A finance leader is reviewing a PEO renewal. Payroll support looks fine. Workers’ comp pricing is clear enough. Then a line item appears that seems simple: group term life insurance included.

That line is where many buyers stop asking questions.

They shouldn’t. Life insurance inside a PEO can be a useful part of a broader benefits strategy, but it can also hide markups, participation requirements, and contract language that matters only when the company tries to leave. By then, their bargaining power is gone. For an HR director or CFO managing a workforce of 10 to 2,000 employees, the main job isn’t to admire the bundled benefit. It’s to determine whether the coverage is competitively priced, operationally workable, and contractually safe.

Table of Contents

- Evaluating PEO Life Insurance Beyond the Proposal

- How PEO Life Insurance Actually Works

- The Real Costs and Eligibility Requirements

- PEO Life Insurance vs Other Sourcing Options

- Key Contract Risks and Compliance Traps

- How to Negotiate and Compare PEO Life Insurance

- Your Checklist for Evaluating PEO Life Plans

Evaluating PEO Life Insurance Beyond the Proposal

A common scenario looks like this. A 75-person company receives two PEO proposals. One highlights a lower admin fee. The other highlights stronger benefits. Both mention life insurance, but neither gives enough detail to tell whether it’s a meaningful employer-paid benefit, a voluntary add-on, or a bundled product carrying extra margin.

That matters because life insurance tends to get waved through as a low-drama line item. Medical gets the scrutiny. Payroll gets the scrutiny. Life insurance often doesn’t, even though it affects employee perception, total benefit cost, and the company’s risk during a PEO exit.

The practical way to evaluate PEO life insurance is to stop treating it as a free extra. It should be reviewed the same way a finance team reviews any bundled service. What is the actual coverage? Who pays for it? Which carrier sits underneath the plan? What happens at renewal? What happens if the company leaves the PEO?

A useful first pass includes four questions:

- Coverage design: Is the plan basic employer-paid life, voluntary supplemental life, AD&D, or some combination?

- Cost visibility: Is the quoted amount a pass-through carrier premium, or is margin embedded in the benefit package?

- Contract control: Can the PEO change carriers or terms during the agreement?

- Exit continuity: Do employees have any conversion option if the master policy ends?

Practical rule: If the proposal describes life insurance in one line, the buyer doesn’t have enough information yet.

That is where a structured PEO benefit markup transparency review becomes useful. The issue usually isn’t whether life insurance exists. The issue is whether the buyer can see the economics and the contract mechanics clearly enough to make a sound decision.

How PEO Life Insurance Actually Works

The mechanics matter because PEO life insurance is not the same as buying a small standalone group plan through a local broker.

