Most advice on PEO accreditation is too shallow to help a CFO make a good decision. It treats accreditation like a binary signal. Logo present, risk handled. Logo absent, move on. That shortcut misses the underlying issue, which is what liability shifts, what liability stays put, and what the contract still leaves on the buyer's books.

That matters most when a company has employees in multiple states, an internal HR team that's already stretched, or a board that expects tighter controls around payroll, benefits, and compliance vendors. In those situations, accreditation isn't a marketing badge. It's one layer in a risk framework. Teams that outsource payroll often learn the same lesson from broader vendor reviews: process efficiency matters, but financial accountability and service scope matter more. That's a useful lens in HireAccountants' payroll outsourcing insights, and it applies directly to PEO selection.

A better starting point is this. PEO accreditation is useful, but it's not self-executing. A buyer still has to verify status, read the liability language, and understand where the PEO's protections end. Companies that skip that step often discover the gap only when there's a tax notice, an eligibility error, or a dispute over who pays for the fallout. The same pattern shows up in many provider reviews and compliance checks, especially when buyers don't look past formal credentials and into active oversight, which is why a PEO regulatory scrutiny review belongs in diligence.

Table of Contents

- Why PEO Accreditation Is More Than Just a Badge

- The Two Types of PEO Accreditation That Matter

- What PEO Accreditation Actually Guarantees

- The Fine Print What PEO Accreditation Does Not Cover

- A Buyer's Checklist for Verifying and Evaluating Accreditation

- Using Accreditation to Strengthen Your PEO Decision

Why PEO Accreditation Is More Than Just a Badge

A finance team receives two PEO proposals. One carries an ESAC logo. The other says it has strong controls and long client tenure. The fast decision is to favor the accredited provider and move on. The better decision is to ask what that accreditation proves and whether it aligns with the company's biggest exposures.

That distinction is where most buyers lose precision. PEO accreditation is a signal, not a substitute for due diligence. It can tell a buyer that an outside body has reviewed parts of the PEO's finances, conduct, or tax compliance. It doesn't tell the buyer whether the service model is strong, whether implementation will go smoothly, or whether the contract pushes expensive mistakes back to the client.

Practical rule: If accreditation is the only reason a provider looks safe, the buyer hasn't done enough work.

For an HR director, this shows up in execution. A provider can be accredited and still deliver weak escalation support, poor handoffs between payroll and benefits teams, or vague answers about state onboarding. For a CFO, the issue is more direct. A provider can look solid on paper and still leave open questions about indemnification, claim handling, and what happens if taxes, premiums, or contributions aren't remitted as expected.

Three practical takeaways matter at this stage:

- Start with risk, not branding. Ask whether the company is more exposed to payroll tax liability, multi-state compliance friction, benefits administration errors, or service disruption.

- Separate validation from protection. Accreditation may confirm review standards. It doesn't mean every loss scenario is covered.

- Match the credential to the risk. Different PEO credentials address different operational and financial problems.

A buyer who understands that difference will read proposals differently. The badge stops being a closing argument and becomes the opening question.

The Two Types of PEO Accreditation That Matter

Buyers often treat PEO accreditation as one bucket. That is a mistake. ESAC accreditation and IRS CPEO certification address different forms of risk, and a finance team that blurs them can miss the exact liability transfer it thought it was buying.

ESAC accreditation

ESAC accreditation is a private accreditation standard focused on financial controls, reporting discipline, and operating conduct. It matters because a PEO sits in the middle of cash movement. Payroll taxes, benefit premiums, garnishments, and retirement contributions all pass through the provider. If those controls are weak, the client inherits the fallout fast.

The process is not casual. ESAC states that applicants pay a $5,000 application fee as part of the accreditation process, according to the ESAC accreditation process overview. A fee alone proves nothing, but the broader point does matter. Accreditation requires a provider to submit to outside review instead of relying on sales claims about being financially sound.

ESAC also requires a minimum capital position. Under the financial requirements in ESAC's accreditation agreement, an accredited PEO must maintain Adjusted Net Worth of at least $100,000 or 5% of Total Adjusted Liabilities, whichever is greater. For a CFO, that is the practical value. The standard creates a floor under the balance sheet, which matters more when the provider has substantial remittance obligations across multiple client accounts.

