A project can look fine in the estimate, survive the billing cycle, and still disappoint in the post-job review. Leadership usually blames production, change orders, or field supervision first. Quite often, the leak started earlier, inside payroll.

That happens when labor hours hit the wrong cost code, when a foreman's time lands in the wrong classification, or when a mobile crew's work is processed correctly for pay but incorrectly for job cost. The paycheck goes out. The books close. Then the company uses distorted labor history to judge profitability and price the next bid.

For construction firms, payroll is not a clerical finish line. It is the operating system behind labor cost, compliance, and margin visibility. Companies that want a broader baseline on payroll process design can also compare construction-specific needs against a general payroll guide for UAE companies. The jurisdictions are different, but the useful contrast is this: construction adds layers of project coding, wage rules, and reporting deadlines that generic payroll thinking doesn't solve.

Table of Contents

- Beyond the Paycheck Why Payroll Is a Financial Control

- What Makes Construction Payroll Uniquely Complex

- The Real Costs of Payroll Non-Compliance

- How Accurate Payroll Protects Your Profit Margins

- A Modern Workflow for Construction Payroll

- How to Choose the Right Payroll Solution

Beyond the Paycheck Why Payroll Is a Financial Control

Most leadership teams still treat payroll as a back-office deadline. In construction company payroll, that mindset creates expensive blind spots because labor isn't just an expense category. Labor is the primary input behind job cost, WIP credibility, and bid discipline.

A contractor can pay everyone accurately enough for morale purposes and still run a weak payroll operation financially. That happens when payroll gets processed as a payment event instead of a control system. If field time, project coding, and wage rules aren't aligned before payroll closes, the company records labor cost that looks official but isn't decision-grade.

The practical issue is simple. Payroll feeds too many downstream decisions to tolerate sloppy coding.

Practical rule: If payroll can't explain labor by job, class, and location without cleanup after the run, finance is managing after-the-fact noise, not usable cost data.

For owners and CFOs, the stakes go beyond avoiding a complaint from the field. Accurate payroll supports three decisions that determine financial performance:

- Project review: Leadership needs credible labor cost by job and cost code before deciding whether a superintendent has a production issue or whether the estimate was wrong.

- Bid pricing: Estimators need real labor history, not payroll totals that were cleaned up manually at month-end.

- Risk management: Public work, union obligations, and multi-state exposure all rely on payroll data being right before reports are submitted.

A generic payroll process fails because construction labor moves. Crews change jobs, classifications, and jurisdictions. Pay rates can change within the same pay period. The business doesn't just need net pay. It needs labor intelligence.

That's why strong contractors stop asking whether payroll ran on time and start asking whether payroll produced trustworthy job-cost inputs. Those are very different standards.