The buying-club model behind the policy

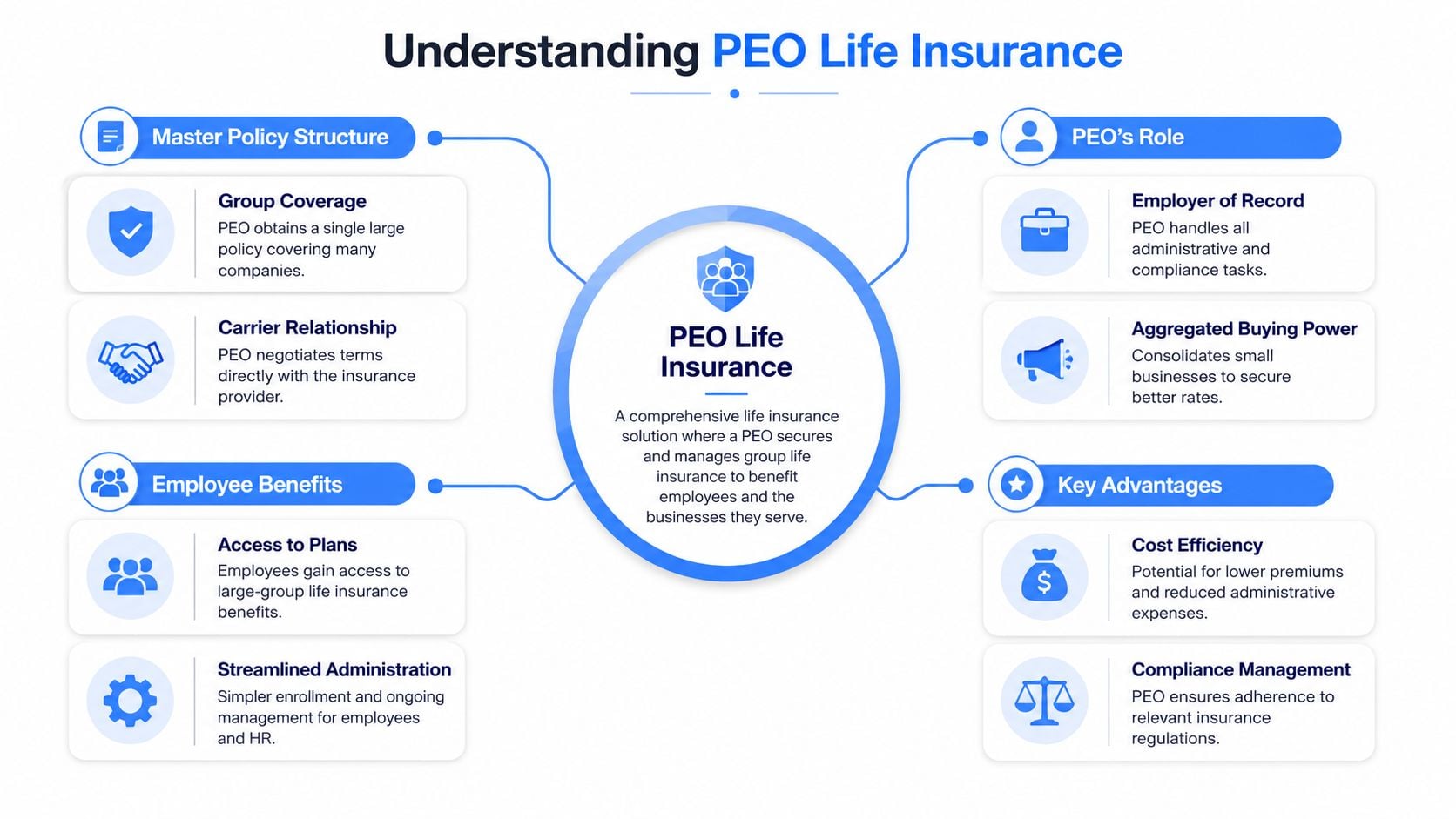

In a PEO structure, the employer enters a co-employment arrangement and the PEO sponsors the benefits plan. Coverage is delivered under a large-group master policy, with the PEO acting as plan sponsor and administrator. That setup lets very small employers, including firms with 2 to 5 employees, access large-employer life and disability benefits that would usually be reserved for much bigger organizations, as described by EESI’s explanation of PEO health plan structure.

The easiest way to think about it is a buying club. One 40-person firm on its own has limited bargaining power and more volatility. Inside a pooled PEO book, that same firm joins a much larger risk pool. The carrier prices the aggregate population, not one small employer in isolation.

That pooling effect is why costs can be steadier. The same EESI explanation notes that aggregating employees across many client companies smooths volatility and helps avoid the 50% premium spikes that can hit a small-group plan when one employee develops a chronic condition. For a CFO, the point isn’t just lower rates. It’s fewer ugly surprises at renewal.

A broader primer on what PEO insurance includes helps frame where life coverage fits inside the full co-employment model.

Buyers often focus on whether the PEO offers life insurance. The sharper question is who controls the master policy and what that means for the employer’s flexibility later.

For companies with employees in California, especially those comparing bundled group coverage with individual options for executives or carve-outs, it can also help to find life insurance for Californians through a local market lens and compare that with the PEO structure.

