Most advice on professional employer organization reviews starts in the wrong place. It tells buyers to compare feature lists, browse ratings, and shortlist the names that appear most often on roundup pages. That approach works for software trials. It doesn’t work for a co-employment agreement that can reshape payroll administration, benefits strategy, compliance exposure, and renewal costs for years.

A PEO decision belongs in the same category as a major finance and risk decision, not a casual vendor search. The hard part isn’t figuring out whether a portal looks polished. The hard part is determining whether the provider can support your workforce model, price the relationship transparently, and write a contract that won’t become expensive to unwind later.

The gap in most professional employer organization reviews is simple. They focus on what is easy to market and ignore what is expensive to fix.

Table of Contents

- The Problem with Five-Star Ratings for a Seven-Figure Decision

- Why Most PEO Reviews Are Unreliable

- A 6-Point Framework for Truly Vetting a PEO

- Decoding PEO Pricing and Uncovering Hidden Costs

- The Contractual Risks Most Reviews Ignore

- How to Compare PEO Providers Side-by-Side

- Negotiation Levers to Secure a Better PEO Agreement

The Problem with Five-Star Ratings for a Seven-Figure Decision

A five-star rating doesn’t tell a CFO what happens when a payroll tax issue hits a quarter-end close, when a benefits renewal comes back higher than expected, or when a multi-state hiring push exposes gaps in compliance support.

That matters because the value of a PEO relationship is material. According to NAPEO industry overview data, businesses that use a PEO grow two times faster, experience 12 percent lower employee turnover, and are 50 percent less likely to go out of business than comparable non-PEO businesses. If the upside is that significant, the downside of choosing badly is also significant.

Typical review pages flatten this into soft criteria. Friendly support. Easy onboarding. Clean dashboard. Those details matter, but they’re secondary. The economic outcome of the relationship is driven by pricing mechanics, benefit plan design, compliance execution, and contract terms.

Practical rule: If a review doesn’t discuss the client service agreement, renewal terms, and service ownership, it isn’t a serious review. It’s marketing content.

A buyer evaluating options for a workforce between 10 and 2,000 employees usually isn’t asking, “Do employees like the app?” The key questions are sharper:

- Can finance model the total cost? Not just the admin fee, but benefits, workers’ compensation treatment, taxes, and renewal exposure.

- Can HR get reliable support? Not a generic hotline. Named contacts, escalation paths, and issue resolution expectations.

- Can leadership exit cleanly if needed? Data access, implementation repayment terms, termination notice, and liability language matter more than testimonials.

The smarter way to read public feedback is to treat it as a weak signal, not a verdict. It can help surface themes. It can’t replace diligence.

For buyers trying to sanity-check how a specific provider is discussed in the market, a focused review such as Group Management Services reviews analysis can be useful. But it should only be one input among contract review, pricing comparison, and reference calls with long-tenure clients.