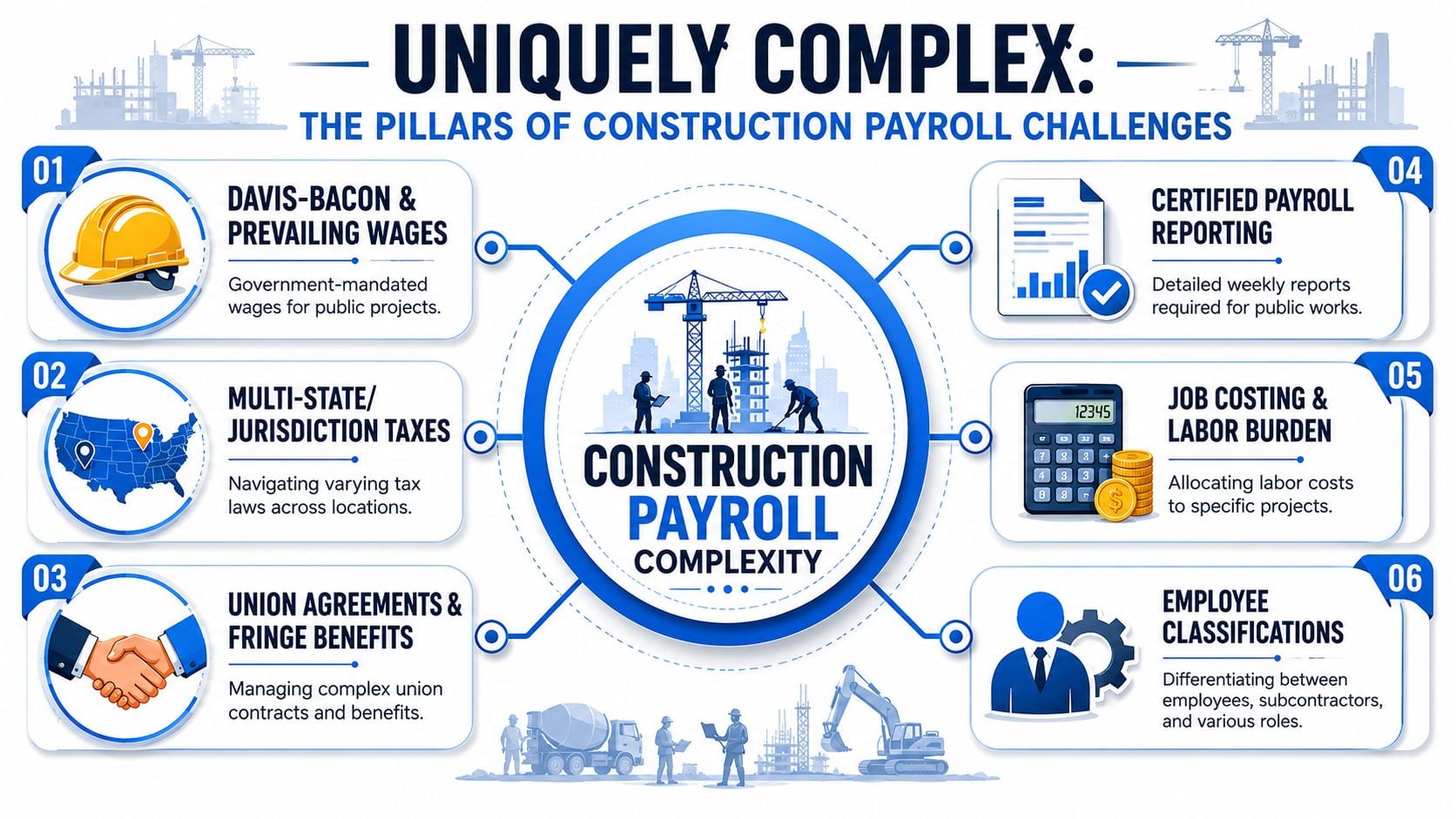

What Makes Construction Payroll Uniquely Complex

Construction payroll isn't ordinary payroll with a few extra fields. It's a job-costing engine, a compliance process, and a labor allocation system running at the same time.

Every hour needs more than an employee name

The core complexity starts with labor distribution. Construction payroll is technically harder than standard payroll because labor must be assigned not only to employees but also to projects, cost codes, and classifications before wages, overtime, taxes, deductions, and fringe benefits are calculated, as explained in this construction payroll reporting overview.

That means one bad timesheet entry creates two problems at once. Payroll can be wrong, and job costing can be wrong. A misclassified carpenter hour doesn't just affect wages. It can distort production reporting, labor burden, and the company's view of whether a phase was profitable.

A clean process usually requires these fields before payroll is released:

| Required input | Why it matters |

|---|---|

| Employee | Identifies pay rules, deductions, and tax setup |

| Job | Places labor cost on the correct project |

| Cost code | Tells operations what activity consumed labor |

| Classification | Supports correct wage treatment and reporting |

| Location | Affects tax treatment and local rule handling |

Companies that still collect handwritten timesheets and then let office staff “figure out the coding later” are choosing rework. They're also creating avoidable arguments between payroll, project management, and accounting.

