let unexpected charges flow through later.

- Responsibility matrix: Spell out who handles taxes, notices, filings, claims coordination, and error correction.

A useful companion during review is this explanation of indemnification and related contract issues in PEO agreements, especially for teams that need to translate legal language into operating risk.

One more negotiation point often gets missed. Ask what happens if the implementation timeline slips because of the provider, not the client. If there’s no service accountability around launch timing and setup accuracy, the employer may absorb avoidable disruption with no remedy.

Hidden Risks and Common Contract Pitfalls

The sales pitch usually emphasizes scale, convenience, and cost. The harder conversation is about plan structure and contractual exposure.

Many PEO-sponsored health plans are legally structured as Multiple Employer Welfare Arrangements, or MEWAs. That matters because the legal and underwriting framework can affect compliance scrutiny, renewal dynamics, and coverage continuity if the underlying arrangement runs into trouble. According to this discussion of PEO-sponsored group health plans and MEWA issues, 18% of small businesses switching to PEOs do not review MEWA trust agreements before signing, leading to unexpected benefit gaps.

Why MEWA status matters

A buyer doesn’t need to become a benefits lawyer, but the buyer does need to know whether the offered health plan is operating through a MEWA and what documents govern it.

That review should include:

- Trust and plan documents: Not just the summary deck.

- Renewal and reserve language: Especially where coverage continuity could be affected.

- Underwriting approach: How broader pooled claims experience may influence future pricing.

- Exit transition process: What happens to employees and elections if the employer leaves.

CSA language that causes problems

The contract language that creates expensive surprises is often ordinary-looking.

Red flags include:

- “Pass-through costs” with vague definitions

- Automatic renewal terms without meaningful notice protection

- Administrative fee language with no cap

- Unclear allocation of liability between the provider and employer

- Termination clauses that make a clean exit difficult

An employer reviewing these terms should treat the CSA as an operating document, not a procurement formality. The value of the relationship depends as much on the paper as on the platform.

Companies comparing PEOs, renegotiating a renewal, or trying to pressure-test a current agreement can get a clearer view through PEO Metrics. The firm helps HR, finance, and leadership teams compare providers side by side, identify cost and contract trade-offs, and negotiate stronger terms before signing.