That still leaves room for error. A PEO can meet ESAC standards and still disappoint operationally. Claims handling can be slow. State onboarding can be sloppy. Contract language can still leave gray areas around indemnity and client cooperation duties. ESAC helps screen for financial and procedural discipline. It does not replace contract review or reference checks.

The same principle shows up in other compliance-driven vendor decisions. A badge matters only if the underlying controls reduce exposure in a real operating environment, which is also the logic behind this guide to managing driver fatigue legally.

IRS CPEO certification

IRS CPEO certification is narrower and legally more specific. It deals with federal employment tax compliance, not general service quality.

The IRS announced the first wave of certifications in 2017, when it certified 34 Professional Employer Organizations, according to the IRS news release on the initial CPEO certifications. That number mattered because it showed how selective the process was from the start.

For buyers, the primary issue is not prestige. It is tax liability treatment. A CPEO is certified under a federal framework that changes how employment taxes are handled and who is responsible for paying them. That distinction becomes much more important in multi-state operations, where payroll complexity goes up and a single tax process failure can trigger notices in several jurisdictions at once.

Certification also comes with ongoing federal requirements. The IRS requires a CPEO to post a bond and satisfy reporting, background, and suitability standards, as explained in the IRS Certified Professional Employer Organization program materials. Buyers comparing providers should understand the legal and tax mechanics before they compare admin fees, which is why this Certified Professional Employer Organization CPEO guide is worth reviewing early.

A non-certified PEO may still be well run. The point is narrower. It does not offer the same federal tax liability structure as a CPEO.

A side-by-side comparison

| Attribute | ESAC Accreditation | IRS CPEO Certification |

|---|---|---|

| Primary purpose | Financial controls, operating standards, and outside review of business practices | Federal employment tax compliance and liability treatment |

| Overseen by | Employer Services Assurance Corporation | U.S. Internal Revenue Service |

| Main buyer question it helps answer | Does this provider show baseline financial discipline and reporting controls? | How are federal payroll tax obligations handled, and who bears that liability? |

| Review emphasis | Financial submissions, CPA-prepared reporting, conduct standards, capital requirements | Tax compliance, background review, bond requirements, ongoing IRS reporting |

| Best use in diligence | Screening for provider stability and cash-handling discipline | Evaluating federal tax risk transfer |

| What it does not prove | Strong service execution, favorable contract terms, or broad protection against every client loss | Service quality, state tax protection, benefits administration quality, or contract fairness |

The strongest PEO candidates explain these credentials precisely. If a provider answers a tax liability question with an ESAC badge, or answers a financial controls question by saying it is a CPEO, keep digging. That answer usually means the buyer is hearing marketing language instead of risk language.

What PEO Accreditation Actually Guarantees

Accreditation matters only if it changes your risk position after funds leave your account. That is the standard CFOs should use.

What ESAC verifies

ESAC accreditation gives buyers evidence of baseline financial controls and outside review. One practical example is capital strength. The accreditation framework requires a PEO to maintain a minimum level of adjusted net worth tied to its liabilities, which creates a floor under the provider's balance sheet rather than leaving buyers with unsupported claims about financial stability. NAPEO summarizes those accreditation requirements in its overview of PEO financial and reporting standards.

That matters because a PEO is often holding payroll funds, remitting employment taxes, and transmitting benefit payments on a tight cycle. If a provider is thinly capitalized, a shortfall can surface fast. Accreditation does not remove that risk, but it gives the buyer a documented control point and recurring outside scrutiny.

ESAC also signals that the provider is operating under ongoing financial reporting expectations, with CPA involvement and periodic review. In practice, that is useful for screening. It is not enough for approval.

What CPEO status changes in practice

CPEO status has a narrower but more concrete effect. It changes the federal employment tax liability structure.

For a multi-state employer, that distinction is not academic. If a payroll tax issue surfaces with a non-certified provider, the buyer often ends up reading the service agreement, testing indemnity language, and asking whether the provider has both the cash and the willingness to cure the problem. With a CPEO, the federal tax treatment is more defined, which reduces one category of ambiguity during a dispute or audit.