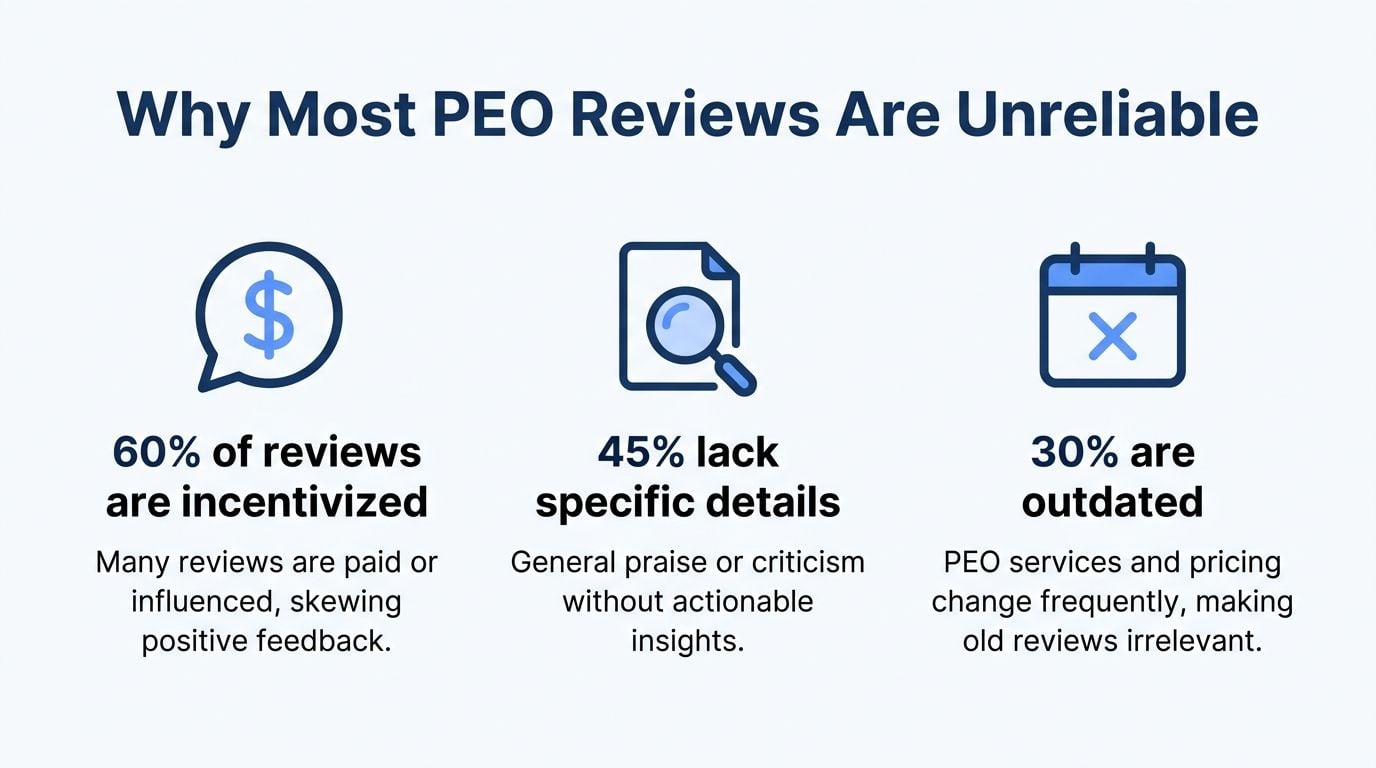

Why Most PEO Reviews Are Unreliable

The average PEO review article is built to attract search traffic, not to protect a buyer from a bad agreement. That’s why so many listicles look nearly identical. They reward visibility and broad brand recognition, then dress the results up as objective analysis.

The market itself makes this worse. The PEO industry includes over 6,675 businesses as of 2026, and fewer than 10% of the 900+ distinct PEOs hold the IRS Certified Professional Employer Organization designation, according to IBISWorld industry data. A crowded market with limited certification at the top end isn’t something a generic “best PEOs” list can simplify honestly.

What review content usually gets wrong

Many review pages rely on three weak inputs:

- Shallow summaries: They repeat homepage language about payroll, HR support, and benefits access without testing how those services are delivered.

- Outdated assumptions: PEO service models change. Account teams change. Carrier mixes change. Contract terms change.

- No risk lens: They compare features and skip the legal and financial structure that governs the relationship.

That last point is the most damaging. A provider can score well in public sentiment and still be a poor fit for a company with field employees, multiple tax jurisdictions, or complex leave requirements.

What serious buyers should verify instead

The fastest way to pressure-test a review is to look for missing operational detail. If it doesn’t answer these questions, it probably isn’t decision-grade research:

| Review test | Weak review | Useful review |

|---|---|---|

| Contract coverage | Barely mentioned | Explains renewal, notice, exit, and liability terms |

| Service model | “Great support” | Names dedicated rep model or call-center model |

| Compliance fit | Generic | Distinguishes by state complexity and industry risk |

| Financial stability | Omitted | Screens for accreditation and certification |

| Cost analysis | Quote-level only | Separates admin fees from pass-through and markup risk |

A better starting point is to study recurring buyer pain points instead of star averages. Pattern-based resources such as PEO customer complaint pattern analysis are more useful because they expose where implementations break down, where communication fails, and where billing disputes tend to surface.

The question isn’t whether a PEO is popular. It’s whether the provider can carry your risk profile without creating a future contract problem.

