Most advice on NYC employees health insurance plans is too shallow to help a CFO make a defensible decision. It treats the city’s new premium-free public option as a benchmark to admire, not a market shift to interrogate.

That’s the mistake.

In New York City, benefits strategy isn’t just about premiums anymore. It’s about who carries the risk, how stable that funding is, what trade-offs employees feel at the point of care, and whether an employer wants to absorb administrative complexity or outsource it. For companies with 10 to 2,000 employees, that changes the evaluation of a broker, an ASO setup, and a PEO relationship.

A company that copies headline talking points about “free coverage” will miss the underlying issue. A company that studies funding structure, network design, and enrollment execution will make a better choice.

Table of Contents

- The New NYC Health Insurance Landscape Post-2026

- The Three Ways to Offer Health Insurance in NYC

- Cost vs Control Decoding NYC Benefit Design Trade-Offs

- The Hidden Risk in NYCs Premium-Free Promise

- Implementation and Enrollment Beyond the Basics

- A Decision Framework for NYC Employers

The New NYC Health Insurance Landscape Post-2026

NYC’s benefits market has a new reference point. Starting in 2026, New York City is implementing its most significant employee health insurance overhaul in over 40 years, moving to a self-funded government health insurance-style model intended to save taxpayers an estimated $1 billion annually while preserving premium-free coverage for 750,000 employees, pre-Medicare retirees, and their families, according to this overview of the 2026 NYC employee health insurance overhaul.

That matters well beyond municipal workers.

Private employers in the five boroughs compete in the same labor market. Employees compare what they pay, which doctors they can see, how easy it is to use the plan, and whether the employer looks organized during enrollment. Once the city resets expectations around premium-free coverage and broader access, private employers can’t benchmark benefits the old way.

Why old comparisons fail

A narrow carrier comparison between Aetna, Cigna, Oxford, or UHC misses the structural issue. The smarter question is whether the employer wants a fully insured model, a self-funded model, or a co-employment structure through a PEO.

Those models behave differently when claims rise, when networks shift, and when HR teams need to manage leave, payroll, onboarding, and benefits in one operating system.

Practical rule: In NYC, benefits should be evaluated as a financing and risk decision first, then as a carrier decision.

What CFOs should benchmark now

A finance team reviewing NYC employees health insurance plans should pressure-test four things:

- Funding logic: Is the employer buying fixed premiums, paying claims directly, or joining a broader sponsored pool through a PEO?

- Network reality: Will employees get actual access to the hospitals and physician groups they expect in New York?

- Employee friction: How many care decisions trigger unexpected out-of-pocket costs?

- Administrative load: Can the current HR team manage enrollment, eligibility, payroll deductions, notices, and vendor disputes without creating error risk?

For many growth-stage employers, this market shift also makes broader HR outsourcing trends more relevant. Benefits can’t be separated cleanly from payroll operations, compliance workflows, and employee support anymore.

The market changed, even for employers outside city government

The city’s own health benefits program is a $9.4 billion per year system covering active employees, pre-Medicare retirees, and families, with roughly 70% of the covered population made up of active employees and retirees under age 65, based on this NYC employee health insurance fact sheet. When a benefits program that large changes structure, the broader market notices.

That doesn’t mean private employers should imitate it. It means they need to understand what employees will compare them against, and where a public plan’s headline value may hide different long-term trade-offs.