Public work adds a second clock

Federal public work creates a different type of strain. Payroll has to be right internally, and reporting has to be right externally. Those are separate obligations with separate failure points.

When a company works across classifications and project types, workers' comp coding also becomes part of the discussion. Teams that need a reference point for job-duty mapping often review resources like WC class codes California 2026 while aligning payroll, safety, and insurance classifications. That doesn't replace payroll review, but it helps expose where administrative coding and actual field duties have drifted apart.

A generic payroll platform usually assumes one employee, one rate, one tax profile, one clean reporting path. Construction rarely behaves that way.

Mobile crews break generic payroll setups

The next issue is workforce mobility. Crews move between states, cities, union environments, and project funding types. A worker can spend part of a pay period on private work, part on prevailing wage work, and part under different labor classifications.

That's where many systems fail. They can process pay, but they can't govern complexity. Firms dealing with that mix need payroll controls built around crew mobility, classification changes, and jurisdiction shifts, not just paycheck production. This is the exact governance problem covered in multi-state payroll rules for construction PEO arrangements.

What works in practice is disciplined field capture and constrained data entry. What doesn't work is free-text coding, email approvals, or after-the-fact spreadsheet corrections.

The Real Costs of Payroll Non-Compliance

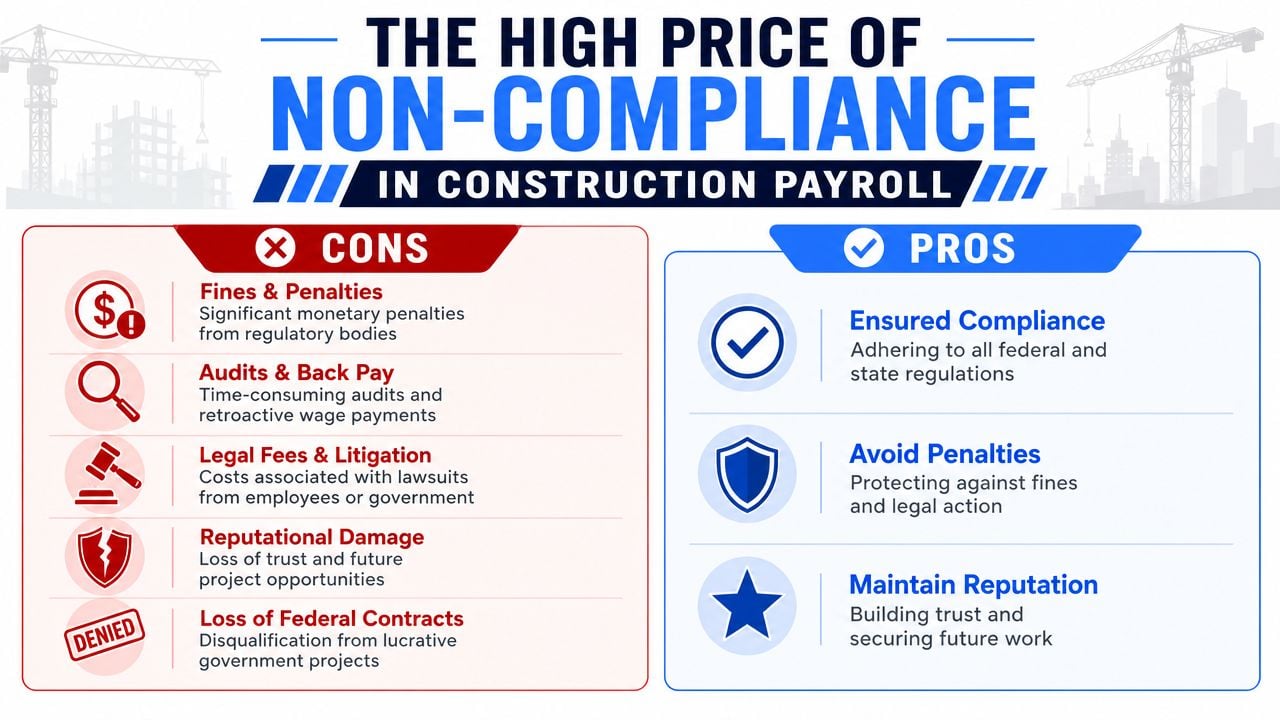

A payroll breakdown rarely starts with a missed paycheck. It starts on a Tuesday afternoon when an owner, agency, or prime contractor asks for labor support by classification and week, and the office has hours, rates, and job codes that do not reconcile. At that point, payroll stops being back-office administration. It becomes a margin problem, a cash-flow problem, and a credibility problem.

Where federal exposure starts

On federally funded work subject to Davis-Bacon and Related Acts, certified payroll is required on qualifying projects, and contractors have to submit weekly WH-347 reporting with the supporting wage, classification, deduction, and fringe information. The reporting package also includes a signed Statement of Compliance, as outlined in this certified payroll guide for Davis-Bacon work.

That requirement changes how leadership should view payroll. The risk is not limited to whether employees were paid. The company also has to prove that time was coded correctly, classifications were applied correctly, and the reporting file can survive scrutiny weeks or months later.

Finance and operations leaders should press on a few points that expose weakness fast:

- Were field hours approved before payroll was calculated?

- Did payroll use the same labor classification that project reporting used?

- Were fringe allocations and deductions documented clearly enough to defend?