That still leaves exposure around state taxes, wage payment timing, benefits administration errors, and operational mistakes. Buyers often miss that point because the sales narrative blends accreditation, certification, and insurance-like protection into one reassuring package. They are not the same thing.

Finance leaders should also understand what happens when payroll tax responsibility becomes contested. This overview of how the IRS assesses responsible persons is useful background when reviewing contracts, approval workflows, and escalation procedures. It also explains why disciplined buyers ask for stronger reporting packages and clearer PEO financial disclosure requirements before signing.

Where SOC 1 Type 2 fits

SOC 1 Type 2 answers a different diligence question. It addresses whether the provider's controls relevant to user entities' internal control over financial reporting were designed appropriately and tested over time, based on the AICPA trust services and attestation framework described in the AICPA guide to SOC reports.

That is useful if your company depends on the PEO's payroll system, approval chain, user access controls, or change-management process for audit support. A SOC 1 Type 2 report can help your controller, auditor, or lender evaluate whether those controls exist and were tested over a review period.

The trade-off is straightforward. ESAC helps answer whether the provider shows financial discipline. CPEO status addresses a defined slice of federal tax liability. SOC 1 Type 2 helps assess control design and operating effectiveness. None of the three, by itself, guarantees contract fairness, error-free execution, or protection from every loss a client can suffer.