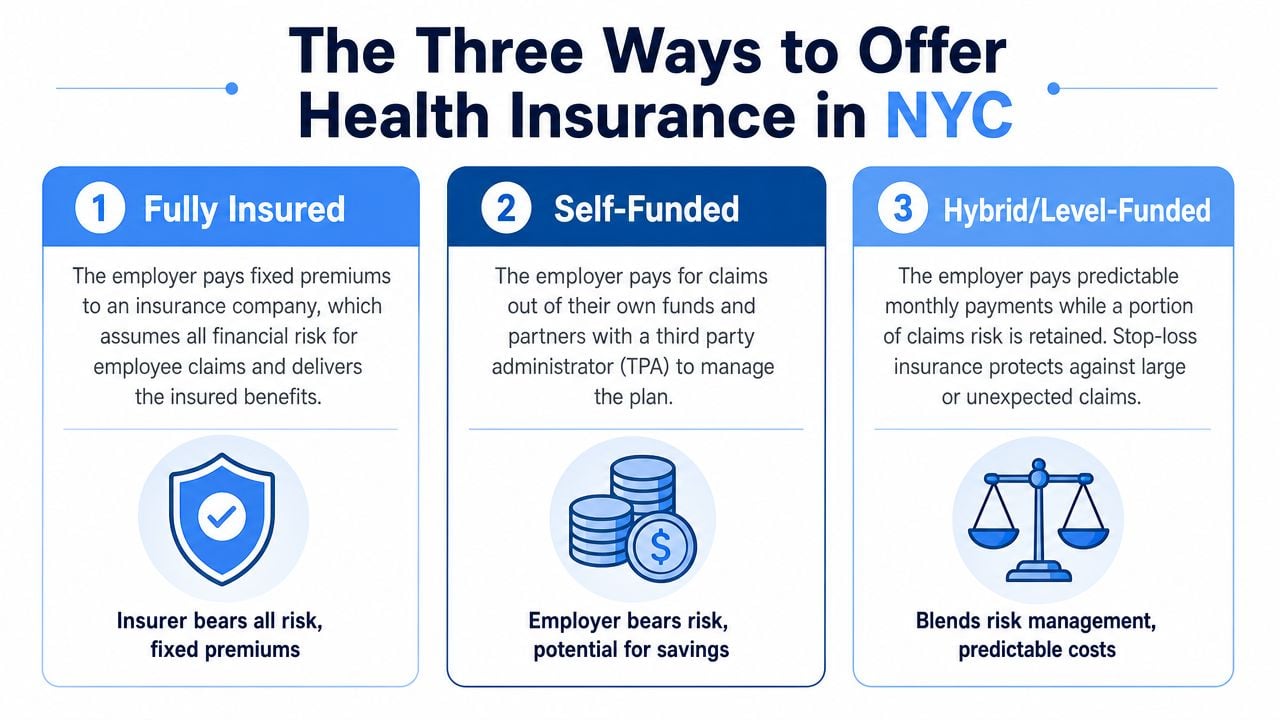

The Three Ways to Offer Health Insurance in NYC

A CFO doesn’t need more carrier brochures. A CFO needs a clean framework.

The three practical ways to offer NYC employees health insurance plans are fully insured, self-funded, and PEO-sponsored. The easiest way to think about them is housing.

- A fully insured plan is like renting a high-end apartment. The monthly bill is predictable, but the landlord sets the rules.

- A self-funded plan is like owning the building. The employer has more control, but also absorbs more exposure.

- A PEO-sponsored plan is closer to joining a large co-op. The employer trades some direct control for pooled buying power, administration, and access to infrastructure it likely couldn’t build alone.

Fully insured plans

This is still the default path for many smaller employers. The carrier sets the premium, owns the claims risk, and gives the employer a cleaner budgeting process.

That simplicity has a cost. Employers usually get less flexibility in plan design, less transparency into what’s driving renewals, and less power to negotiate if the carrier’s network or pricing doesn’t fit the workforce.

A fully insured arrangement tends to work best when the company wants straightforward administration and can tolerate limited customization.

Self-funded plans

Self-funding gives employers more control over plan design, vendor selection, and claims strategy. It can be attractive for organizations with stable cash flow, enough employee volume to spread risk, and leadership that wants deeper visibility into spend drivers.

But self-funding isn’t a cosmetic change. It means the employer takes on claims volatility and needs sharper governance around stop-loss, administration, reporting, and compliance. For finance teams that want a plain-English primer, Liberty Insurance on self-funded programs offers a useful overview of how these structures work.

A self-funded plan can look cheaper in a clean spreadsheet and still be the wrong decision if the employer lacks internal discipline.

PEO-sponsored plans

PEO-sponsored plans sit in a different lane. The employer joins a larger benefits platform and typically gets bundled support across payroll, HR, benefits administration, and compliance. That matters in NYC, where health plan decisions often spill into onboarding, classification, leave management, and payroll execution.

For many employers under mid-market scale, this is the practical middle ground. They may not have the employee count, appetite, or internal team to run an advanced self-funded strategy, but they still want better buying power and a more enhanced employee experience than a basic small-group setup usually provides.

A company comparing an administrative services model against co-employment should review the operational differences in this guide to the difference between a PEO and ASO.