- Can the company support the signed compliance statement with underlying records?

Teams reviewing controls or systems should also assess the broader recordkeeping and overtime exposure tied to wage and hour compliance requirements, because a certified payroll issue often leads reviewers into the rest of the labor file.

How non-compliance turns into cost

Penalties get attention because they are easy to see. The larger cost often shows up in slower billing, withheld payments, staff time spent rebuilding records, outside counsel review, and job teams pulled into audits instead of running work.

State enforcement adds another layer. For example, California's Labor Commissioner can impose civil penalties for certain wage statement and payroll record violations, which is one reason multi-jurisdiction contractors need tighter controls before errors spread across a crew, according to the California Department of Industrial Relations payroll records guidance.

The practical problem is spillover. One bad classification can trigger back wages. One weak certified payroll file can trigger a broader document request. One crew working across jurisdictions can turn a single coding error into a pattern that affects multiple employees and pay periods.

I see leadership teams underestimate the internal cost of reconstruction. Once payroll has closed, corrections are no longer simple processing tasks. Someone has to pull foreman notes, compare time entries to job cost reports, confirm rates, trace fringe treatment, and explain inconsistencies to an outside party working on its own deadline.

That work does not create revenue. It protects revenue already earned, and sometimes too late.

Payroll non-compliance is expensive because it forces the company to defend labor data after the operational trail has gone cold.

The trade-off is straightforward. Invest time in approval discipline, coding controls, and record retention before payroll runs, or absorb the higher cost of fixing labor history after an owner, auditor, or agency has started asking questions.

How Accurate Payroll Protects Your Profit Margins

The compliance discussion gets attention because the penalties are visible. The bigger long-term cost is usually hidden. Bad payroll data subtly reshapes how the company measures project performance and prices future work.

Bad payroll data poisons estimating

When payroll coding is wrong, it creates hidden margin leakage in estimating and project profitability. Construction firms operate with variable pay rates and job-based tracking, yet many discussions stop at processing payroll rather than asking how payroll quality changes margin outcomes, as described in this construction payroll challenge analysis.

That is the central financial point. If labor lands in the wrong place, the company learns the wrong lesson from the job.

A few common examples make the pattern clear:

- Crew hours hit the wrong phase: The company thinks framing outperformed and cleanup underperformed. The estimate gets adjusted in the wrong direction.

