Searching for employee benefits brokers near me often starts in the wrong place. Employers treat it like a quote chase, compare premiums across a few spreadsheets, then hire the firm with the best presentation and the lowest disruption risk.

That is how companies end up with a weak renewal strategy, sloppy enrollment support, and no real influence with carriers once rates move against them.

A broker influences plan design, contribution strategy, compliance handoffs, employee communication, vendor coordination, and renewal negotiations. For many companies, the financial impact sits close to payroll and workers' comp. The operational impact can be bigger. A poor broker choice usually shows up as higher admin time, more employee confusion, and fewer options when claims run hot.

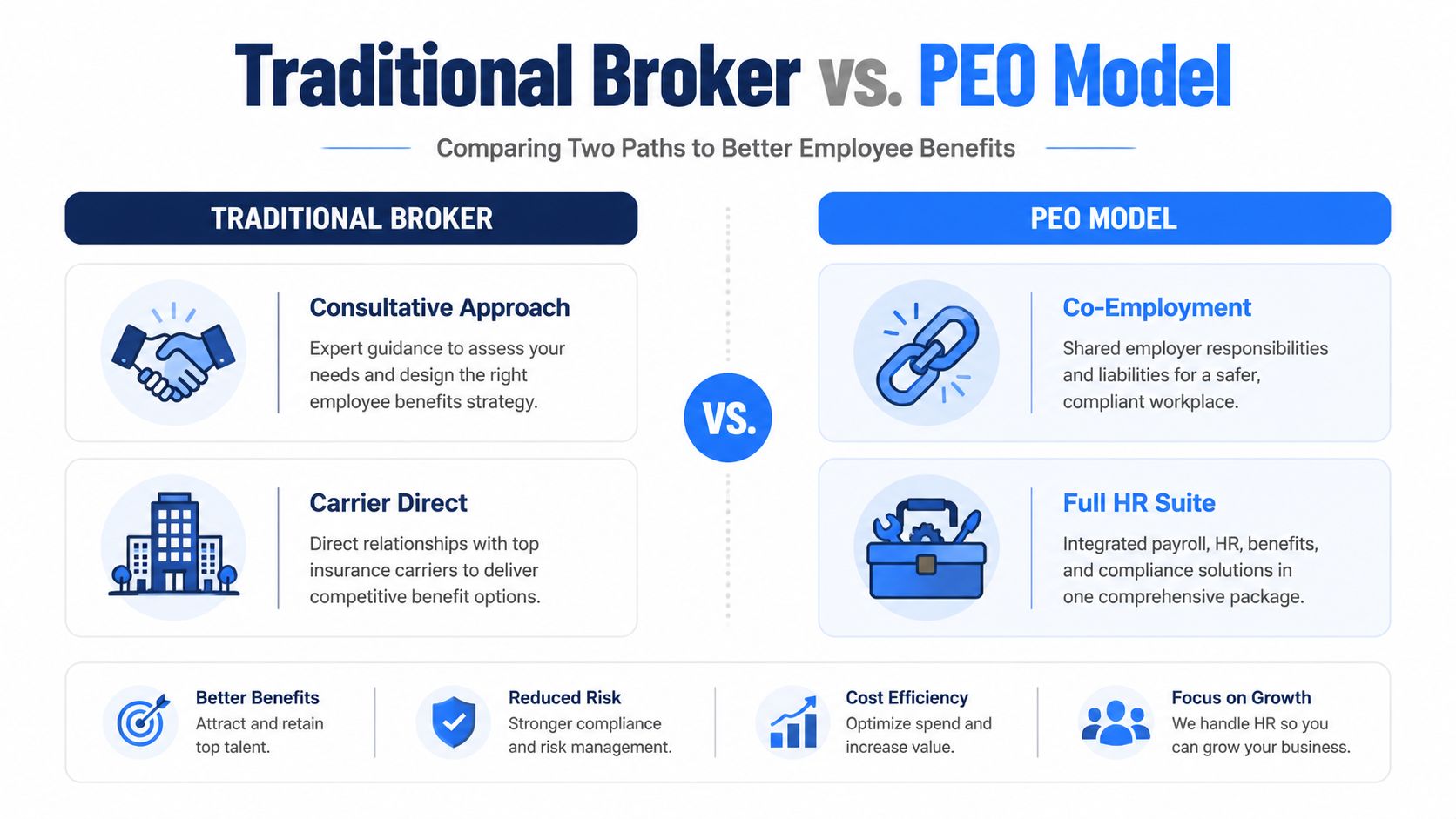

The decision gets harder, and more important, at one point many leadership teams skip. A traditional broker is not always the right model. Some employers are better served by an integrated PEO or ASO arrangement, especially if they need stronger HR infrastructure, better benefits administration, or access to a broader service model. This guide uses a practical framework for that comparison, including when a broker-only approach makes sense and when a PEO plus benefits broker alignment strategy gives you better results.

I have seen companies with 35 employees save time and reduce renewal chaos by moving into a PEO. I have also seen 150-person firms overpay inside a bundled model they had outgrown, where a strong independent broker and a clean ASO setup would have given them more control. The right answer depends on headcount, internal HR capacity, multi-state complexity, turnover, and how much service you require, not how familiar the word "broker" feels.

Table of Contents

- Your Broker Is a Partner Not a Vendor

- Finding Candidates Beyond a Simple Search

- A Data-Driven Vetting and Interview Process

- Decoding Broker Compensation and Total Cost

- Red Flags That Disqualify a Broker

- Is a Broker Even the Right Model for Your Company

Your Broker Is a Partner Not a Vendor

The phrase employee benefits brokers near me makes the search sound local, simple, and transactional. It isn't. A broker isn't office supply procurement. A broker is an outside advisor with direct influence over plan strategy, administration, and employee trust.

That distinction matters because employers often buy on presentation quality instead of operating quality. A polished broker can still give HR a pile of PDFs, weak enrollment support, and vague answers on compliance ownership. A strong broker usually does the opposite. The process feels quieter, but the work is tighter.

What a real partner actually does

A serious broker should help the company answer questions like these:

- Strategy fit: Does the current plan lineup match the workforce, or is it just a recycled package from last year?

- Administration fit: Can payroll, enrollment, eligibility, and reporting move through clean systems without manual patchwork?

- Risk fit: Who owns ACA tracking, notices, documentation, and escalation when something goes wrong?

- Market fit: Is the broker comparing carriers and funding approaches, or just steering the account into familiar placements?

A vendor sells a product. A partner owns outcomes with the employer team.

Practical rule: If the broker spends more time talking about quoting than governance, that's a sales process, not an advisory relationship.

Why the stakes are higher than most buyers assume

A broker decision creates second-order effects. The wrong one doesn't just produce an average renewal. It creates more payroll corrections, more employee confusion, more back-and-forth with carriers, and more internal labor on the HR side.

That's why the broker-versus-platform question matters too. Some employers need a broker plus separate systems. Others need integrated support. Companies sorting through that decision usually benefit from understanding how PEO and benefits broker alignment works before they request proposals.

The central mistake is treating the broker as a vendor to manage. The better framing is this. The employer is selecting a partner that will either reduce complexity or spread it around the organization.

Finding Candidates Beyond a Simple Search

The brokers with the best search rankings aren't always the brokers with the best service teams. Marketing reach and client execution are different skills.

That matters in California in particular. The state's Insurance Brokers & Agencies industry is projected to include 48,255 businesses in 2026, with 132,759 employees, and employment has grown faster than the number of firms, according to IBISWorld's California industry analysis. In plain terms, the market includes both large, scaled brokerages and smaller specialist firms. Buyers need to search deliberately.

Use referral channels that expose service quality

Most good broker referrals come from people who had to live with the broker after the sale.

Start with a short list of peers and advisors:

- CFO contacts: Ask who helped model renewal options clearly and who buried compensation.

- HR leaders: Ask which firms handle open enrollment cleanly and which create ticket volume.

- Employment counsel: Ask which brokers know where their lane ends and when legal review is needed.

- Payroll consultants or HRIS partners: Ask which brokers coordinate well and which create downstream errors.

The useful question isn't “Do you like them?” It's “What breaks under pressure?”