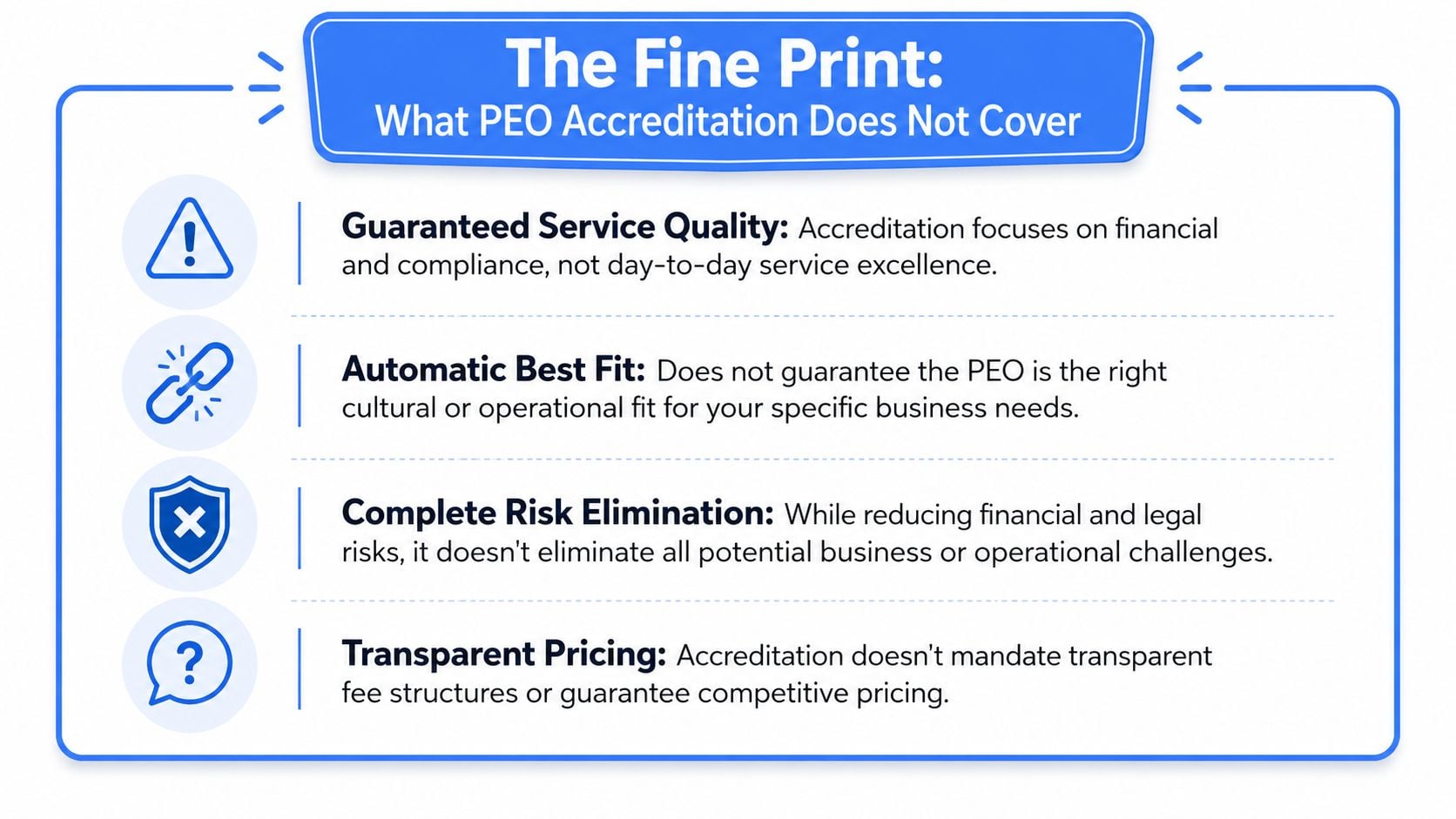

The Fine Print What PEO Accreditation Does Not Cover

The most expensive mistake buyers make is assuming accreditation equals full protection. It doesn't. The main danger isn't that accreditation has no value. The danger is that buyers assign it broader meaning than it carries.

Coverage is narrower than buyers assume

A critical gap in buyer understanding is the scope of ESAC's Client Assurance Program. ESAC's $16 million Client Assurance Program only covers specific liabilities, including payroll taxes, health premiums, and retirement contributions, and not all operational failures or contract breaches, as noted in ADP's explanation of certified PEOs. Buyers frequently assume accreditation guarantees full financial protection. It doesn't.

That single point changes how a proposal should be read. If a PEO says it is accredited, the buyer still has to ask: protected against what, exactly? If the answer stays vague, the buyer should assume the sales narrative is broader than the actual coverage.

Accreditation is strongest as a control against certain financial and compliance failures. It is weak as a blanket promise about every bad outcome in the relationship.

Common gaps that stay with the client

Several important risks usually remain with the employer, even when the PEO is accredited:

- Bad HR advice: If the PEO gives flawed termination guidance and the company ends up defending a wrongful termination claim, accreditation doesn't automatically pay that bill.

- Contract disputes: If the disagreement is about service levels, implementation promises, or performance under the client service agreement, accreditation usually won't resolve the economic damage.

- Pricing opacity: Accreditation doesn't require a provider to present fees in a buyer-friendly format. Admin fees, ancillary charges, implementation costs, and renewal language still need review.

- Operational fit: A provider may be compliant and financially reviewed, yet still be wrong for a business with union exposure, high turnover, multi-entity reporting, or a lean internal payroll team.

Consider a simple scenario. A company changes providers midyear. During onboarding, employee deductions are set incorrectly and a benefits enrollment file goes out with errors. Employees complain, HR spends days cleaning it up, and the employer grants manual corrections and goodwill concessions. That's a real business cost. Accreditation doesn't make the client whole for every hour spent fixing a provider mistake.

The same applies to insurance assumptions. An accredited PEO may carry workers' compensation and other coverage, but a buyer still needs to understand what sits inside the PEO arrangement and what remains outside it. That's why buyers should review what PEO insurance actually includes before they treat accreditation as a complete risk transfer.