- Higher-rate labor is miscoded into lower-skill work: The historical unit cost looks better than reality. The next bid comes in too low.

- Traveling labor is processed without clean location coding: Management underestimates what it costs to self-perform work in certain markets.

None of those failures show up as dramatic payroll disasters. Employees may still be paid correctly. The damage shows up later in bid recap meetings, margin fade, and disputes between estimating and operations.

Good payroll data changes management behavior

Strong construction company payroll gives leadership a cleaner way to manage work in progress. It helps answer practical questions that matter:

| Management question | Payroll data needed |

|---|---|

| Which jobs are burning labor faster than planned? | Hours by job and cost code, current pay period |

| Are wage classes aligned with actual work performed? | Classification-level labor detail |

| Should a future bid use in-house labor or subcontract it? | Reliable historical labor cost by activity and location |

A contractor with accurate labor coding can review phase-level performance during the job, not months later during cleanup. That changes behavior. PMs catch overruns earlier. Estimators stop relying on broad assumptions. Finance spends less time reconciling labor after payroll and more time interpreting what the data means.

One useful lens for buyers evaluating payroll partners or PEOs is profitability, not just administration. A provider that improves labor visibility can affect project economics more than one that processes checks. That's the issue behind PEO impact on profitability ratios.

The best payroll process doesn't just produce accurate pay. It produces labor history that estimating can trust.

A Modern Workflow for Construction Payroll

Most payroll failures in construction don't come from one major breakdown. They come from poor handoffs. Field time reaches the office late. Supervisors approve hours without checking classifications. Payroll edits data manually to make the run. Accounting then repairs job costs after the fact.

A modern workflow fixes the handoffs first.

Field capture before payroll entry

The process should start in the field with digital time capture that forces job, cost code, and classification selection before hours are submitted. Tools vary. Some firms use dedicated construction platforms, while others connect mobile time apps to ERP and payroll systems. The technology matters less than the discipline built into it.

What works:

- Required coding at entry: Employees or crew leads must assign hours to the correct job and labor bucket before submission.

- Limited choices: The system should show only valid jobs, codes, and classifications for that worker or crew.

- Daily review: Waiting until payroll day guarantees memory-based corrections.

What doesn't work:

- Paper sheets sent on Friday

- Supervisor text messages as approval

- Office staff rekeying hours from photos

- Catch-all cost codes for “miscellaneous labor”

Approval rules that actually work

Supervisor approval needs to be more than a click. Site leadership should confirm three things before payroll moves forward: the hours were worked, the coding fits the work performed, and any classification or jurisdiction changes are documented.

A practical approval chain often looks like this:

| Step | Owner | Control point |

|---|---|---|

| Time entry | Employee or crew lead | Job and cost code required |

| First review | Foreman or superintendent | Confirms hours and task alignment |

| Payroll review | Payroll or HR | Applies wage, tax, and deduction rules |

| Accounting sync | Finance | Confirms labor posted correctly to jobs |

Companies evaluating support models can compare how payroll workflows connect approvals, system handoffs, and accounting visibility in PEO payroll approval workflow integration.

Payroll and accounting need one version of labor

Once hours are approved, the payroll system should calculate wages and output data that accounting can use without rebuilding the file. It is in this context that integrated construction payroll earns its keep. The company should be able to issue pay, produce compliance outputs where needed, and post labor cost into the accounting structure using the same approved source data.

That means fewer spreadsheets crossing departments and fewer arguments over whose report is “right.” It also shortens month-end because finance isn't trying to reconcile payroll detail that never should have drifted in the first place.

The key design principle is simple. Enter labor once, validate it early, and let every downstream process use that same approved record.