Look in the places general search misses

A local chamber listing or a paid directory won't tell much about broker depth. Better filters come from industry context.

For example, a manufacturer with multiple locations should look for a broker already serving employers with hourly populations, leave complexity, and payroll coordination issues. A professional services firm may need stronger executive benefits strategy and cleaner employee communication. Industry associations and regional employer groups often surface those specialists faster than a generic web search.

A parallel search on PEO options near your business is also smart at this stage. It prevents the team from overcommitting to a broker search before confirming the service model.

Good candidate sourcing doesn't start with “Who is nearby?” It starts with “Who already supports companies that look like this one?”

Use LinkedIn to screen before the first meeting

LinkedIn is one of the quickest ways to remove weak candidates before anyone wastes an hour on an intro call.

Review the actual account team, not just the firm page. Check for:

- Tenure patterns: Is the service team stable, or does the account management bench turn over frequently?

- Client profile clues: Do their posts and recommendations suggest they work with employers of similar size and complexity?

- Functional depth: Is there visible expertise in compliance, analytics, enrollment tech, or only sales leadership?

- Local relevance: Are they active in the employer communities and industries the company operates in?

This process usually produces a shortlist with far fewer surprises. That's the point. A search for employee benefits brokers near me should produce candidates worth evaluating, not just candidates who bought visibility.

A Data-Driven Vetting and Interview Process

Shortlists fail when every finalist gets a different interview and a different standard. The result is predictable. One broker wins because the team liked the presentation style. Another loses because they had a weaker salesperson, even if the underlying operation was better.

That's why the vetting process needs structure. According to Nava Benefits, top employers use a structured methodology that can lead to 20% to 30% better renewal performance, and one of the biggest checkpoints is proving the broker's tech stack instead of accepting vague claims about integrations.

Start with business fit

Before the interview, the employer should define the account itself. That means workforce mix, current pain points, compliance exposure, enrollment process, payroll environment, and decision priorities.

A broker that's excellent for a single-state office employer may be a poor fit for a multi-state operator with variable-hour staff. Buyers should ask each finalist for examples from similar organizations and ask for proof of results in companies of similar size and complexity. If the broker can't show relevant examples or keeps answering in generic language, the process should stop there.

For firms doing deeper diligence on the people involved, especially before handing over sensitive workforce data, it can also be reasonable to perform a digital identity check on key contacts and verify professional consistency across public records and profiles.

Test the operating model

The interview shouldn't focus on “What can you quote?” It should focus on “How do you operate?”

Use questions that force specificity:

- How does the broker run the renewal calendar? Ask for a sample timeline, not a verbal summary.

- What systems feed enrollment, deductions, and compliance reporting? Ask them to show actual workflow, not slides.

- Who owns ACA-related tasks, and where does responsibility shift back to the employer?

- How are carrier issues escalated mid-year? Ask who responds, how fast, and with what documentation.

- What does the service team look like after implementation? Sales coverage isn't service coverage.

A strong broker can answer these cleanly. A weak broker will blur roles, overpromise support, or talk around the details.

The fastest way to expose a shallow broker is to ask what happens in March, not what happens at renewal.

Use a scorecard instead of impressions

A scorecard keeps finance, HR, and leadership aligned. It also helps when the final two candidates are very different.

A practical scorecard often includes these categories:

| Evaluation area | What to look for |

|---|---|

| Strategic advice | Evidence they can shape plan design, not just quote plans |

| Technology | Real integrations, clean reporting, and accountable workflows |

| Compliance support | Clear ownership boundaries and access to capable specialists |

| Service model | Named team, escalation process, and cadence outside renewal |

| Commercial terms | Transparent compensation and documented scope |

| Client fit | Experience with similar size, state footprint, and workforce mix |

The most revealing part of the process is often the demo. A broker should be able to show reporting, enrollment support tools, file handling, and workflow visibility. If the “technology platform” turns out to be a carrier portal plus spreadsheets, that isn't a modern operating model.

A practical interview standard

The cleanest process is to give every finalist the same requirements in advance:

- A sample renewal timeline

- A demo of enrollment and reporting tools

- A written explanation of compensation

- A description of the post-sale service team

- Examples of similar clients or comparable scenarios

- Their approach to payroll, HRIS, and vendor coordination

That creates an apples-to-apples review.