What coverage usually looks like

Most PEO life setups fall into three buckets.

- Basic life insurance: The employer pays for a base amount of coverage for eligible employees.

- Voluntary life insurance: Employees can elect and pay for additional coverage through payroll deduction.

- AD&D coverage: Accidental death and dismemberment is often packaged alongside basic or voluntary life.

The operational difference is important. Basic life is part of the employer’s spend and benefits philosophy. Voluntary life is often where enrollment, communication, and pricing friction show up. AD&D can look attractive in a proposal summary but may not carry the same value to employees as straightforward life coverage.

What works best is clarity. Employees should know which coverage is automatic, which is elective, and who pays. What does not work is burying those distinctions in a long benefit summary where HR has to untangle them after implementation.

The Real Costs and Eligibility Requirements

A CFO signs off on a PEO proposal because the life insurance line looks inexpensive. Three months later, the finance team realizes the lower premium did not reduce total spend. The savings sat inside a bundled package that also carried admin fees, margin on ancillary benefits, and tighter eligibility rules than the company had been managing before.

What the proposal shows and what it often hides

PEO proposals rarely make life insurance pricing easy to audit. The quote may show a modest employer-paid basic life benefit and a clean per-employee rate, but that does not tell you how much of the charge is carrier premium, how much is administrative load, and how much is margin embedded in the bundle.

That distinction matters. A PEO can offer a competitive life rate and still cost more overall once service fees and bundled benefit charges are added back in. Finance teams that are already reviewing how much it costs to outsource HR should test the life plan the same way. Use all-in cost, not the headline insurance number.

A practical review usually breaks the offer into four pieces:

- Carrier premium: The underlying cost of the life benefit.

- PEO fee: The administrative charge tied to the co-employment platform.

- Employer contribution: What the company pays for basic life, and whether it subsidizes any supplemental tiers.

- Bundled spread: Extra margin that may sit inside ancillary products and never appear as a separate line item.

Buyers are at a disadvantage in negotiations. If the PEO will not show the rate basis, age-banded structure, guaranteed issue limits, and evidence of insurability rules, the company is buying blind. A lower bundled number can still be a worse deal if it limits plan design flexibility or creates renewal exposure the CFO cannot see at signing.

Eligibility rules that disrupt coverage

Eligibility is where inexpensive proposals start to break down in practice.

PEO life plans often require a defined class of eligible employees, such as full-time staff working a minimum number of hours, and they may impose participation standards for employer-paid or voluntary coverage. Those rules are manageable for a stable workforce. They are harder for employers with variable-hour staff, multi-state hiring, acquisitions, or inconsistent HRIS data.

The risk is operational and financial. If employee classifications are wrong, waiting periods are applied inconsistently, or waiver forms are missing, coverage disputes can surface only after a claim. At that point, HR is dealing with a carrier or master policy administrator that will look at the written eligibility rules, not at what the company intended.

Ask for these items before signing:

- The exact definition of an eligible employee

- Waiting periods and effective-date rules

- Participation requirements by coverage type

- Guaranteed issue limits for supplemental life

- Evidence of insurability triggers

- Portability and conversion rights when employees leave

- The PEO’s process if participation drops or census data changes

One more point gets overlooked. If the company expects exceptions for executives, part-time employees, or recently acquired teams, confirm whether the PEO permits those carve-outs under the master arrangement. Many do not, or they price them in a way that erases the apparent savings.

For companies comparing PEO life insurance with broader HR outsourcing options for SMBs, this is often the deciding issue. Cost matters, but eligibility control determines whether the plan will hold up once the workforce changes.

PEO Life Insurance vs Other Sourcing Options

A PEO is one sourcing model, not the default winner. The better choice depends on the company’s size, internal HR capacity, appetite for contract control, and tolerance for renewal volatility.

Where each model wins

A PEO usually wins on administration. Enrollment, payroll deduction, billing, and vendor coordination sit in one operating model. That is especially attractive for lean HR teams or growing companies adding employees across states. The trade-off is reduced control. The employer doesn’t own the benefits architecture in the same way it would under a direct plan.