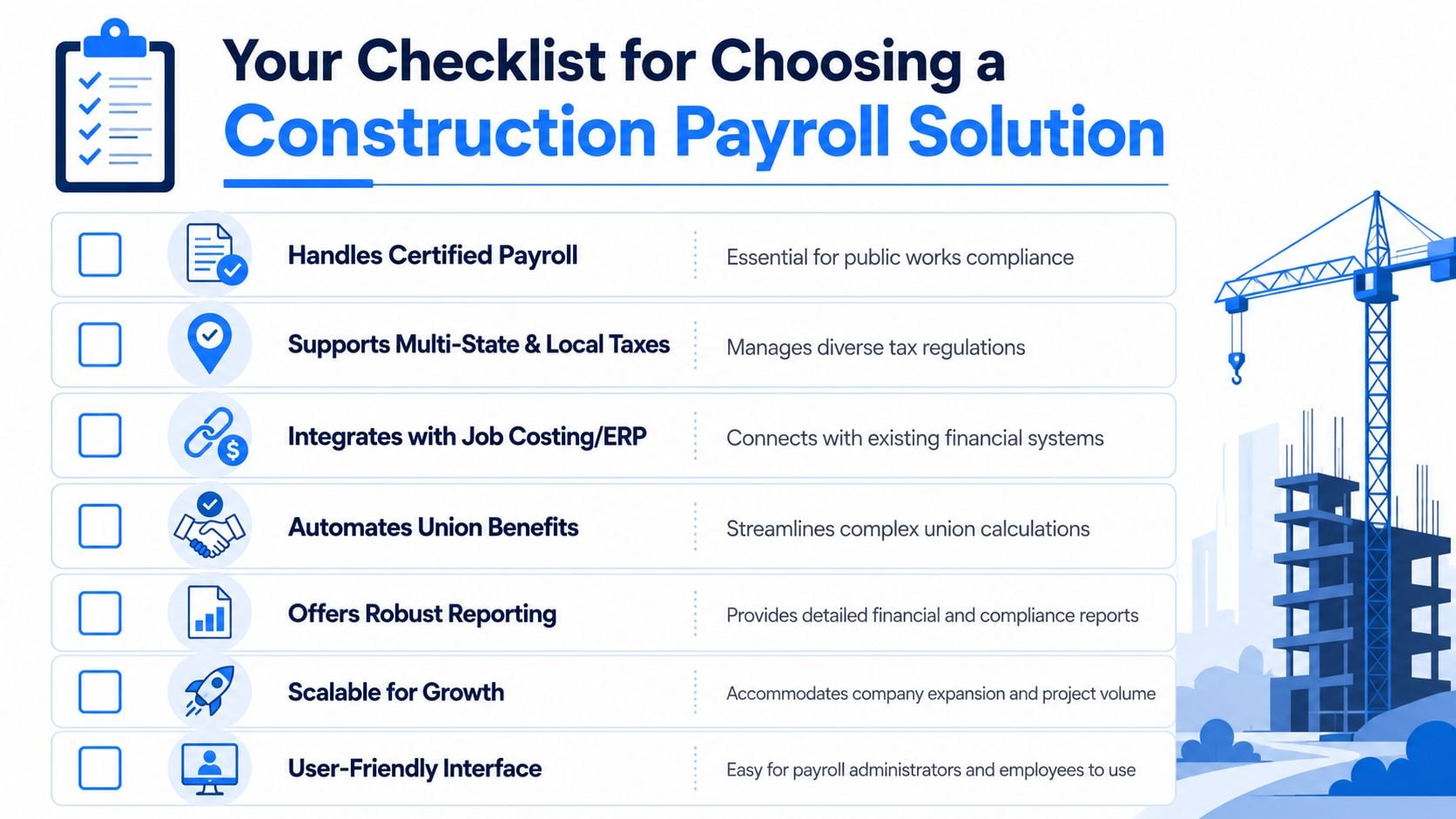

How to Choose the Right Payroll Solution

A payroll platform looks inexpensive until it starts distorting labor cost by job. Then estimating bids from bad history, project managers chase margin they already lost, and finance spends month-end correcting payroll entries that should have posted cleanly the first time.