Companies that want a more disciplined approach to vendor scoring can adapt methods from a PEO and HR vendor performance evaluation model. The same logic applies here. Define criteria first, score consistently, then negotiate from evidence rather than personality.

Decoding Broker Compensation and Total Cost

A low broker fee can be the most expensive option on the page.

I see companies fixate on premium discounts or a reduced consulting fee, then ignore the hours HR, payroll, and finance will spend cleaning up the broker's operating gaps. That mistake gets worse when the essential choice is not just broker A versus broker B, but a traditional broker model versus an integrated PEO or ASO setup that shifts administration, compliance support, and service accountability into one system.

What compensation actually tells you

Broker pay signals incentives. It also signals what kind of service model you are buying.

A commission-based broker is paid through carrier placements. That model can work fine, especially for companies that want market access, renewal support, and a service team without a separate consulting invoice. The trade-off is visibility. Employers often struggle to see total broker compensation, carrier-specific incentives, and whether the broker is staffed to handle payroll file issues, billing disputes, eligibility corrections, and employee escalations after open enrollment.

A fee-based broker usually gives finance a cleaner audit trail. The employer can see what advice costs, what work is included, and what falls outside scope. That makes comparison easier. It does not guarantee better outcomes. Some fee-based firms still underdeliver operationally.

The right question is narrower and more useful. Can the firm explain, in writing, how it gets paid, what work that pay covers, and where its incentives could affect recommendations?

What to ask for in writing

Written disclosure should be specific enough that HR and finance would interpret it the same way six months later.

Ask every finalist for:

- All compensation streams: carrier commissions, overrides, consulting fees, technology charges, wellness program fees, and any incentive payments

- A defined scope of work: renewal strategy, employee meetings, open enrollment support, compliance coordination, reporting, vendor management, and issue resolution

- Service limits: what triggers extra fees, what work is excluded, and response-time expectations

- Carrier and vendor relationships: any financial incentives tied to preferred platforms, voluntary products, or specific insurance markets

If a broker stays vague here, expect problems after implementation.

Buyer standard: If your CFO cannot explain the compensation model and service scope in two minutes, the arrangement is too opaque.

Total cost is operating cost plus broker cost

This is the part many companies miss. The broker's compensation is only one line item. The bigger cost often sits inside your team.

A weak broker creates manual work. HR fixes enrollment mistakes. Payroll reconciles bad deductions. Finance chases billing corrections. Managers answer employee questions that should have been handled by the broker or the enrollment platform. None of that shows up as broker compensation, but it is still labor cost.

For a 75 to 150 employee company, even a modest amount of extra admin work adds up fast. Ten hours a month of HR cleanup, five hours of payroll correction, and recurring manager interruptions can erase any savings from a lower broker fee. That is why teams comparing models should review a PEO total cost of ownership analysis, not just premium deltas.

When a broker model makes sense, and when an integrated model is better

A traditional broker model usually fits companies that already have solid internal HR and payroll processes, clean data, and enough in-house capacity to manage vendors. In that setup, the broker is primarily an advisor and market representative.

An integrated PEO or ASO model makes more sense when the company's problem is not only plan selection. It is execution. If eligibility files break, onboarding is inconsistent, ACA tracking is shaky, or HR is one person covering benefits, leave, payroll support, and employee relations, a lower broker fee will not solve the underlying issue. An integrated model often costs more in visible fees and less in hidden labor.

That is the decision point employers skip. They compare broker compensation without deciding whether they need advice, administration, or both.

The better proposals make that distinction clear. They show who owns each task, how service is delivered, and why the compensation model matches the level of support the employer needs.

Red Flags That Disqualify a Broker

Some concerns are fixable. Others should end the conversation.

Too many employers keep weak candidates alive because the broker is responsive during the sales process. That's not enough. Sales responsiveness doesn't predict renewal discipline, data quality, or compliance support.

According to the U.S. Chamber comparison of PEOs and insurance brokers, 48% of businesses choose a broker based primarily on the lowest initial price, a mistake associated with an average 22% renewal increase. The same source notes that outdated broker technology contributes to ACA reporting errors in 50% of level-funded plans. Those are not minor misses. They're operating risks.