A traditional broker usually wins on customization. The employer can shape the life benefit more directly and keep the relationship with the carrier market outside a co-employment arrangement. The downside is more internal work and, for smaller groups, more exposure to market swings and limited plan design options.

An ASO model often fits employers that want outsourced administration without fully stepping into a master-policy arrangement. It can preserve more employer control than a PEO, but the company may not get the same pooled purchasing effect on benefits.

A direct-to-carrier approach generally makes more sense for larger employers with enough scale, internal benefits expertise, and appetite for handling more vendor management themselves.

For teams comparing broader HR outsourcing options for SMBs, the life insurance question should sit inside that larger operating model decision, not outside it.

Life Insurance Sourcing Models Compared

| Sourcing Model | Cost Leverage | Admin Burden | Plan Flexibility | Portability Risk |

|---|---|---|---|---|

| PEO | Strong when pooled buying power is real | Low for employer | Moderate | Higher if tied to master policy exit terms |

| Traditional broker | Varies by group size and market access | Moderate to high | High | Lower when employer owns the plan relationship |

| ASO | Moderate | Moderate | Moderate to high | Usually lower than a PEO, depends on plan structure |

| Direct to carrier | Best for employers with scale | High | High | Lower when contract sits directly with employer |

The side-by-side decision often comes down to one hard question. Is the company trying to buy convenience, control, or a mix of both?

A useful comparison point for employers evaluating the difference between a PEO and ASO is who owns the benefits relationship. That single distinction affects pricing visibility, implementation burden, renewal bargaining power, and what happens when the company changes vendors.

The best model isn’t the one with the cleanest proposal. It’s the one whose trade-offs fit the company’s operating reality.

Key Contract Risks and Compliance Traps

Many employers assume life insurance inside a PEO is portable enough. That assumption is often where the risk starts.

The exit problem most proposals ignore

Frequently asked questions about portability and exit risk are still poorly answered in the market. A central issue is whether employees keep life coverage if the employer switches PEOs or exits the co-employment relationship. If the PEO’s master policy terminates, employees may lose coverage unless the employer secured a conversion option, as noted in G&A Partners’ discussion of how insurance works with a PEO.

That is not a minor technicality. It becomes a board-level issue when a company changes providers during a tight renewal cycle, closes an acquisition, or consolidates payroll systems and discovers the life coverage path out of the old PEO was never clearly documented.

The same G&A discussion also notes increased employer scrutiny of exit terms and renewal protections in the 2025–2026 business context. That shouldn’t be read as a quantified market trend. It should be read as a warning sign that buyers are getting more cautious because contract continuity matters.

Clauses worth redlining before signing

The strongest review process usually focuses on contract language, not the marketing deck. Legal and finance teams should look closely at:

- Conversion rights: Is there a written process that allows employees to convert or continue coverage after termination of the PEO relationship?

- Carrier substitution: Can the PEO replace the underlying life carrier mid-term, and if so, what notice is required?

- Renewal discretion: Does the employer have any protection if rates or plan terms change at renewal?

- Eligibility governance: Who is responsible if employee classifications or hours tracking create enrollment errors?

- Termination timing: What happens to active claims or pending elections during implementation or offboarding?

For employers already reviewing related liability exposures, especially in regulated states, resources on employment practices liability for NY employers can be a useful reminder that benefit administration issues rarely stay isolated from broader HR risk.

A PEO contract can look balanced during onboarding and still be one-sided on exit. The difference usually sits in the appendices and insurance exhibits.

What doesn’t work is accepting verbal reassurance that “employees are usually covered.” If the continuity terms aren’t explicit, the employer should assume they are weak.

How to Negotiate and Compare PEO Life Insurance

A CFO gets three PEO proposals that all look close on price. Six months later, one turns out to have higher employee-paid life rates, a carrier change the employer did not expect, and renewal math that was never clear in the first meeting. That is usually not a sourcing failure. It is a comparison failure.