Why this framework matters in NYC now

Effective January 1, 2026, the NYC Health Benefits Program replaced the legacy GHI CBP/Anthem plan with the new NYC Employees PPO, a dual-carrier model with EmblemHealth and UnitedHealthcare that automatically enrolls active employees and pre-Medicare retirees unless they opt out, according to NYC municipal plan transition details from NYCMEA.

That public-sector shift doesn’t tell a private employer which model to choose. It does make one point obvious. Employers need to stop evaluating benefits as a list of plan names and start evaluating them as risk structures with different operational consequences.

Cost vs Control Decoding NYC Benefit Design Trade-Offs

Benefit design gets real when an employee needs care.

A plan can look generous on a summary page and still frustrate employees if costs jump when they choose the “wrong” hospital, urgent care center, or physician group. That’s exactly why CFOs shouldn’t stop at premiums. The hard part is cost-sharing design.

What the NYCE PPO shows about trade-offs

The new NYCE PPO uses a tiered copayment structure. Primary care visits are $0 at select providers and $15 at others, while inpatient hospital care is $0 at H+H facilities and $300 at other participating hospitals, according to the NYCE PPO member site.

That’s not a defect. It’s a design choice.

The city is signaling that it wants members to use certain providers and facilities because those arrangements are more cost-efficient for the plan. Employees still get access to a broader network, but the plan nudges behavior through copays.

How that plays out for employers

For an HR director or CFO, the primary question isn’t whether tiering exists. It’s whether the workforce will tolerate it.

A Manhattan-based office with employees already using preferred health systems may see little friction. A distributed workforce with employees spread across boroughs, Long Island, Westchester, and hybrid home-office schedules may react very differently. If people can’t easily tell which sites are favored, they’ll experience the plan as confusing, not efficient.

Here’s a simple comparison of the design logic:

| Benefit choice | Lower member cost | Higher member cost | What it means |

|---|---|---|---|

| Primary care | $0 at select providers | $15 at others | Network steering starts with routine care |

| Inpatient hospital | $0 at H+H facilities | $300 at other participating hospitals | Hospital selection changes out-of-pocket exposure materially |

| Urgent and virtual care | Lower-cost channels can reduce spend | Non-preferred use can cost more | Convenience and education matter as much as plan design |

Why PEO buyers should pay attention

A PEO won’t erase cost-sharing trade-offs, but it can change them. Some PEO-sponsored plans offer broader national carrier access, different network configurations, or a cost-sharing setup that better fits a company with executives in Manhattan, managers in Brooklyn, and remote staff in New Jersey or Connecticut.

That matters for recruiting and retention. Employees don’t evaluate actuarial logic. They evaluate whether care feels easy, predictable, and fair.

The best plan on paper often loses to the plan employees can actually use without calling HR three times.

For specialized benefit categories, employers should also inspect how a plan handles family-building, maternity support, and related services instead of assuming parity across vendors. Resources like Bornbir’s Progyny doula guide can help HR teams understand the questions employees may ask when a carrier touts enhanced reproductive or maternity-related support.

A disciplined comparison process should test the member experience, not just the premium line; a structured health plan comparison process becomes useful. The most expensive mistake isn’t choosing a pricey plan. It’s choosing a plan that creates hidden friction, then paying for it through employee complaints, exceptions, and off-cycle fixes.

The Hidden Risk in NYCs Premium-Free Promise

“Premium-free” is powerful marketing. It’s also incomplete analysis.

For a CFO, the right question isn’t whether a plan charges employees $0 premiums today. The right question is whether that funding arrangement is durable enough to support benefits stability over the next renewal cycle and beyond.

The real problem underneath the headline

A critical risk in the city’s premium-free NYCE PPO rollout is that the NYC Employee Health Fund has hit zero, creating a $600 million budget hole that threatens future benefit cuts and makes the premium-free promise potentially volatile, as reported in this analysis of the NYC health fund crisis.

That doesn’t mean the plan fails on day one. It means the financing story is under strain.

For private employers benchmarking against city coverage, this creates a trap. If leadership treats “premium-free” as the whole value proposition, it may underestimate how quickly a funding issue can turn into plan changes, cost shifts, narrower practical access, or pressure during future contract cycles.