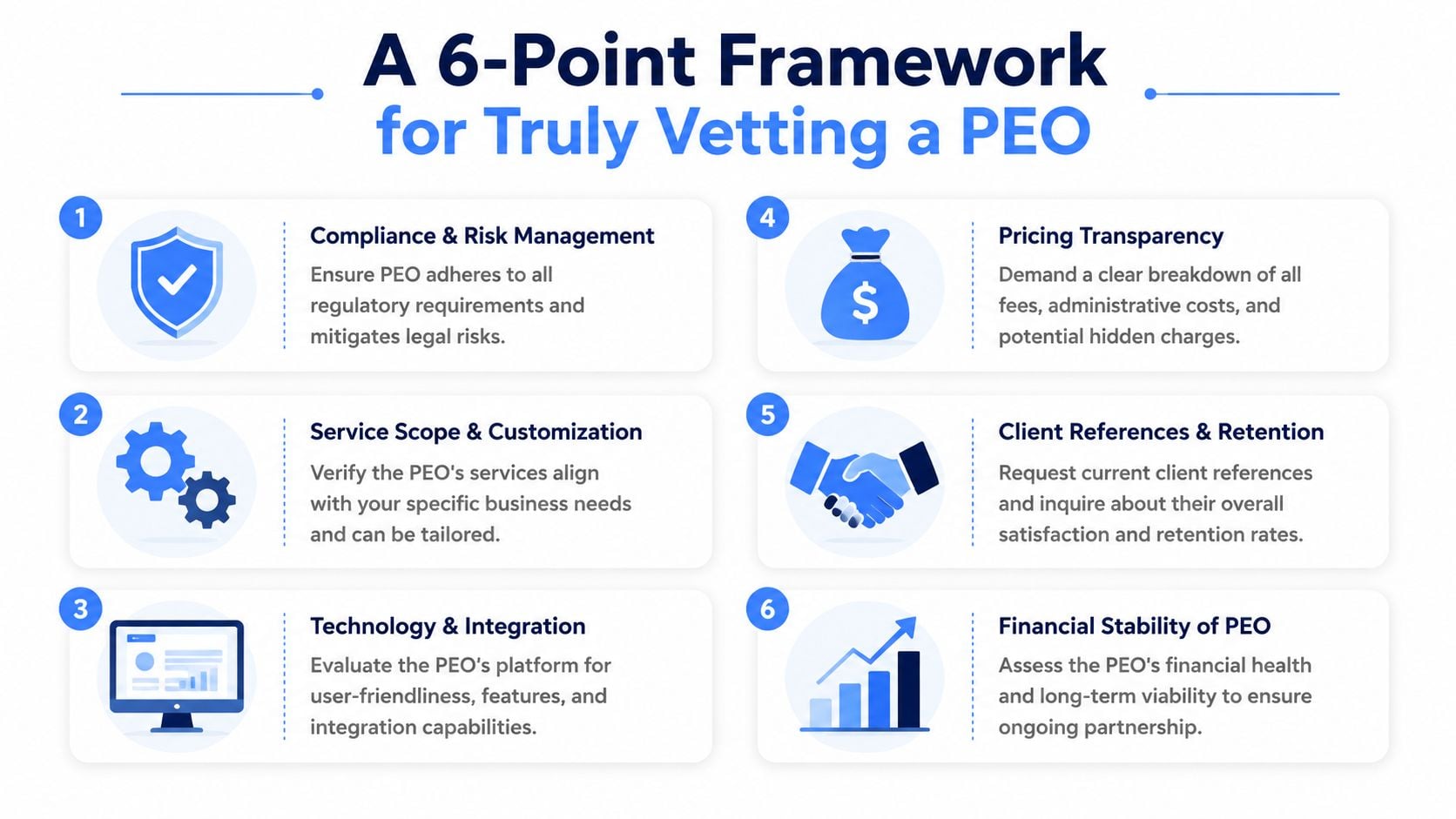

A 6-Point Framework for Truly Vetting a PEO

A strong PEO evaluation has to produce an apples-to-apples decision. That means each finalist gets reviewed under the same operational, financial, and contractual lens. Anything less leaves too much room for sales choreography.

A useful companion to internal diligence is Benely’s guide for evaluating PEOs, especially for organizing discovery questions before demos and finalist calls. The key is to use any checklist as a starting point, not as a substitute for contract and pricing analysis.

Price structure before sticker price

A quote that looks lower at first glance can become more expensive if the fee base expands with payroll, renewals, or benefits administration changes.

Buyers should ask for a line-item breakdown that separates:

- Administrative pricing model

- Benefits costs

- Workers’ compensation handling

- Tax-related pass-through items

- Implementation charges

- Any fees tied to off-cycle payrolls, amendments, or year-end processing

A quote isn’t transparent if finance can’t model it for the next renewal cycle.

Benefits quality and contribution design

Many professional employer organization reviews treat benefits as a yes-or-no feature. That’s too shallow. The issue isn’t whether a provider offers medical, dental, vision, life, or disability plans. The issue is whether the contribution strategy fits the workforce and whether employees will use the plans.

When benefits are reviewed properly, HR should test:

- Carrier choice and plan structure

- Voluntary benefit depth

- Employer contribution flexibility

- Enrollment support for employees

- How renewal changes are communicated

A benefits package that looks strong on a spreadsheet can still fail if employee cost share is out of line with local labor expectations.