The cleanest way to negotiate PEO life insurance is to stop treating it like a minor add-on. In practice, this coverage is often where bundled pricing gets harder to audit and where vague answers survive longer than they should.

Questions that force transparency

Start with the money flow. Ask the PEO to separate four things in writing: carrier premium, employer contribution, employee-paid deductions, and the PEO’s administrative charge. If those items stay blended together, you are not comparing insurance costs. You are comparing sales presentations.

These questions usually produce useful answers:

- Show the carrier rate sheet: Request the underlying life insurance rates apart from the PEO fee.

- State whether pricing is pass-through or marked up: If the PEO adds margin, ask how it applies to basic life, voluntary life, and AD&D.

- Break out employer-paid and employee-paid costs: A spread on voluntary life comes out of employees’ checks and can affect enrollment and employee relations.

- Identify who controls renewal terms: Confirm whether the PEO, the carrier, or both can reprice the plan at renewal.

- Ask for plan change examples: Have the PEO show what happens if headcount shifts, a class changes, or participation drops.

- Request implementation assumptions: Clarify evidence of insurability rules, guaranteed issue limits, and any waiting period that could affect enrollment.

For a practical framework on how buyers can press for clearer economics across bundled benefits, review this explanation of PEO benefits negotiation strategy and pricing pressure points.

A common mistake is focusing all negotiation energy on the admin fee while accepting vague answers on ancillary benefits. That is where hidden margin often survives.

How to normalize competing proposals

Put every proposal into the same spreadsheet and force the same inputs. If one PEO bundles basic life with AD&D, another lists it separately, and a third mixes insurance charges into a broader benefits line, the apparent price gap is meaningless.

Use a side-by-side process that finance can audit:

- Map the exact life plan design. Note basic life, voluntary life, AD&D, guarantee issue limits, and any age-banded reductions.

- Separate insurance from administration. Keep PEO service fees out of premium comparisons.

- Test employee impact. Compare payroll deductions for the same employee profiles, not just employer cost.

- Review underwriting and participation rules. A cheaper quote loses value fast if enrollment requirements are hard to administer.

- Model renewal exposure. Ask what happens if claims change, headcount drops, or the carrier reprices a class.

- Assign a cost to friction. If HR has to chase exceptions, explain denied enrollments, or clean up deduction errors, that is an operating cost even if it does not show in the quote.

A useful comparison does not stop at premium. It shows where the PEO earns margin, where employees may pay more than expected, and where the employer absorbs avoidable risk.

What works is a disciplined buyer process. Get the same census assumptions, the same plan design, and the same pricing breakdown from every bidder. Then push on the areas that usually stay blurry: employee-paid rates, renewal mechanics, and who profits from the ancillary lines.