Why employers should care even if they aren’t in the public plan

Employees compare offers emotionally, not structurally. They hear “free” and assume “better.” Finance leaders need to translate that into a smarter internal discussion.

A company considering a PEO should ask whether a privately sponsored, larger pooled arrangement offers more predictable cost governance than trying to mirror a public-sector promise that may face future pressure. The issue isn’t ideology. It’s stability.

Consider how this plays out in practice:

- Recruiting conversations: Candidates may anchor on low employee contributions and miss the details of copays, network steering, and long-term plan stability.

- Budget planning: A company can underinvest in benefits strategy if it assumes public benchmarks will remain static.

- Renewal negotiations: Employers with weak data and weak negotiating power often react late, after the market has already moved.

Board-level view: A low visible premium doesn’t remove cost. It changes where the cost sits and when the problem surfaces.

Why the PEO model can function as a hedge

For some employers, a PEO-sponsored benefits platform is less about getting a shinier card and more about reducing exposure to abrupt administrative and pricing surprises. That’s especially relevant in NYC, where benefits decisions often collide with payroll deadlines, leave compliance, and employee relations.

A finance team reviewing options should also study the fine print around renewals, fee increases, contribution rules, and service accountability. Many buyers focus only on the medical plan summary and miss the operational risk. Consequently, common PEO benefit plan transparency issues deserve attention.

The takeaway is blunt. Premium-free doesn’t mean risk-free. In NYC, that distinction matters.

Implementation and Enrollment Beyond the Basics

Most enrollment problems aren’t strategic. They’re operational.

The hardest part of NYC employees health insurance plans usually isn’t selecting a plan name. It’s determining who is eligible, how classes of workers are handled, when transitions occur, and whether payroll, benefits administration, and compliance rules stay synchronized.

Where employers get tripped up

Public guidance on the NYCE PPO transition has focused heavily on full-time active staff, leaving groups like 70% of CUNY’s insured adjuncts and part-timers with unclear information about coverage continuity, according to this update on healthcare concerns affecting CUNY employees.

That should get every private employer’s attention.

A mixed workforce creates the same kind of risk. If a company has full-time employees in Manhattan, part-time workers in Queens, remote staff outside the city, and contractors managed by several department heads, benefits administration can break down fast. The problem isn’t just confusion. The problem is inconsistent treatment.

A practical execution checklist

A disciplined HR and finance team should test enrollment and implementation against real employee categories, not an idealized full-time roster.

- Full-time staff: Confirm waiting periods, payroll deduction timing, and carrier effective dates line up.

- Part-time workers: Verify eligibility rules are documented and applied consistently across departments.

- Remote employees: Check whether the network and plan administration still work cleanly for workers outside core NYC geography.

- Leave cases: Make sure payroll, COBRA administration, and benefit continuation rules are coordinated.

- New hires and status changes: Audit how promotions, reduced schedules, and terminations flow into the benefits system.

Why this becomes a PEO discussion

A PEO can earn its keep. Not because it magically simplifies law, but because it centralizes systems and accountability. A company that manages payroll in one tool, benefits in another, and eligibility decisions in email threads is asking for errors.

A stronger operating model usually has three traits:

- One source of truth for employee status

- Clear eligibility workflows tied to payroll

- Named support contacts when exceptions appear

A benefits strategy that works only for standard full-time employees isn’t a strategy. It’s a partial solution.

For employers with a diverse workforce, enrollment shouldn’t be treated as an annual event. It should be treated as an ongoing controls issue. That’s especially true in NYC, where workforce structures are rarely as simple as the org chart suggests.