The right choice starts with the firm's failure point, not the vendor's feature list. Construction companies usually have three paths. Keep payroll in-house with better software, outsource to a construction-focused payroll provider, or use a PEO that bundles payroll with broader employer administration. Price matters, but only after the company is clear on what payroll errors are costing in rework, reporting delays, and bad job-cost data.

Compare options by failure point

Use a simple test. Which problem is hurting financial control today: weak field time capture, compliance-heavy processing, or fragmented HR and payroll administration?

| Option | Best fit | Common weakness |

|---|---|---|

| In-house software | Strong internal payroll staff and disciplined field controls | Heavy dependence on internal expertise |

| Specialist payroll firm | Companies needing construction-specific processing support | Integration gaps with accounting or field systems |

| PEO | Firms that want payroll, HR, and employment administration bundled | Generic PEOs may not handle construction edge cases well |

If foremen are approving incomplete coding, software alone will not fix the process. If labor cost is posting late or landing in suspense accounts, a specialist processor may still leave finance doing manual cleanup. If leadership wants one provider handling payroll, benefits, onboarding, and employer administration, a PEO can make sense, but only if the provider understands mobile crews, union setups, and public works requirements. Buyers comparing those models can use references like what PEO payroll includes to distinguish bundled administration from actual construction fit.

Automation has the same trade-off. It helps when it removes rekeying and preserves approved source data through payroll and accounting. It does not help when it adds another layer that finance still has to reconcile. For teams reviewing back-office workflow more broadly, ReceiptsAI's guide to automation is a useful companion read on where automation improves accounting operations versus where it relocates manual work.

Questions providers should answer without dodging

A serious evaluation should feel like an operating review. Ask the provider to show how work moves from field entry to pay run to job cost reporting, and where exceptions are caught before they hit payroll.

- Show the certified payroll workflow: Ask them to demonstrate how they generate, review, and correct WH-347 reporting.

- Walk through mixed labor on one project: Have them show how the system handles union and non-union labor, or multiple classifications in the same pay period.

- Explain jurisdiction handling: Ask what happens when employees cross state lines or split time between tax locations.

- Prove the accounting handoff: Ask how labor posts back to jobs, phases, cost codes, and the general ledger without manual remapping.

- Clarify exception management: Ask who catches missing coding, late approvals, classification conflicts, and fringe issues before payroll is finalized.

- Show reporting finance can use: Ask for a sample labor report that ties payroll output to job-cost review, not just paystub detail.

That last point matters more than many buyers expect.

A provider can run payroll accurately and still leave the company with poor cost visibility if labor does not map cleanly into the accounting structure. In practice, the best system is the one that lets operations trust job labor reports, lets accounting close faster, and gives estimating a cleaner labor history for the next bid.

Contract terms worth negotiating

Many firms spend all their energy on implementation and leave the operating terms vague. That is expensive later.

Ask for service commitments tied to payroll accuracy, certified payroll turnaround, issue escalation, and reporting support. If those promises matter during the sales process, they should appear in the contract.

Press on these terms before signing:

- Defined responsibilities: Spell out who owns tax setup, wage table maintenance, reporting deadlines, and correction handling.

- Implementation scope: Confirm what data migration, earnings-code setup, and job-cost mapping are included.

- Response times: Set timelines for urgent payroll issues and compliance-related exceptions.

- Renewal protection: Review fee increases, termination timing, and any exit assistance.

- Construction references: Require proof of experience with companies that match the buyer's workforce model and reporting needs.

For firms comparing PEOs specifically, PEO Metrics is one option that provides side-by-side analysis of providers, projected costs, contract terms, and fit by industry and service model.

Companies that are evaluating payroll providers, comparing PEOs, or trying to tighten an existing arrangement can use PEO Metrics to benchmark options, review contract terms, and understand the trade-offs between payroll vendors and PEO models for construction environments.