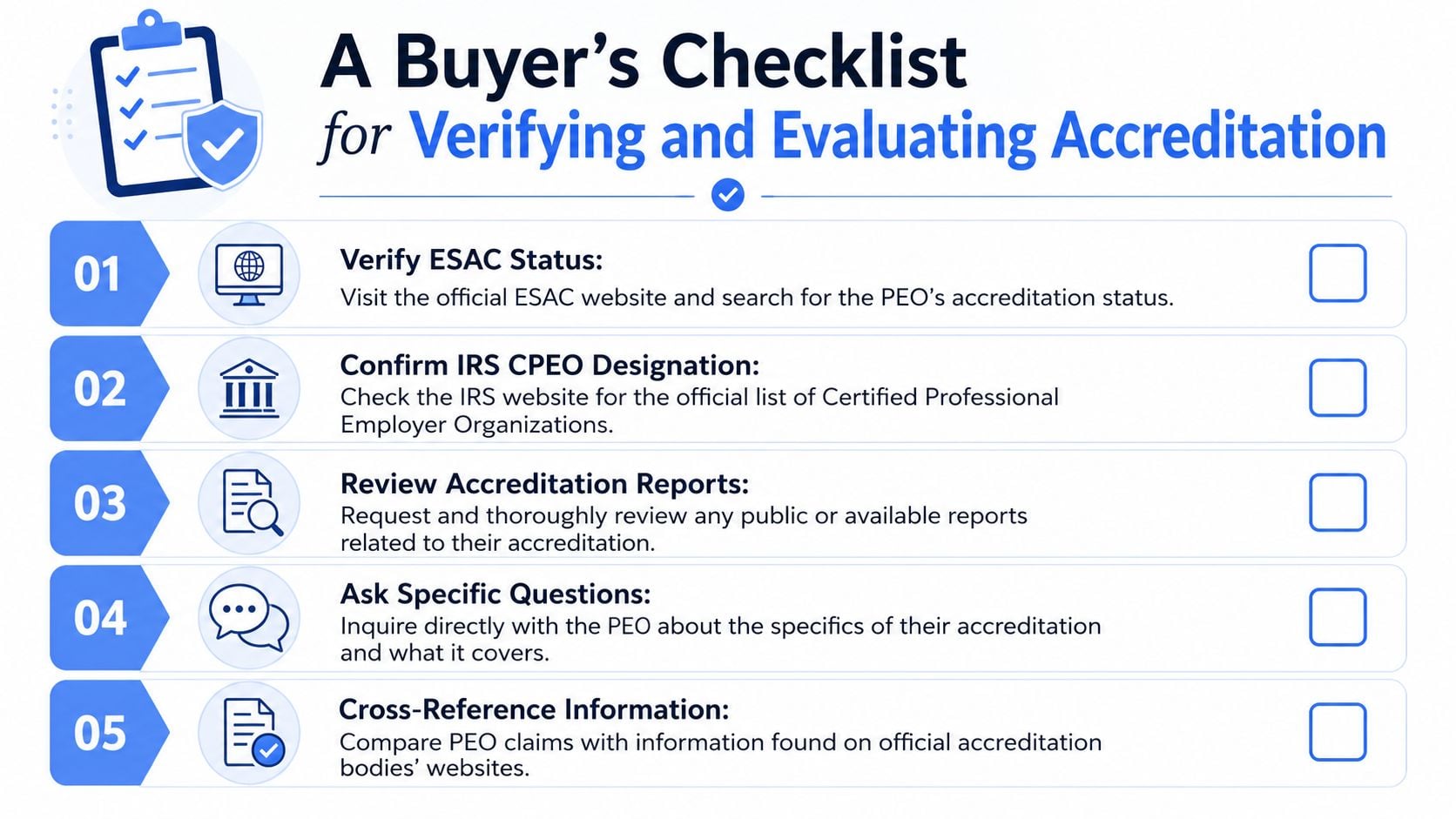

A Buyer's Checklist for Verifying and Evaluating Accreditation

Accreditation review should start before pricing, demos, and implementation plans. If a provider cannot be verified independently, the rest of the diligence process is already on weak footing. For a CFO or controller, the goal is simple. Confirm which entity holds the credential, what that credential covers, and where the liability shifts back to the client company.

Verify status before reviewing the proposal

Start outside the sales process.

- Check current IRS CPEO status: The IRS maintains the official public list of Certified Professional Employer Organizations and states that it updates that list by the 15th day of each month on the IRS CPEO public listings page.

- Confirm ESAC standing directly: Use ESAC's own directory, not a badge image or a statement in a proposal.

- Match the legal entity: The accredited or certified entity name should match the party named in the client service agreement, payroll tax filings, and insurance documents. Large PEO groups often use multiple affiliates, and buyers get into trouble when the marketing brand and the contracting entity are not the same.

- Check for status timing issues: If renewal, suspension, or ownership changes are in play, ask for the effective dates in writing. A provider can describe itself as accredited based on past status while the current contract is being signed by a different entity or during a gap period.

This takes a few minutes and screens out a surprising amount of avoidable risk.