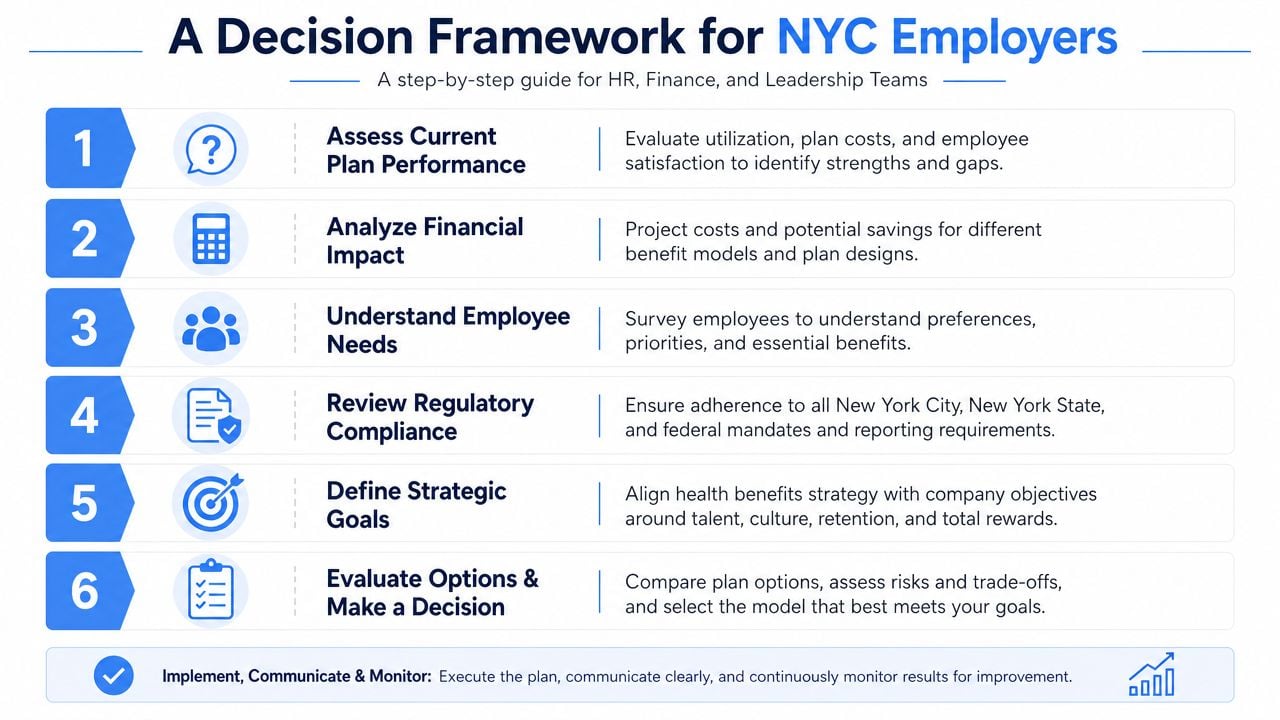

A Decision Framework for NYC Employers

The right benefits model depends less on what sounds generous and more on what the company can support. A 20-person firm, a 150-person multi-state operator, and a 900-person employer with an internal HR team shouldn’t make the same decision.

This framework keeps the discussion grounded.

Six questions leadership should answer

How much cost volatility can the company absorb?

If leadership needs tighter budgeting and fewer moving parts, fully insured or PEO-sponsored arrangements usually fit better than direct self-funding.How much internal administration can HR realistically handle?

A lean HR team shouldn’t pretend it can manage a complex benefits stack the way a large employer can.How important is provider access in New York City?

Employees in NYC care about named systems, physician groups, and convenience. A network that looks broad nationally may still create local frustration.How much employee friction is acceptable?

If a plan relies on aggressive tiering or confusing navigation, HR will end up absorbing the complaints.Does leadership want control or insulation?

Self-funded structures offer more control. PEO arrangements often offer more insulation from day-to-day administration.Is the company buying a plan or buying an operating model?

In many cases, the actual decision isn’t just medical coverage. It’s whether leadership wants help with compliance, payroll, onboarding, and benefits administration under one umbrella.

A simple model-selection lens

| If the company prioritizes | Likely best fit |

|---|---|

| Predictable budgeting and minimal admin | Fully insured |

| Customization and direct financial control | Self-funded |

| Broader infrastructure with outsourced support | PEO-sponsored |

A company evaluating outsourced support should study how professional employer organization health insurance works before assuming it’s just “benefits through payroll.” It’s usually a broader structural decision than that.

The clearest takeaway

Leadership should make this choice with Finance, HR, and operations in the same room. If one group picks the cheapest-looking option without pressure-testing risk, network fit, implementation burden, and employee experience, the company will pay later.

The best decision is the one the company can defend at renewal, administer cleanly, and explain clearly to employees.

Companies evaluating a PEO, renegotiating an existing arrangement, or trying to benchmark NYC benefits options against other models can use PEO Metrics to compare providers side by side, identify pricing and contract trade-offs, and approach the decision with sharper understanding instead of relying on sales presentations.