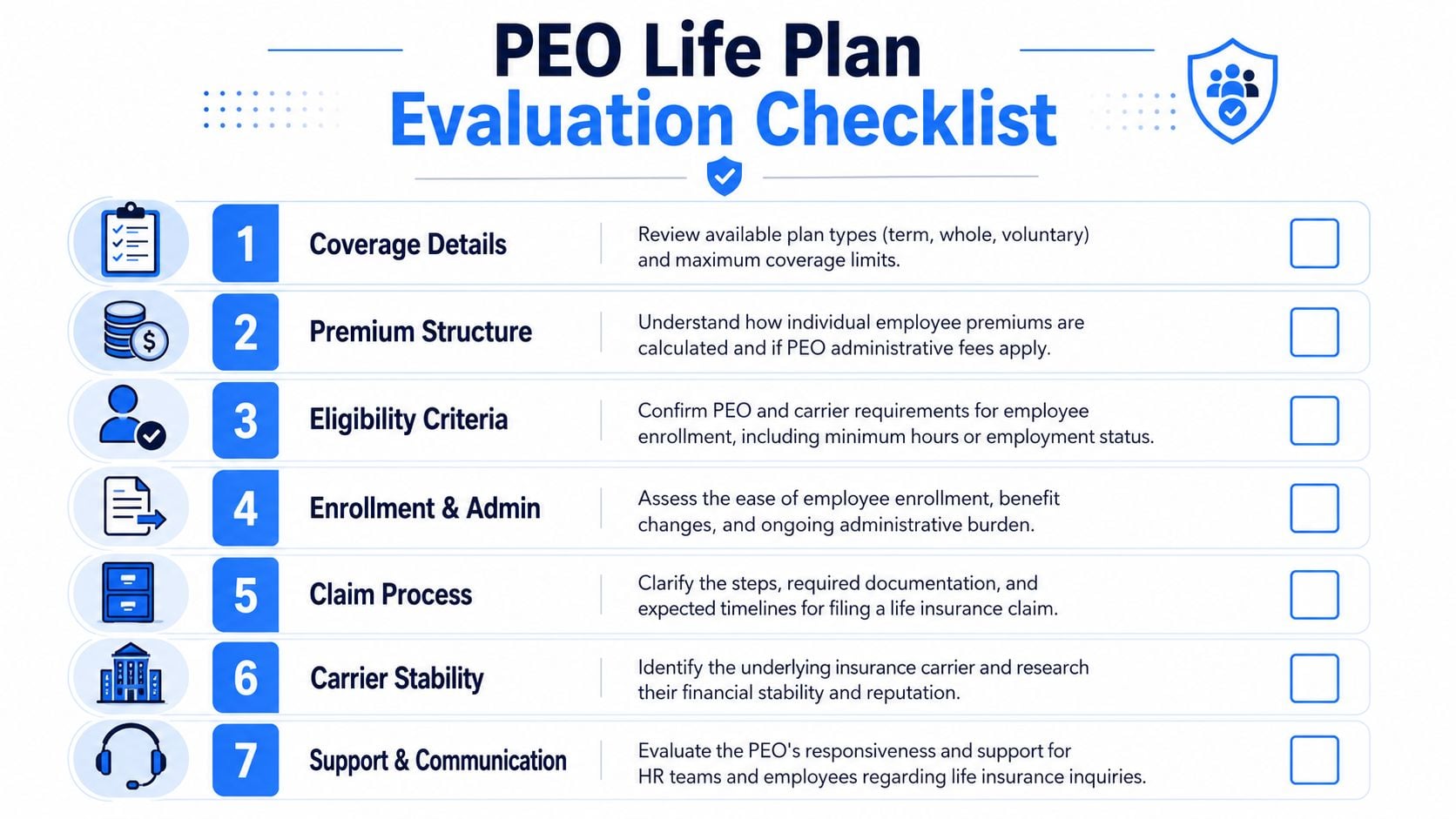

Your Checklist for Evaluating PEO Life Plans

A strong review process is short enough to use and detailed enough to catch the core issues.

Use this checklist before signing or renewing:

- Verify cost transparency: Ask whether life premiums are pass-through or marked up, and separate that from the PEO service fee.

- Confirm plan adequacy: Review the actual coverage tiers, employee elections, and whether the benefit design fits the workforce.

- Check eligibility rules: Make sure HR can administer participation and eligibility requirements consistently.

- Identify the carrier: The employer should know which insurer is underwriting the life plan and whether that can change.

- Review claims support: Confirm who handles employee questions, beneficiary changes, and claim coordination.

- Redline exit terms: Get written language on conversion options, timing, and continuity during a PEO transition.

- Normalize comparisons: Evaluate every PEO proposal on the same all-in basis before making a decision.

The key takeaway is straightforward. PEO life insurance can be a real advantage, but only when pricing is transparent and exit risk is controlled. If either piece is missing, the bundled convenience isn’t worth much.

PEO buyers who want an independent second look can work with PEO Metrics to compare providers, benchmark pricing, flag contract risks, and negotiate stronger terms before signing or renewing.