Commercial red flags

The first category shows up in proposals and pricing discussions.

- Lowest-price positioning with no multi-year logic: If the pitch is “we'll save money this year” but there's no modeling or renewal strategy, expect problems later.

- Compensation opacity: If the broker won't clearly disclose how they're paid, the employer can't evaluate alignment.

- Black-box recommendations: If they present one preferred option without showing trade-offs or underlying rationale, that's weak advisory work.

- No clear scope boundaries: If nobody can define what support is included after implementation, service disappointments are almost guaranteed.

A credible advisor is comfortable with scrutiny. A weak one redirects it.

Operational red flags

This second category is even more important because it affects daily execution.

- Spreadsheet-heavy administration: If the system depends on emailed census files, manually updated trackers, and PDF enrollment forms, the employer will carry unnecessary admin load.

- Vague compliance ownership: “We help with compliance” is not an answer. The employer needs names, responsibilities, and escalation rules.

- Salesperson-led expertise claims: If every answer depends on one producer and no service team appears, the account is fragile.

- No meaningful payroll or HRIS coordination: Benefits administration doesn't live in isolation. Weak coordination causes errors that spread into deductions, files, and reporting.

A modern broker should be able to show the workflow. If they can only describe it, assume the process is less mature than advertised.

One final red flag is subtle but common. The broker never raises the possibility that a broker may be the wrong model. Advisors who refuse to discuss alternatives are protecting revenue, not helping the client make the best decision.

Is a Broker Even the Right Model for Your Company

This is the question most broker searches never ask. Not “Which broker?” but “Should this company be using a broker-only model at all?”

That gap matters because search results for employee benefits brokers near me rarely explain when a PEO may be the better fit. The broker websites emphasize plans, rates, and service, but they usually don't compare the total operating model against a PEO. Yet for companies with 20 to 200 employees, Greystone Benefits highlights a real decision gap. PEO pricing can become highly competitive with a standalone broker-plus-payroll setup, especially when HR and compliance support are part of the picture.

Broker vs PEO At a Glance

| Criteria | Employee Benefits Broker | Professional Employer Organization (PEO) |

|---|---|---|

| Core role | Advises on benefits and carrier selection | Bundles benefits, payroll, HR support, and compliance administration |

| Carrier flexibility | Usually broader | Often more standardized within the provider's model |

| Employer control | Typically higher on plan design choices | Often more structured and process-driven |

| Administrative burden | Employer usually keeps more internal coordination work | More work is centralized under one operating model |

| Best fit | Employers that want customization and can manage multiple vendors | Employers that want integration, support depth, and simplified administration |

| Common buyer mistake | Assuming a quote comparison is enough | Assuming bundled service always means the best fit |

When each model usually makes sense

A traditional broker often works best when the employer wants higher control over carrier strategy, already has capable HR and payroll infrastructure, and can manage multiple vendors without creating internal drag. Larger employers also tend to have more appetite for specialized arrangements and custom service stacks.

A PEO usually becomes more attractive when the business is growing fast, adding states, running lean internally, or trying to combine benefits, payroll, HR support, and compliance into one accountable structure. That doesn't mean every company should move to a PEO. It means every company should compare the models before assuming a broker is the default.

Some employers land in the middle and evaluate an ASO or hybrid arrangement. That's often worth exploring when the business wants stronger infrastructure without fully changing the employment administration model. A useful starting point is a clear PEO vs HRO comparison, especially for leadership teams trying to separate service scope from marketing labels.

The smartest buyers don't start with loyalty to a model. They start with the operating problems the business needs to solve.

The best takeaway is simple. If a company is searching for employee benefits brokers near me, it should also ask whether the broker model itself still fits the company's size, complexity, and internal bandwidth. That one decision usually matters more than which local firm wins the RFP.

PEO decisions get expensive when buyers compare sales presentations instead of service models, contract terms, and total cost. PEO Metrics helps employers evaluate PEOs side by side, benchmark pricing and benefits, and negotiate stronger terms before they sign or renew.