Service model and escalation path

Service quality isn’t about whether the sales team is responsive. It comes down to who owns the account after implementation.

A CFO or HR director should know:

- whether there’s a dedicated account manager

- whether payroll support is pooled or named

- how urgent issues escalate

- how support works during payroll cutoffs and renewal periods

Decision test: Ask each finalist to show the post-sale support structure in writing. If that answer stays vague, support will stay vague after signature.

Compliance depth and accreditation

Compliance support has to be examined at two levels. First, can the provider handle federal and state employment requirements across the footprint? Second, can it handle the employer’s industry-specific obligations?

Accreditation and certification help narrow the field. For that reason, buyers should review a provider’s PEO accreditation standards and distinctions before moving too far into pricing discussions. Certification doesn’t guarantee fit, but lack of it should trigger deeper scrutiny.

Contract terms and exit mechanics

A clean buying process often gets derailed here because legal review starts too late. The client service agreement should be part of the evaluation, not an end-stage formality.

Review these items before final pricing discussions end:

- Rate increase language

- Termination notice requirements

- Data export obligations

- Implementation fee treatment

- Allocation of liability for compliance errors

- Renewal structure and auto-renew terms

If a provider won’t share agreement language early, that’s a warning sign.

Industry fit over generic scale

The largest provider isn’t always the safest pick. A healthcare employer, contractor, franchise operator, or fast-scaling tech company often needs a different compliance and service model than a low-complexity office workforce.

Generic reviews fail most often. They rank brands by awareness and skip the harder fit questions:

- Does the provider understand workforce classification risk?

- Can it support state-specific leave and tax complexity?

- Does it have specialists who work with similar employers every day?

- Can it speak clearly to the reporting and documentation your team needs?

A disciplined framework makes weak proposals obvious. It exposes where a provider is polished in demo settings but thin in service design, contract flexibility, or compliance depth.

Decoding PEO Pricing and Uncovering Hidden Costs

Pricing confusion is one reason bad PEO decisions survive longer than they should. The buyer thinks the quote is competitive, then finance discovers later that the actual cost sits in markups, pass-through treatment, or renewal mechanics.

Benchmark data cited by Alpha Apex Group on top PEO companies says over 75% of PEO users realize significant annual cost savings. That can absolutely be true. But those savings show up when pricing is transparent, not when the fee structure hides cost movement in payroll, taxes, or workers’ compensation treatment.

What a quote needs to separate

A useful PEO quote should let finance answer one question quickly. What is fixed, what varies, and what can rise at renewal?

A clean comparison should isolate:

- Admin fee structure such as percentage of payroll, per-employee pricing, or a hybrid model

- Benefit premiums and whether there is any embedded administrative margin

- Workers’ compensation treatment including whether rates are pooled or experience-sensitive

- Payroll tax handling and any fee built into tax processing

- One-time implementation charges

- Fees triggered by special requests such as off-cycle runs, reporting support, or custom integrations

Without that separation, low pricing can be an illusion.

What works and what backfires

A percentage-of-payroll model can align well when compensation levels are stable and the formula is clear. It can backfire when payroll rises quickly and the agreement doesn’t put guardrails around fee growth.

A per-employee model can look easier to budget. It can also become less predictable if the provider layers annual admin increases, benefit markups, or extra service charges that weren’t visible during the sales process.

The right evaluation method is simple:

| Pricing question | Why it matters |

|---|---|

| What is the billing unit | It determines how cost moves as headcount or payroll changes |

| What is pass-through | It shows what the PEO controls versus what the client ultimately funds |

| What can renew upward | It identifies budget risk before contract signature |

| What services cost extra | It prevents year-one surprises |

For companies that need a more structured way to dissect quote design, a detailed review of PEO pricing and cost structure helps frame the right questions for finance, HR, and legal together.

A cheap quote that can’t be modeled is more dangerous than an expensive quote that can.

The Contractual Risks Most Reviews Ignore

Most reviews stop at service impressions. The contract is where the actual relationship lives.

This is the biggest blind spot in professional employer organization reviews because the painful terms usually don’t show up during the sales cycle. They show up when the company wants to leave, renegotiate, or challenge a renewal increase. By then, their negotiating position is weaker.

Data shows 68% of SMBs face unexpected termination fees when switching PEO providers within the first 24 months, and 41% of companies are unaware of automatic rate increase clauses until renegotiation, leading to $12,000 to $35,000 in unforeseen costs. That isn’t a minor administrative issue. That’s a finance issue, a legal issue, and often a board-level trust issue if the switch was meant to reduce cost or risk.