Questions that expose real risk

Good diligence questions force specific answers. Generic assurances are not enough when payroll taxes, benefits remittances, and workers' compensation claims are involved.

- If the provider is ESAC accredited, what losses are covered by the program and what losses sit outside it? Ask for a written answer tied to actual scenarios, such as unremitted payroll taxes, unpaid health premiums, or a client contract dispute.

- If the provider is not a CPEO, who carries the federal employment tax risk if deposits are late or filings are wrong? Contract indemnification may help, but indemnification is only as good as the counterparty's balance sheet and the remedy language.

- Which legal entity signs the agreement, runs payroll, remits taxes, and sponsors benefits? In multi-entity structures, those functions are not always handled by the same company.

- What insurance sits behind the operating model? Ask for policy types, limits, named insured structure, and whether the client company has any direct rights under those policies.

- What is the notice process if payroll taxes, retirement contributions, or insurance premiums are missed or delayed? The primary concern is not whether the provider says it has controls. The issue is how quickly the client is told and what cure steps exist before penalties or coverage problems escalate.

- How is state compliance handled for unemployment, local tax registrations, and workers' compensation across each operating state? Multi-state exposure is where weak operating discipline becomes expensive.

Buyer test: If the answer to a liability question is a story about service quality, ask again. The right answer identifies the responsible entity, the contract language, and the remedy.

For teams formalizing the process, a structured PEO due diligence checklist for buyers helps finance, legal, and HR review the same risks in the same order.

Use accreditation as a multi-state filter

Accreditation matters more once the workforce crosses state lines. Tax registrations multiply. Workers' compensation rules diverge. Leave mandates, wage notice requirements, and payroll timing rules become harder to control. In that setting, accreditation is useful because it gives buyers evidence of baseline oversight. It does not prove the provider is set up well for your specific states, entity structure, or employee mix.

That is the trade-off buyers need to see clearly. A provider with accreditation but weak state-by-state execution can still create penalties, late filings, and cleanup work. A provider without accreditation may still perform well, but the buyer should demand more proof. That usually means tighter contract language, clearer implementation accountability, stronger financial disclosure, and direct answers about who owns compliance tasks in each state.

A practical screening rule works well here. If your company operates in multiple states, treat accreditation as one control in the risk stack, not the whole stack. Verify it. Then test whether the provider's legal entity structure, tax process, insurance model, and notice obligations fit the states where you employ people.

Using Accreditation to Strengthen Your PEO Decision

The strongest use of PEO accreditation isn't as a pass-fail screen. It's as an advantage. Once a buyer understands what the credential does and doesn't mean, the conversation with providers gets sharper.

Treat accreditation as a negotiation tool

If a provider is ESAC accredited but not a CPEO, the buyer has a clear next move. Push harder on federal tax indemnification, notice obligations, and remedy language. If a provider claims strong controls but holds neither credential, ask for more than verbal assurances. Request financial documentation, insurance detail, and tighter service commitments.

A buyer can also use accreditation status to rank implementation risk. A well-credentialed provider may still lose on pricing, service team fit, or contract flexibility. But if two finalists look close, stronger accreditation usually justifies more trust in back-office controls and governance.

How to rank providers more intelligently

There is also a difference between basic accreditation and top-tier credential depth. Only about 1% of all PEOs in the United States currently hold ESAC accreditation, IRS CPEO certification, and Workers' Comp Risk Management certification simultaneously, making these triple-certified providers a rare and highly trusted benchmark in the market, according to Extensis on certified PEO distinctions.

That doesn't mean every buyer needs a triple-certified provider. A single-state professional services firm may not need the same level of risk infrastructure as a multi-state operator with field staff, complex workers' comp exposure, and tight finance controls. But the rarity of that combination is useful. It gives buyers a benchmark for what “best-in-class risk posture” can look like.

The practical takeaway is simple. Treat accreditation as the beginning of diligence, not the end of it. Verify it. Match it to the risk that matters most. Then use it to shape contract terms, provider ranking, and escalation planning.

PEO buyers that want an independent view of pricing, benefits, contract terms, service trade-offs, and liability language can use PEO Metrics to compare providers side by side and negotiate from a stronger position before signing or renewing a PEO agreement.