Clauses that deserve line-by-line review

The client service agreement should be treated like an operating document, not boilerplate. Finance and counsel should review at least these points carefully:

- Termination fees tied to minimum terms, notice periods, or implementation cost recovery

- Automatic renewal language that narrows the window to exit cleanly

- Annual fee escalation clauses that don’t define how increases are calculated

- Liability allocation for payroll, tax, benefits, and compliance errors

- Data ownership and export terms for employee files, payroll history, and reports

A polished implementation and decent portal don’t offset a contract that makes exit expensive.

What to ask legal and finance to mark up

A buyer should ask counsel to mark every clause that shifts operational mistakes back to the employer. Finance should mark anything that can increase spend without a negotiated approval point.

Useful questions include:

- What notice is required to terminate without penalty

- What fees survive termination

- Who pays if the PEO makes an error

- How quickly must the provider return payroll and employee data

- What exactly triggers a rate increase

Review the cancellation language before the benefit deck. If exit is punitive, the relationship isn’t flexible, no matter how attractive the first-year pricing looks.

How to Compare PEO Providers Side-by-Side

A side-by-side comparison should expose trade-offs, not hide them. Most buyers already know that national firms tend to have broader infrastructure, regional firms may offer closer support, and newer tech-forward providers often present cleaner user experiences. That isn’t enough to make the call.

The missing layer is fit. A regulated employer should care whether the provider has actual industry fluency. That’s especially important because a 2025 Gartner market analysis found that industry-specialist PEOs reduced compliance violations by 32% compared to generalists for mid-market firms in regulated sectors like healthcare and construction. Generic rankings rarely account for that.

For buyers reviewing the broader field, a current list of professional employer organizations is useful for market mapping. The actual work starts after the list, when each provider is scored against the same operating criteria.

PEO Vetting Comparison Matrix

| Evaluation Criterion | PEO A National Generalist | PEO B Industry Specialist | PEO C Modern Tech-First |

|---|---|---|---|

| Pricing format clarity | Broad proposal, may require follow-up to isolate pass-through items | Usually clearer on industry-specific cost drivers | Often clean presentation, but extras need review |

| Service model | Larger pooled support structure is common | Dedicated team is more common | Strong portal, support depth varies |

| Industry expertise | Broad coverage, less tailored | Strong fit for regulated or niche workforces | Better fit for straightforward operating models |

| Compliance approach | Wide-state coverage, process-driven | Deeper workflows for specialized requirements | Good automation, may be lighter on edge cases |

| Contract flexibility | Terms may be more standardized | Sometimes more negotiable for fit-sensitive clients | Can be flexible, but check renewal language closely |

| Termination process | Needs careful review for notice and fees | Often easier to evaluate if scope is narrower | Varies widely |

| Best fit | Employers prioritizing scale and broad infrastructure | Employers with complex regulatory exposure | Employers prioritizing usability and modern workflows |

This type of comparison reveals a pattern quickly.

A healthcare group, contractor, or multi-state employer with leave complexity might accept a less polished interface if the specialist provider can manage compliance risk more effectively. A lower-complexity office-based employer might make the opposite choice and prioritize technology and employee self-service.

The best PEO on paper isn’t the one with the longest feature list. It’s the one whose service model, contract terms, and compliance depth match the company’s operating reality.

Negotiation Levers to Secure a Better PEO Agreement

Selection isn’t the finish line. The strongest advantage usually exists after the shortlist is clear and before legal redlines begin.

According to the U.S. Chamber of Commerce overview of professional employer organizations, a PEO’s client service agreement must define the precise conditions for rate increases. Pushing for a clause that limits annual increases to 3% to 5% is a critical negotiation point for predictable long-term cost.

Useful asks include:

- Rate increase cap so renewal exposure doesn’t drift without explanation

- Implementation fee credit or waiver if the provider wants the business urgently

- Defined service levels for payroll support, account response, and issue escalation

- Data export commitment so transition risk is controlled if the relationship ends

- Termination language revision to reduce penalties and shorten notice friction

- Named support structure written into the agreement or implementation documents

For employers tightening hiring quality alongside PEO selection, tools that improve candidate screening can also reduce downstream HR strain. A practical reference point is MyCulture.ai’s top assessment tools, especially for teams trying to pair better HR infrastructure with stronger hiring processes.

The takeaway is straightforward. Negotiate the downside before celebrating the upside.

PEO decisions get expensive when buyers rely on marketing summaries instead of contract language, cost modeling, and fit analysis. PEO Metrics helps companies compare providers side by side, flag hidden pricing and contract risks, and negotiate stronger terms before signing.